Foxes and hedgehogs

When it comes to investor psychology, the Ancient Greeks knew what they were talking about.

They categorised people as either hedgehogs or foxes. Foxes, they said, know many things whereas hedgehogs know one big thing.

Early last year equity investors were all hedgehogs with the Coronavirus being the one big thing they knew.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

As a result, between 20 February and 23 March, the MSCI World Index went down by a third in the steepest decline of its size on record and the VIX index, a volatility measure of the S&P 500 known as the ‘fear index’, blew out to an all-time high.

However, from the March market low, there was a gradual transformation from hedgehog to fox culminating in Q4. Throughout this time, many stocks rallied significantly. Equity indices in the US hit all-time highs driven by a historic imbalance between a very small number of "mega-cap" technology stocks and the rest. Investors woke up from the pandemic being the only thing that mattered, to it being one of many factors.

Of those that we would highlight, three were general and should persist into 2021:

- Monetary and fiscal stimulus was of unprecedented scale and accompanied by clear "whatever it takes" commitments from authorities worldwide,

- The development of vaccines in record time meant it was possible to look through the disturbing short-term COVID data,

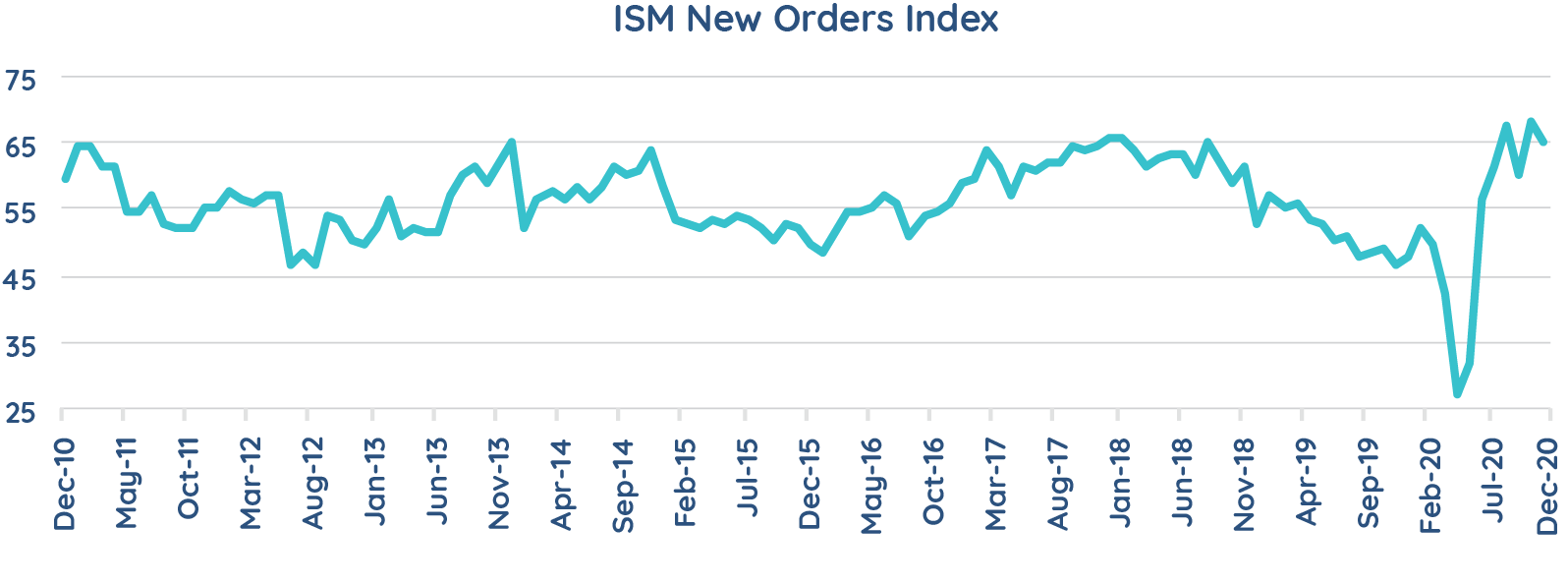

- Economic data began to recover and drove sentiment: showing investors arguably care less about current levels and more about changes of direction.

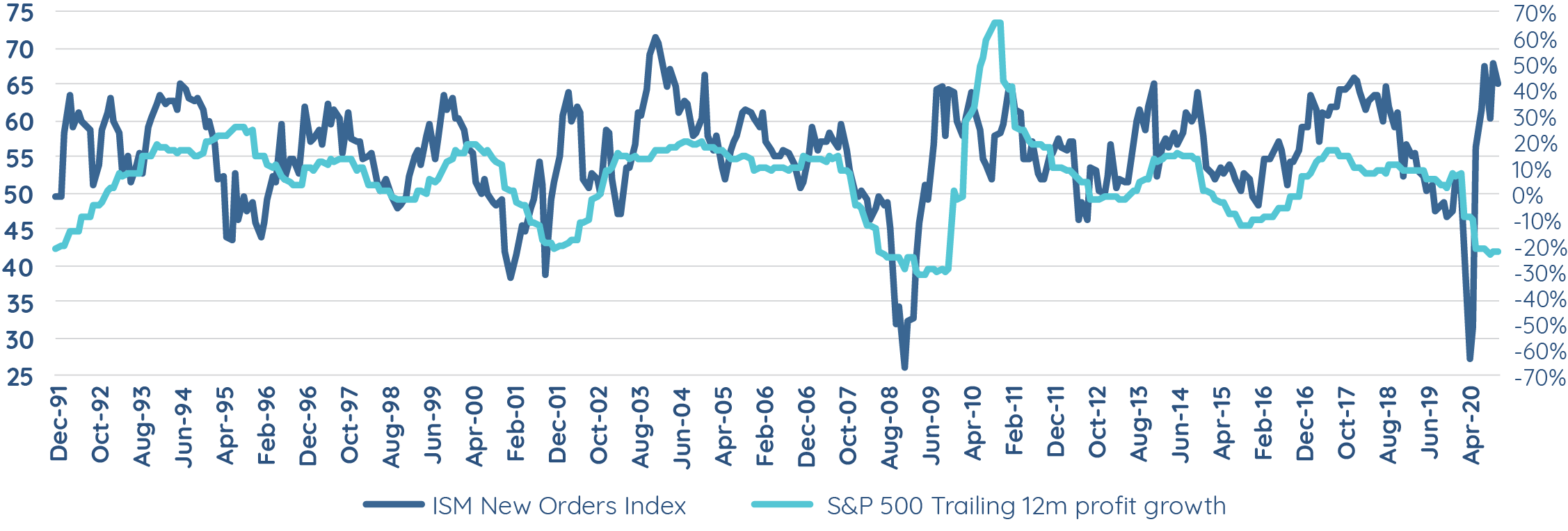

Source: Talaria, St Louis Federal Reserve

Source: Bloomberg, Talaria

The US election was a specific factor:

- Biden becoming President-elect eliminated one uncertainty, and markets hate uncertainty,

- While by the end of December there was no "blue sweep," the early January elections have now given the Democrats control of the Senate, which will likely be more stimulatory for the US economy.

Most importantly, for all the terrible consequences of the pandemic, it had a major positive effect in ending a long-running economic cycle while kicking off a new one.

While monetary and fiscal measures prevented economies completely falling off a cliff, they also offer an opportunity to invest in this year’s early cycle economic growth and future expansion.

The equity advantage

In our view, equities are a good way to approach this reset.

Cash and bonds as significant parts of a retirement portfolio are probably non-starters. Both have their places but interest rates on cash are very low and it would take an unusual view of the world to justify a heavy weighting. More importantly, as we discussed previously, government bonds in developed markets are unattractive in that they:

- Tend to be expensive, offering little, no or negative yields to maturity

- They are unlikely to offer the traditional hedging characteristics upon which the classic 60:40 portfolio (60% equities: 40% bonds) is based - on current valuations, investors cannot expect government bonds to provide positive returns when stock markets fall

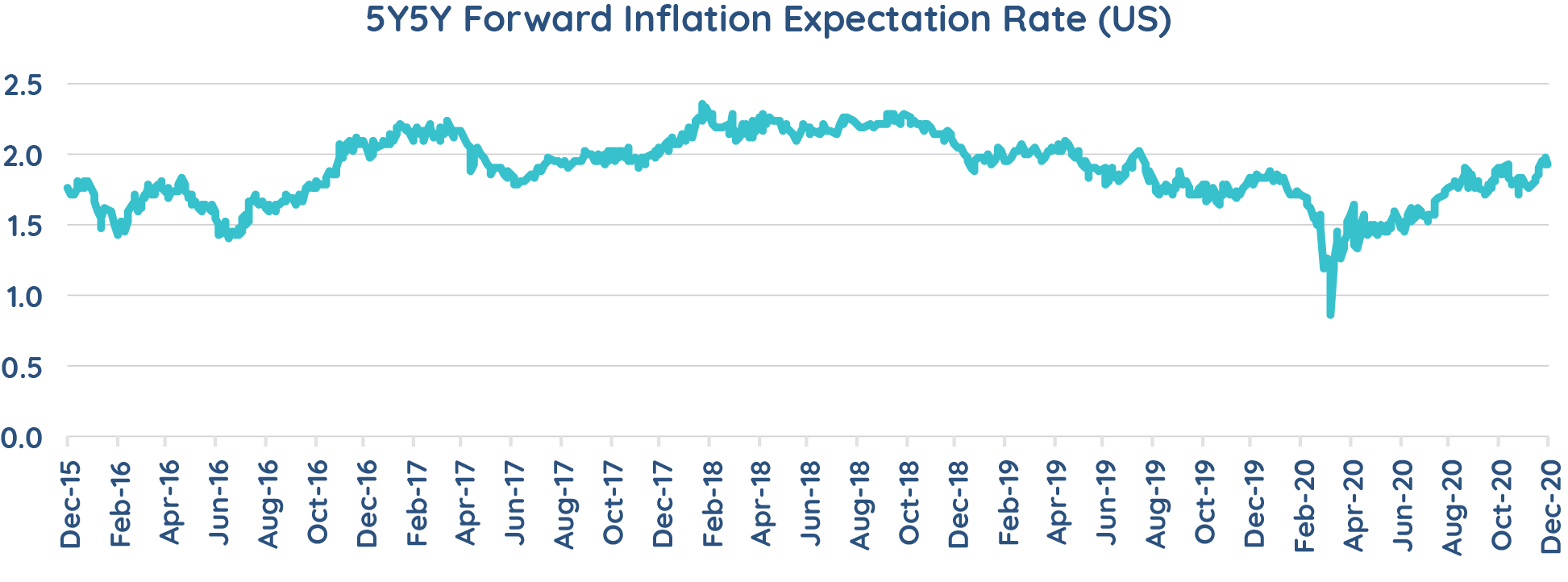

- They are vulnerable to inflation, the threat of which is the most credible since the early eighties.

Equities on the other hand represent regions, sectors, industries and companies that will, in many cases, see their cash flows grow with economic recovery.

Moreover, although it is a complicated dynamic, equities (particularly those valued as shorter duration) – shorter time to make back your investment or those representing companies with a degree of pricing power – can also benefit from inflation picking up.

This means while an investor knows that growing inflation will reduce her real return from bonds, she might see an improvement in her return from shares if the companies the shares represent can grow cashflows in the inflationary environment.

Which equities?

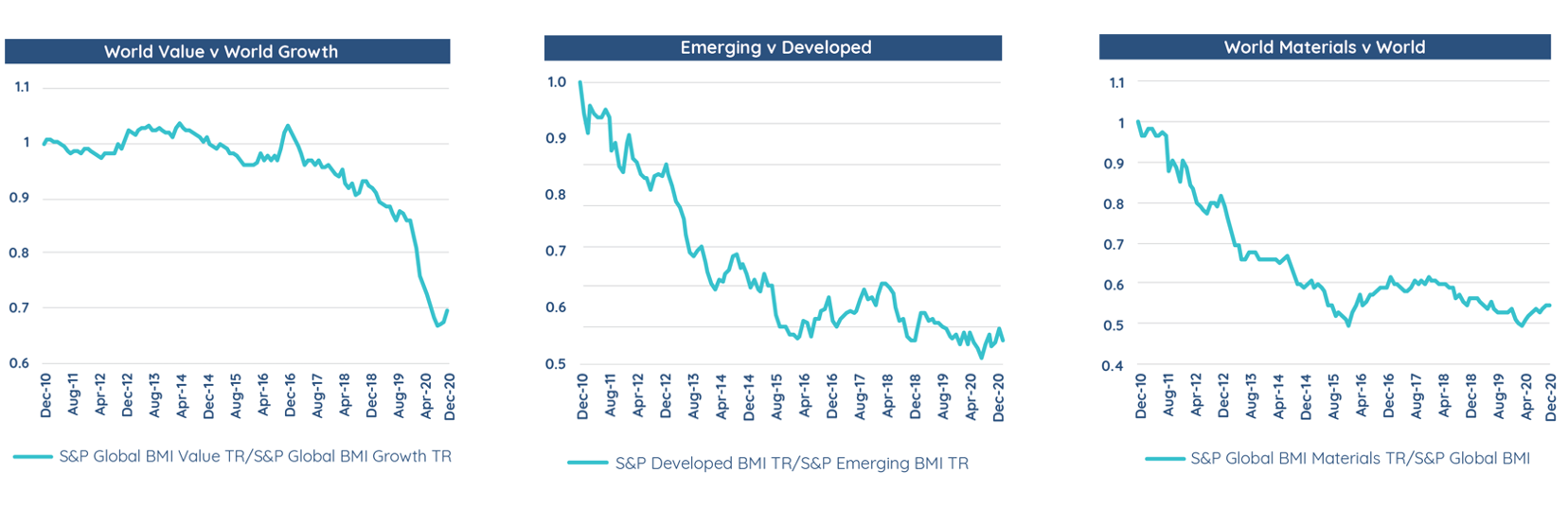

One rule is to buy growth when growth is scarce, and to buy value when there is growth for all. A variation on this theme is to invest in value when there is a wide-spread between value and growth and invest in growth when that spread is narrow.

Source: Talaria, Bloomberg

This arbitrage lens provides a guide to which areas of the market are interesting. Strictly speaking, arbitrage is a value-based strategy but relative performance is useful shorthand, with areas that have been weak for an extended period worthy of consideration as the below charts demonstrate (all charts below are 10-year price relative):

Source: S&P Dow Jones Indices

As the charts show, one class of shares can underperform another for years: in themselves these relationships are not timing tools, yet they are powerful indicators of when there are changes in economic and market cycles. In view of the reset, they are worth taking seriously.

Stay up to date

Don't forget to click "like" if you enjoyed this wire, and hit the "follow" button below to be informed whenever Chad publishes on Livewire.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase the certainty of global equity returns for investors through its:

> Unique and structurally lower-risk investment approach that combines capital growth and income generation to deliver a more consistent return profile (smoothing).

> Portfolio of up to 45 large, globally listed companies.

> Internationally experienced and personally invested leadership team.

www.talariacapital.com.au

........

The information in this article is general information only and is not based on the objectives, financial situation or needs of any particular investor. In deciding whether to acquire, hold or dispose of the product you should obtain a copy of the current Product Disclosure Statement (PDS) for the Fund and consider whether the product is appropriate for you.

Wholesale Units in the Talaria Global Equity Fund (the Fund) are issued by Australian Unity Funds Management Limited ABN 60 071 497 115, AFS Licence No. 234454. Talaria Asset Management Pty Ltd ABN 67 130 534 342, AFS Licence No, 333732 is the investment manager and distributor of the Fund. References to “we” means Talaria Asset Management Pty Ltd, the investment manager. A copy of the PDS is available at australianunity.com.au/wealth or by calling Australian Unity Wealth Investor Services team on 13 29 39. Investment decisions should not be made upon the basis of the Fund’s past performance or distribution rate, or any ratings given by a rating agency, since each of these can vary. In addition, ratings need to be understood in the context of the full report issued by the rating agency itself. The information provided in the document is current at the time of publication.

3 topics

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets