Indexed annuity bonds offer steady income and help build the nation

Elizabeth Moran

Elizabeth Moran Consulting

Here I suggest five Indexed annuity bonds that are perfect for retirees looking for low risk, stable additions to their portfolio as well as helping meet minimum withdrawals for SMSFs in drawdown.

If you are retired you must actually use a set amount of your super each year. It’s called a drawdown.

Three of the biggest problems faced by SMSFs in drawdown are: building a reliable cashflow, making sure money lasts, and protecting against inflation.

Indexed annuity bonds are an ideal solution to all three of these significant problems and more.

Let me explain. Indexed annuity bonds have been issued by public private partnerships or joint ventures to help fund the construction and maintenance of important infrastructure projects such as schools, universities, hospitals, railway stations, government buildings and even water treatment plants.

The bonds were issued years ago in the over the counter bond market and are very long dated.

The entities typically receive payments from the state or federal government, making them very low risk investments.

An index annuity bond works like a reverse mortgage - investors pay a lump sum up front which is then returned over the life of the bond in quarterly payments that include both a principal and interest component. These periodic payments are increased each quarter to reflect inflation, which is particularly valuable to retirees wanting steady income with the added inflation protection. The value of your investment is paid down over the life of the bond. The bonds act like an annuity although there is no lifetime cover. Instead, they have a maturity date.

Also, importantly, they can be used in estate planning and left to beneficiaries in your will.

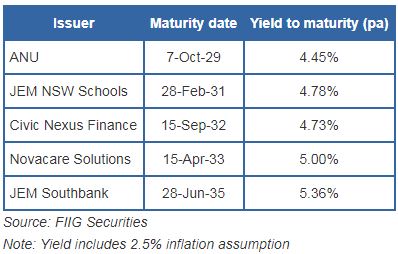

One example is Australian National University. In 2004, ANU issued a $115m indexed annuity bond, maturing on 7 October 2029, to fund growing capital expenditure (including re-development of the John Curtin School of Medical Research and renovation of the Research School of Physical Sciences and Engineering).

It was issued with a $100 face value but it has been repaying principal since 2004 and the current principal outstanding, which includes the effect of inflation since 2004, is around $78. A new investor needs to pay more, close to $84 as these bonds have become sought after for high yields given very low risk. The projected yield to maturity on these bonds is 4.4 per cent per annum, which includes a 2.5 per cent annual inflation.

Let’s assume an investor starts with an $84,000 investment today. The bond would pay its first full quarterly payment in October and would return $2,055, then again in January 2019 $2068, in April $2,081 and in July $2,094.

Notice how the payment is increasing. This is because our model assumes positive inflation at the Reserve Bank midpoint target of 2.5 per cent per annum. Lower inflation would mean lower payments and higher inflation, higher payments. Payments would continue until October 2029 when the last payment, projected at $2,704 would be paid.

In total, 45 payments would be made over 11 years, providing a reliable cashflow to the SMSF. The bonds would also provide an inflation hedge, and an investment that returns capital, so would help meet minimum withdrawals amounts from the SMSF in drawdown. Magic!

Young retirees might look at longer dated options such as JEM Southbank maturing in 2035, a wholly owned special purpose finance vehicle majority owned by funds managed by AMP. The original finance was used for the construction and operation of the Southbank Education and Training Precinct for the Queensland government under a private public partnership. This bond has a projected yield to maturity of 5.35 per cent per annum.

Investors thinking about a portfolio of these bonds could also look to add Civic Nexus, where funding was used to build the Southern Cross Railway station in Melbourne, Novacare, which was contracted by the NSW Department of Health for the financing, design, construction and refurbishment of various facilities at the Mater Hospital in Newcastle and Jem Schools, the financing vehicle contracted to finance, design, construct, maintain and manage 11 schools in NSW.

There are about eight of these bonds available to retail investors, which are perfect for SMSF retirees. We haven’t seen any new issuance for some time, which is a great shame. Like other bonds, they can be bought and sold in the secondary market. They make great, low risk, stable additions to any portfolio and present good relative value.

As published in The Australian on 23 June 2018

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

7 topics

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Comments

Comments

Sign In or Join Free to comment