How to invest in ASX dividend stocks, plus the dividend stripping strategy

ASX stocks pay some of the biggest dividends in the world and due to franking credits, they can be extremely lucrative for Aussie investors.

FY25 half-year earnings season is upon us (FY24 full-year reporting season for some companies!), which means it's time to begin getting your investing house in order. We’re gearing up for earnings season at Market Index and over the next few weeks, we’ll be releasing several articles to help you with:

- When companies are about to report

- What the market is expecting of them when they do

- Dividend amounts and ex-dividend dates

We’re going to kick off our earnings season coverage with dividends. Wait a minute – nobody’s declared a dividend for this earnings season yet – so there aren’t any ex-dividend dates…I hear you say!

Correct. But I assure you, this is indeed the perfect time to start thinking about the deluge of dividends about to be paid in March and April, particularly for those who wish to investigate the dividend stripping strategy.

Dividend stripping is a long-time favourite of Aussie income investors who, like great white sharks, roam the ASX dividend ocean on the hunt for big, fat, juicy dividends. But (do a Sir David Attenborough voice in your head here…) the ASX dividend investor is not only interested in finding those juicy dividends, they want the lucrative franking credits that come with them as well.

Get a grip on the strip

Dividend stripping involves buying shares in a company prior to the ex-dividend date and selling those shares after the ex-dividend date. The goal is to capture the dividend and any associated franking credits. In some cases, the share price in question may not fall as much as the dividend-franking credit combination, yielding an instant profit.

Some investors choose to hold until they’ve recouped all the share price fall that comes after a company goes ex-dividend and try to make the entire dividend-franking credit profit. Once the trade is complete, dividend strippers move on to the next, and next dividend stripping opportunity.

Before we get into the next bit, which is essential information for ASX dividend strippers, I’d better just cover a few definitions for beginners (to save you googling elsewhere!).

Dividend = A portion of a company’s profit its management may choose to distribute to shareholders. Most major ASX-listed companies pay dividends twice a year, based upon their half and full year reporting schedule.

Declaration date = When the company declares the dividend, generally when the company reports its earnings, will include the amount of the dividend, the degree to which the dividend is franked (e.g., 0% (unfranked), 50%, 80%, 100% etc.), and important other dates like the ones below.

Ex-dividend date = On this day, the shares trade without entitlement to receive the dividend. Anyone who purchased shares prior to the ex-dividend date is entitled to receive the dividend, whereas anyone who purchases shares on or after the ex-dividend date is not entitled to receive the dividend.

Record date = Usually occurs the next business day after the ex-dividend date, administrative only, the company paying the dividend will pay the dividend to those recorded on their share register on this date. Rest assured, if you purchased your shares prior to the ex-dividend date, you will be on the register.

Payment date = When dividend moneys are disbursed to registered shareholders. This usually occurs a few weeks after the ex-dividend date, and it could take a couple of weeks extra for the money to finally hit your bank account.

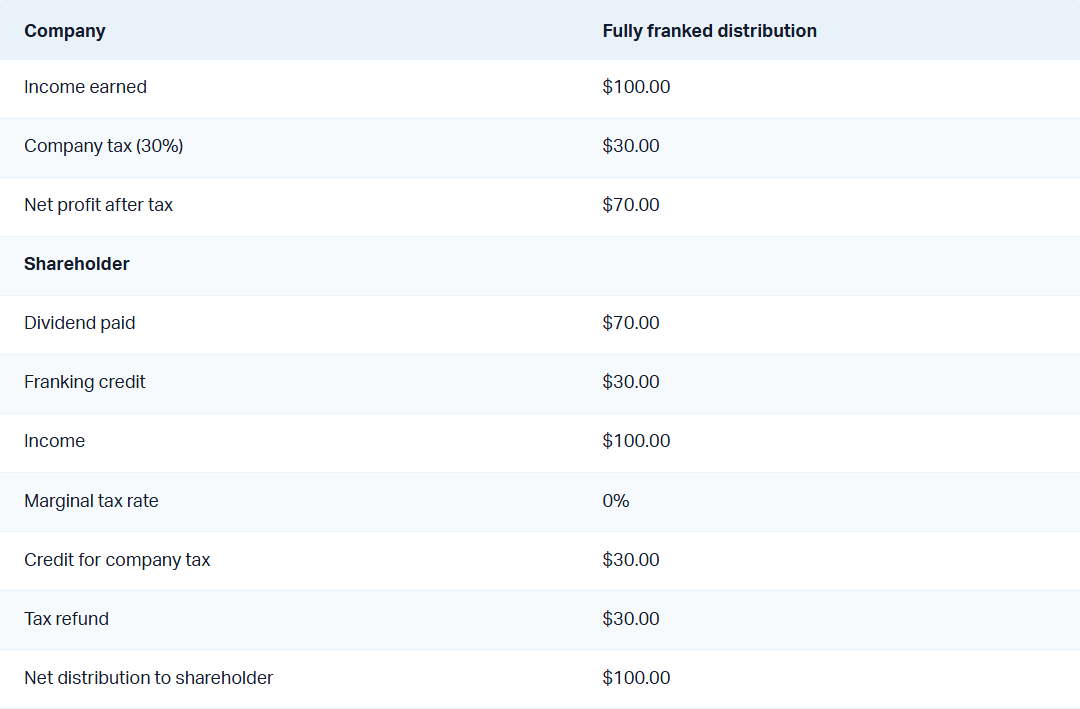

Franking Tax Offset (“Franking Credit”) = System to prevent double taxation on dividends paid to Australian investors. When a company pays corporate tax on its profits, it can attach franking credits (representing that tax paid) to the dividends it distributes. Shareholders then use these credits to offset their own tax liabilities, effectively receiving credit for the tax already paid at the company level. If the franking credits exceed the shareholder’s tax bill, the excess may be refunded.

The fly in the dividend stripping ointment: The 45-Day Rule

Based on that last definition, franking credits are potentially extremely lucrative to those on low or zero marginal tax rates, like pension-phase superannuation funds – essentially making them as valuable as the dividend itself.

There are some extra rules, though, and it’s best to check these with your financial services professional, but consider how franking credits work for an investor on a zero marginal tax rate:

Wouldn’t it be great if you could buy shares in a company the day before it goes ex-dividend, and then sell it on the ex-dividend date and immediately scoop up the dividend and any associated franking credits? It would, but you can’t* – or at least you can’t and still be entitled to the franking credits!

The Holding Period Rule, also known as the “45-Day Rule”, requires Australian resident taxpayers to hold shares at risk continuously for at least 45 days (90 days for preference shares), not including the day of acquisition or disposal. So, in theory, if you want to strip a dividend plus its franking credits, you’ll be at least partially at risk by owning the company’s shares for at least 47 days.

As we’ll see in a case study below, this creates substantial risks for dividend strippers. For now, also note that if you’re adding to an existing parcel of shares and looking to strip just those, any shares sold as part of the dividend strip are considered on a last in-first out method.

*Note: Under the "Small Shareholder Exemption" the 45-Day Rule does not apply if an investor's total franking credit entitlement is below $5,000. This is roughly equivalent to receiving fully franked dividends of $11,666 during the financial year (for companies with a corporate tax rate of 30%)

Dividend strip case studies and risks

Case Study 1: Quick Strip

Assume Sarah's total franking credit entitlement for the current financial year is greater than $5,000. She buys 10,000 shares in BHP on March 5 for $45, the day before it goes ex-dividend for a $1.00 fully franked dividend. Sarah sells her shares on March 6, the ex-dividend date, for $44.50, realising a $0.50 or $5,000 capital loss. She receives the dividend of $10,000 on March 31.

Putting aside any transaction or holding costs, Sarah has made a net profit of $5,000 on her dividend strip – but she will not be entitled to claim the $4,285.71 franking credit because she did not hold her BHP shares at risk for the 45-Day Rule period.

Case Study 2: 45-Day Rule Strip + Win

Assume all of the same details as in Case Study 1, but this time Sarah sells her shares just after the open of trade on 21 April. Because she has held for 45 days, not including her purchase and sale date (March 6 plus 45 days = 20 April), Sarah can now claim the franking credit in her next tax return.

Here are Sarah’s outcomes based on a few possible marginal tax rates:

0% Marginal Rate

- Tax on $14,285.71 at 0% = $0

- Subtract franking credit ($4,285.71) from this tax = $0 – $4,285.71 = –$4,285.71 (i.e. $4,285.71 refund)

16% Marginal Rate

- Tax on $14,285.71 at 16% = $2,285.71

- Subtract franking credit ($4,285.71) from this tax = $2,285.71 – $4,285.71 = –$2,000 (i.e. $2,000 refund)

30% Marginal Rate

- Tax on $14,285.71 at 30% = $4,285.71

- Subtract franking credit ($4,285.71) from this tax = $4,285.71 – $4,285.71 = $0 (i.e. no additional tax)

37% Marginal Rate

- Tax on $14,285.71 at 45% = $5,285.71

- Subtract franking credit ($4,285.71) from this tax = $5,285.71 – $4,285.71 = +$1,000 (i.e. $1,000 additional tax to pay)

45% Marginal Rate

- Tax on $14,285.71 at 45% = $6,428.57

- Subtract franking credit ($4,285.71) from this tax = $$6,428.57 – $4,285.71 = +$2,142.86 (i.e. $2,142.86 additional tax to pay)

Case Study 3: 45-Day Rule Strip + Strip Loss

Sarah buys 10,000 shares in BHP on March 5 for $45, the day before it goes ex-dividend for a $1.00 fully franked dividend. Sarah sells her shares on April 21 for $43.00, realising a $2.00 or $20,000 capital loss. Sarah receives the dividend of $10,000 on March 31. Sarah’s marginal tax rate is 0%, and so she is entitled to a $4,285.71 tax refund in her next tax return.

Putting aside any transaction or holding costs, Sarah has made a net loss of -$5714.29

This last case study demonstrates the key risk associated with the dividend stripping strategy – the 45-Day Rule means there’s very little certainty as to the final sale price for those who wish to get the full benefit of any franking credits attached to a dividend. This means that losses incurred during the minimum holding period could be substantial.

Dividends you might want to strip this earnings season

ASX-listed companies pay some of the juiciest dividend yields among any share market in the world. We have some of the strongest and most reliable blue-chip companies that, in many cases, have long track records of paying dividends.

History suggests that share prices generally tend to rise over the longer term, often recouping in share price any dividends paid. Add in the bonus of Australia’s franking credit regime – and dividend stripping is potentially a very effective strategy for Australian investors, particularly for those on low or zero marginal tax rates.

But there are clear risks for those investors who wish to capture dividends and franking credits due to the 45-Day rule. For this reason, one cannot simply focus on those companies with the highest dividend yields and rates of franking, but rather, those companies most likely to hold or improve their values after dividends are paid.

With literally hundreds of ASX companies set to go ex-dividend in March and April, and given the 45-Day Rule, now is the perfect time to consider which dividends to attempt to strip. So, in tomorrow’s follow-up, we’ll investigate which companies are set to pay the juiciest dividends this earnings season, and roughly when you’ll need to buy their shares to stay on the right side of the 45-Day Rule. Stay tuned!

This article first appeared on Market Index on Wednesday 8 January 2025.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

4 topics

13 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment