Fremont Petroleum FPL.ASX - Prove the Theory to Win the Acreage Prize

There are a few reasons why I recently took an interest in Freemont Petroleum (FPL.ASX $0.011), the first was that they had an existing gas reserve in place, (the “Backup Value”), and they owned 100% of a large 21,500 acre field, for which they are getting first results in as we speak (the “Bluesky”). The other key piece of information is the company was previously known as Austin Exploration AKK.ASX (a real “Stinker”, if I summarise bluntly), and the stale selling of AKK shareholders kept the newly recapitalised/new management FPL cheap. I am interested now, as it looks as if the first well (JW Powell) will work and prove their “Theory”, which may show FPL is sitting on 21,500 acres of very undervalued ground (at $0.011 trading on back of the envelope US$444 per acre, whilst Wattenburg to north is trading ~US$5,000 to ~$15,000 per acre)

Schlumberger( SLB.NYS $59b Mkt Cap) at site fracture stimulating JW Powell well. No small operation

Schlumberger( SLB.NYS $59b Mkt Cap) at site fracture stimulating JW Powell well. No small operation

FPL.ASX share price - 2 Year Chart

FPL.ASX share price - 2 Year Chart

The Background

FPL is based in Fremont County Colorado US. It has current production ~120 boe/d Production (including ~23bopd from its Kentucky leases) which gives it enough cash flow to wash its face. Further, it has 1.8mmboe of Reserves of liquids-rich gas and oil in FPL’s 100% owned Pathfinder field (yet to commercialise). It has 21,500 of largely contiguous acreage 100% owned over the Niobrara Shale (Net Revenue Interest of ~75% (between 72% to 81%) in a producing area.

The Stinker

Previously known as Austin Exploration (AKK.ASX), which had a pretty consistent history of raising money, unsuccessful drilling and deals, then raising more money at ever lower prices. Thus 1,232,770,559 shares on issue and the micro market cap [$13.5m at 1.1c]. It changed to Freemont Petroleum back in June 2017. Plenty of shareholders happy to move on I imagine, however that might be unfortunate timing. Since AKK change to FPL, there have been management changes, and the company was recently recapitalised, most recently at 0.7c (Mkt Cap $8.6m). Management has put their own money into the company. So no free rides, and they want to protect the share structure (avoid dilution if at all possible). The volume is lifting finally in FPL as results near, this allows the register to tighten up a little and take shape. (example, the latest week rolling value is $1.89m vs 6 Month rolling value $4.6m)

The Backup Value

FPL already has 3 successful horizontal wells, each flowed an average ~1.38 mmcfg/d of liquids rich gas and in part led to a big boost in Proven & Probable Contingent Niobrara Resource (2C) to 31.4 mil bbl oil and 366 bcf gas. The traditional play of the shallow Pierre Formation also has 25.6mil bbl of 2C oil, 79 bcf of gas resource. What does this all mean? They have significant gas in the ground, the value of which can only be realised if they can sign a deal with an end user, which will then allow them to connect it into regional pipelines. We are waiting on such a deal/catalyst.

The Bluesky

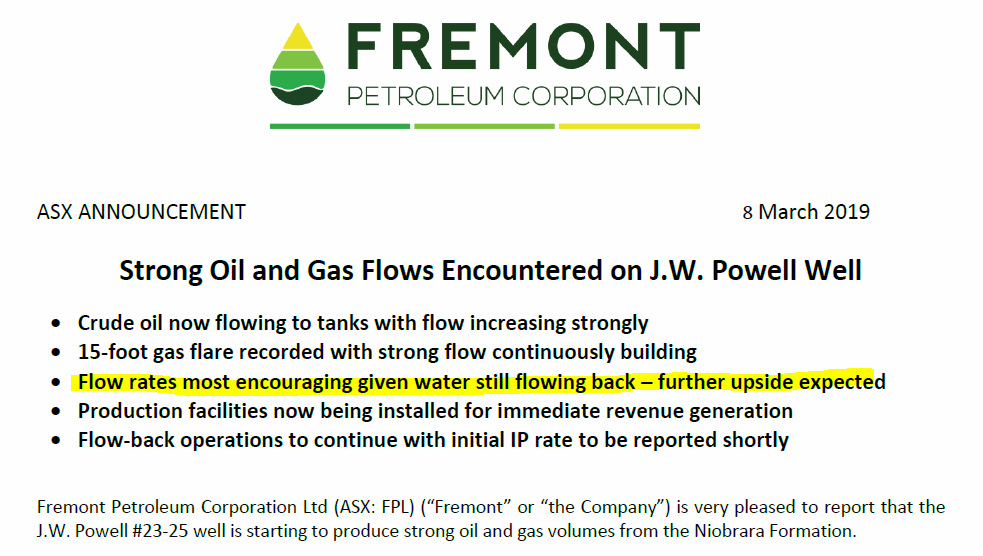

FPL has been drilling JW Powell in the Nibrara. The first thing to note is the hole is being drilled by Schlumberger (SLB.NYS $59b Mkt Cap), who are testing their highly successful fracking technique in the Niobrara formation (The prior drilling release confirmed the intersection is 537 feet thick). The short summary is Schlumberger’s innovative process dills horizontal drainage spokes into multiple layers of the Niobrara shale and fracs them. Why is this important? It is that is significantly cheaper (~$1.5m) than drilling a conventional horizontal well and fracking. This approach has been very successful elsewhere in the basin. This is Schlumberger’s gig – make no mistake, there is more for them in this well than FPL. They want to successfully prove the technique works in the Niobrara formation. This opens a lot of acreage for drilling. A big plus for FPL though. Friday’s announcement is significant. It indicates while they have only unloaded 35% of the fracking fluid, they are already flaring gas and storing oil. The assumption is clearly as the pressure abates the flow of both increases. They move very soon to IP (initial production) testing which will be a key catalyst.

The Acreage Prize

FPL may just have its luck turn. The key to the JW Powell well is for Schlumberger to be able to say that the technique works in the Niobrara (let's think of it as a demonstration well). I would be very surprised if Schlumberger did not go from not wanting to be disclosed in the FPL announcements (in case the well was not a success), to highly visible and helpful and explaining the results. Then FPL’s acreage may be worth significantly more than what it is currently priced. At $0.011 a simple acreage calculation is US$444 per acre. This is a big gap to the Wattenberg field up north, where a low price is ~US$5000/acre and they have traded recently as high as US$15,000 per acre. If I discount the low end (US$5000) by 50%, that is US$2,500 per acre. With the current share structure and exchange rate, that is a price of ~$0.065 for FPL (this is not a forecast). I acknowledge there is a lot more to do to unlock that value, and risks, however, the discount is very wide, and uniquely FPL owns 100% of the 21,500 acres.

The company says more to come.

Given the company history and restrictions from Schlumberger, I hope to date they have been very conservative in guiding the market. They are making it clear they are confident, given the early signs at JW Powell, that the flow rates to be released should be positive. They also indicated they have other things to announce to shareholders (From Friday's announcement).

“As well as providing more updates on the flow back operations, we look forward to reporting a favourable IP rate for oil & gas for the J.W. Powell well very shortly. We also have many other developments that deliver further upside for shareholders and we will report on these also.”

My first guess is this may mean they have something to say on commercialising the existing gas (only a guess).

Last Quarterly

Revenue was $280k and spent $1,565m on exploration (total expenditure $1,735m). They had $1,330m left at bank and plans to spend $1,065m over this coming Qtr. So there is an obvious question mark over future capital raise or the timing of. They can push through the quarter without needing to raise, they would be rolling the dice on the JW Powell results and whatever they are alluding to in their last announcement. As a shareholder, and in talking to others, you would think the better option is to push forward for now. I acknowledge the risk of a capital raise though. It would be good if the company clarified their thoughts on this. To be fair, they need the results from JW Powell first (a week or so away).

Announcements

31/01/2019 - Quarterly Activities Report

31/01/2019 - Quarterly Cashflow Report

07/02/2019 - JW Powell Well Operations Update

14/02/2019 - JW Powell Well Fracking Operations Complete

05/03/2019 - JW Powell Well Operations Update

08/03/2019 - Strong Oil and Gas Flows Encountered on J.W. Powell Well

Conclusion

This company interests me, as they can unlock an uplift in their acreage value by proving the flow rates using the Schlumberger technique. Good for both parties if proven. They have existing assets which are yet to be commercialised which can add value. The management has invested their own money, so realigned with shareholders. The 100% field ownership makes it a relatively easy story to understand, provided the results come in as hoped. I certainly think it is worth following, in the junior oil space. Prior to the JW Powell drilling, PAC Partners published a research note with a $0.016/share price target, very speculative buy. This PT was $0.02 prior and downgraded as a result of the fall in the oil price back in Nov/Dec 2018. (PAC was a broker to FPLs prior capital raise at $0.007)

Gas flare at JW Powell as frack fluids are drained.

Important note - I own shares in FPL and FPLOB ($0.02c Options). These are paid for shares. Wentworth and/or its officers have not been paid for this note. Wentworth has no Corporate Relationship with the company (FPL).

Please Note - This note is not a recommendation or advice to buy or sell FPL shares mentioned. FPL shares should be considered very speculative, high-risk, and volatile. There are significant risks inherent in oil and gas exploration that are not discussed in this note. You should always seek professional advice before considering any share purchase or sale. Please read our full disclaimer. This is a desk trading note, and not a research document, and the view of the authors only. The author has not met the company management and company management have had no input into this note. Wentworth has not independently checked all information contained in this note for its accuracy.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth management" for Alpine's HNW clients, and are now openly available online through the website. Everything starts with the macro, and then we work back from there in terms of asset allocation and positioning for risk. We work with leading independent research providers and have a structured approach that has worked very well over time. Outside of the core portfolios, we look for opportunities in the small to mid-cap sectors of the market, where our experience can add value.

3 topics

1 stock mentioned

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth...

Expertise

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth...

Expertise

Comments

Comments

Sign In or Join Free to comment