Is the stock market in a bubble?

It has been about 10 years since the Global Financial Crisis (GFC) began to unfold. Very few were prepared for the financial damage that ensued. And it has permanently impacted the psyche of many market pundits. Since then, there has been no shortage of bear market predictions and lately there has been a lot of fearmongering in the media.

Several commentators have pointed to some well-known US fund managers struggling to match the performance of the US market. If they are finding it difficult, why wouldn’t you think a bear market is imminent? For example, the US stock market has well and truly surpassed its pre-GFC highs and it continues to break all-time highs nearly every single quarter. Plus, most of the market gains in the US have been driven by technology stocks and much has been written about the rise of the FANG stocks Facebook, Amazon, Netflix and Google.

However, the acronym should really be FAAAM (although it does not have the same ring) to represent the five largest stocks in the S&P 500 – Facebook, Apple, Alphabet (aka Google), Amazon and Microsoft. Their combined market capitalisation is about $3 trillion and given their lofty prices, some observers are pointing to similarities with the technology bubble in 1999/2000.

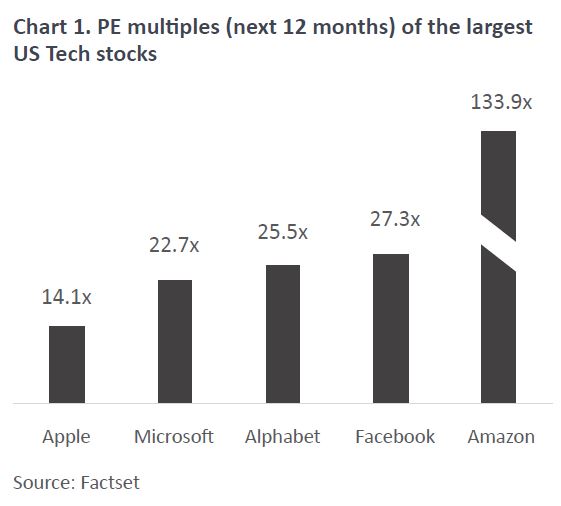

Prices are one thing, but value is another. Typically, rich valuations are a precursor to bubbles bursting. The following chart displays the current price earnings multiples of the technology juggernauts.

Apart from Amazon, their current PE multiples look a little expensive but do not suggest a bubble. Moreover, the global MSCI tech sector is trading at around 20x, which is a far cry from the tech bubble peak of 50x. During the technology bubble, not only were technology stocks dangerously expensive, but they were also cash hungry. Fast forward to today, the FAAAM stocks in the coming year are expected to hold more cash (about $444 billion combined) than the GDP of some countries.

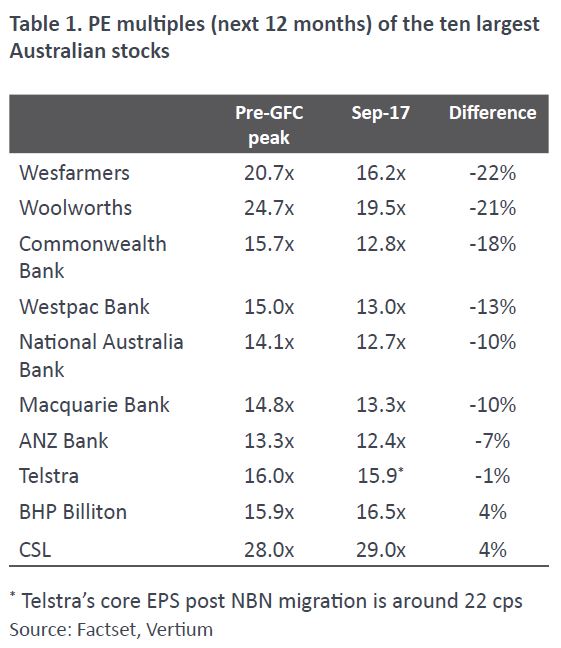

How about valuations in the Australian stock market? Like in the US, some Australian fund managers have found it difficult to outperform this year. Is their performance also signalling an imminent bear market? To get a sense of valuations, the following table highlights the PE multiples of the ten largest stocks in the Australian market at the end of the September quarter compared to their pre-GFC peak.

Compared to 10 years ago, with a couple of exceptions, most stocks have valuation multiples trading well below their pre-GFC highs. Sure, earnings growth in the post-GFC world is lower for some companies which may justify lower valuation multiples. However, interest rates have also halved over the same time frame which should raise valuations. Overall, lower valuation multiples indicate that euphoria, a necessary condition for market bubbles, is lacking.

Bubble or bear market predictions often get a lot of attention, but the canary in the coal mine – valuation multiples – are not yet signalling that we should worry. While we do not know where market prices will be in a year’s time, we do know that the starting point helps determine the future outcome: the lower the valuation multiple, the lower the chances of a market correction.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

11 topics

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Comments

Comments

Sign In or Join Free to comment