ETF ‘ants’ about to crawl through the US

Globally, passive ETFs have dominated market share when compared to actively managed ETFs. However, against a backdrop of extreme market volatility, there’s increasing interest in active management, and there’s been a major development in the past week that could see the active-ETF floodgates open in the US.

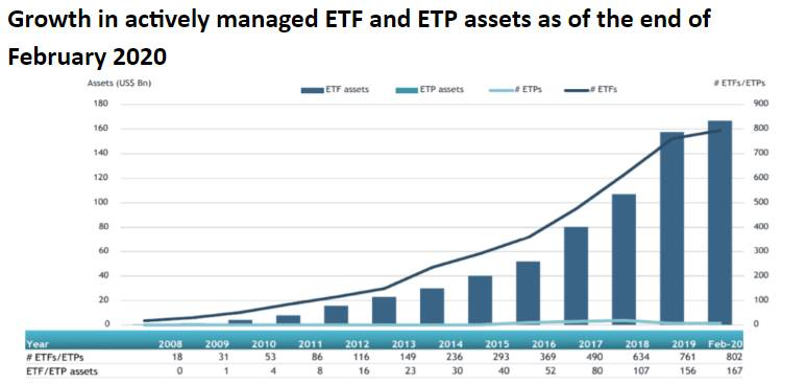

Surprisingly to many, active ETFs have been around in the US for 12 years, mostly in fixed income. There are now 802 active ETFs globally with assets of $167 billion. As the chart below highlights, growth has accelerated over the past 12 months.

Source: ETFGI, March 2020

But, unlike in Canada and Australia where active ETFs can disclose portfolio holdings on a monthly or quarterly basis, US regulators have required all ETFs to provide daily portfolio holdings disclosure.

This is something that has deterred many active managers from offering access to their strategies via an ETF.

Enter the ANTs

On 2 April 2020, American Century (the asset manager) using a structure called Precidian Activeshares, listed two Active Non Transparent (ANTs) ETFs in the US. The non-transparent bit relates to the quarterly (not daily) portfolio holdings disclosure of these actively managed ETFs.

This is a big moment for the US ETF market. More high-quality active managers in the US are now likely to follow suit and offer investors the benefits of an actively managed portfolio (especially relevant in volatile markets) combined with the benefits of the ETF wrapper (the ease of on-exchange investing).

These developments in the US should lead to growing interest and research into active ETFs globally, including here in Australia where a number of high-quality active ETFs are proving to be important elements of investor’s portfolios.

Following the ‘ANT’ ETF listings in the US, I decided to interview Andres Rincon, one of the leading ETF analysts covering the US and Canadian ETF industry.

Andres is TD Securities’ Canadian-based Director of Equity Derivatives and ETF strategy.

I believe Canada is around five years ahead of Australia in terms of non-transparent active ETFs and Australia is around 5 years ahead of the US. Active ETFs make up around 20% of ETF assets in Canada vs 5% in Australia and less than 3%in the US. So, given Canada is the world’s pioneering active ETF market, speaking to a Canadian expert makes sense!

Q&A with Andres Rincon

Q. How big is this news out of the US ETF market?

A. Thank you for having me Chris. This is a big deal for the US ETF market. The approval of these non-transparent structures changes the footprint of the traditional US ETF market which was founded on passive and fully transparent ETFs, and signals to the investing public that the SEC is pivoting in favour of non-transparent structures. Needless to say that the US ETF market is about to become considerably more sophisticated.

Allow me to first provide some context. For years, the SEC was categorically against non-transparent ETFs in the US given concerns of illiquidity and wide spreads in times of distress and tracking error relative to the underlying basket due to the imperfect arbitrage opportunities offered under the non-transparent structures filed. These non-transparent structures filed are different than those offered in Canada or Australia. All of the non-transparent structures filed over the years were similar and did not pass the SEC smell test. These applications were not outright denied, rather just not approved. In May 2019 the SEC took action on Precidian (ActiveSharessm) clearly signaling to the street that non-transparent ETFs were the way forward despite ongoing liquidity, spreads and disclosure concerns. In the interest of fairness and competition, the SEC subsequently approved the other four outstanding non-transparent ETF structures.

Within the spectrum of regulatory flexibility, the US has historically been the strictest on non-transparent ETFs, Canada has been the most lenient, and Australia was somewhere in between but closer to Canada. In Canada, ETF providers are allowed to disclose holdings to investors on a delayed basis (usually quarterly). Most ETFs listed in Canada disclose holdings daily to investors and market makers, but around 30% of ETFs listed in Canada do not disclose their holdings to the public daily. The approval of non-transparent ETFs in Canada has allowed actively managed ETFs to thrive and now represent 20% of the Canadian ETF market. The recent action taken by the SEC looks very similar to the beginnings of a story that is already well developed in Canada.

Q. What do you think caused the SEC to change its mind?

A. A variety of factors contributed to the approval of these non-transparent structures, but we believe politics played a big role in the shift in mindset. The SEC has been fielding pressure from both investors and fund providers for many years as the interest to have actively managed strategies within an ETF wrapper has grown over the years. Fund companies that filed the different non-transparent structures worked diligently with the SEC to appease some of the concerns they had regarding liquidity, spreads and disclosure. Despite this work the SEC remained split with the majority of commissioners remaining against approving non-transparent structures.

A change of government in the US led to personnel changes at the SEC. These changes were taken by investors as being more pro-business, and initially brought speculation that the approval of non-transparent ETFs was simply a matter of time. Time transpired and this view faded, but partisan politics grew within the SEC Commission and subsequently the Precidian model was approved despite reservations from some of the SEC Commissioners. The approval of the Precidian non-transparent model left the SEC Commission no choice but to approve all other non-transparent structures in the interest of open competition and fairness.

Q. How big could active ETFs become, when looking at your Canada experience?

A. The introduction of non-transparent ETFs will undoubtedly fuel the growth of actively managed ETFs in the US. Actively managed ETFs that offer full transparency already exist in the US, but their growth has been muted due to the limited distribution platforms of the fund managers offering these active strategies, when compared to the traditional ETF companies. But the approval of multiple non-transparent structures from large fund companies with large distribution capabilities such as Fidelity and T. Rowe Price and many others that could license the approved non-transparent structures, it will open the door to the traditional active fund managers to launch actively managed ETFs in the US without having to disclose their secret sauce.

Canada is a great test case for the US, and the global leader in actively managed ETFs. When Canadian regulators last commented on non-transparent ETFs three years ago and greenlighted any future launches, our numbers indicated that actively managed ETFs only represented 5% of ETF assets under management (AUM) in Canada. Since then actively managed ETFs have grown over six fold and now represent 20% of AUM in Canadian ETFs. The number of actively managed ETF launches has also increased dramatically in Canada. One asset class that dramatically benefited from non-transparent ETFs is fixed income. In the first half of 2019 about 25% of assets going into ETFs has been on actively managed fixed income ETFs. Although offering multiple non-transparent structures may complicate matters in the US, if Canada is a guide the approval of non-transparent structures will likely open the door to the rapid growth of actively managed ETFs in the US.

Q. What kind of asset class strategies are likely to be available in active ETFs across US and Canada?

A. In Canada fund managers can offer non-transparent and active strategies in a wide set of asset classes including, equities, fixed income, derivatives, and commodities. In the US active strategies can also be offered in a wide range of asset classes, however one of the key restrictions by the SEC in approving non-transparent ETF structures is that these ETFs can only include securities that trade on an exchange that can be tracked and monitored. This means that for now only exchange traded securities such as equities, commodities and derivatives can be included in these portfolios, while over-the-counter fixed income securities would not be allowed. This contrasts with non-transparent actively managed ETFs in Canada, which are common seen in fixed income ETFs.

Another area that has flourished in Canada and may gain momentum in the US with the approval of these structures is market-neutral strategies or more hedge fund like strategies. These strategies have been offered under ETFs in the US for some time now, but its growth has been limited by the unwillingness of the traditional hedge fund manager to share its holdings. Given the option to launch non-transparent ETFs, portfolio managers of long short strategies and other strategies will be more likely to launch an ETF version of their strategies.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris is part of the Pinnacle executive management team and responsible for driving the listed products business. Pinnacle’s mission is to establish, grow and sustain a diverse and complementary stable of world-class, specialist investment managers

........

This communication was prepared by Pinnacle Investment Management Limited (ABN 66 109 659 109 AFSL 322140) (‘Pinnacle’). Past performance is for illustrative purposes only and is not indicative of future performance. Unless otherwise specified, all amounts are in Australian Dollars (AUD).

This communication is for general information only and was prepared for multiple distribution. Whilst Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information.

The information is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. The information in this communication has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. The issuer is not licensed to provide financial product advice. Please consult your financial adviser before making a decision.

Any opinions and forecasts reflect the judgment and assumptions of Pinnacle and its representatives on the basis of information at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. The information is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment.

Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Pinnacle. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

3 topics

Chris is part of the Pinnacle executive management team and responsible for driving the listed products business. Pinnacle’s mission is to establish, grow and sustain a diverse and complementary stable of world-class, specialist investment managers

Expertise

Chris is part of the Pinnacle executive management team and responsible for driving the listed products business. Pinnacle’s mission is to establish, grow and sustain a diverse and complementary stable of world-class, specialist investment managers

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management