JB Hi-Fi: What the market missed

Chad Slater

Ellerston Capital

The most important data in the report was that margins didn’t expand as much as the “Whisper number” thought they would. Firstly, what is the “whisper number?” Most readers will be aware of what is called “the street's expectation” – which is the forecasts that the sell side brokerage houses have for a result. This is why readers often see the perplexing situation where a company says “earnings up 30%” for example and yet they see the stock down – the street thought they would earn more than 30% and that was in the share price.

However, there is also the whisper number. It’s the number that people think may happen, but the broker hasn’t upgraded the number to that level yet.

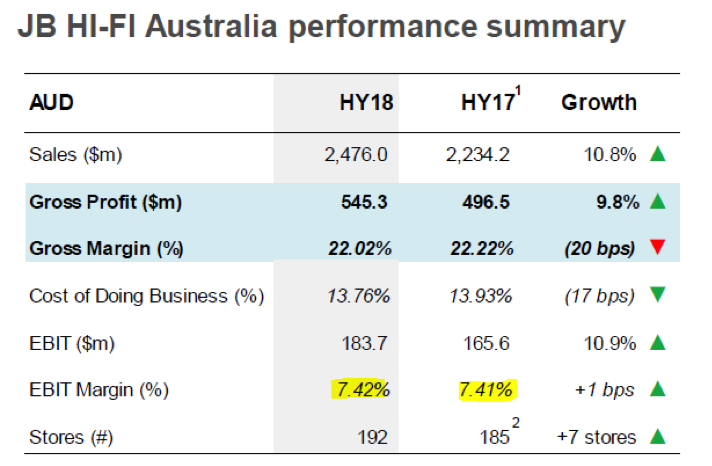

In JB Hi-Fi’s case, there were a lot of stories about how well trading had done over Christmas and early January. This turned out to be true: sales for example in November and December for JBH Australia was backed out to be circa 9% growth – a great result in what is considered to be a market with no real growth.

The issue, returning to the first line, is that most analysts would assume there to be operating leverage whereby sales translates into more higher EBIT margins. It turns out that there was no expansion in margins for JBH Australia.

The other “Whisper” was that they would upgrade synergy forecasts for the Good Guys acquisition. The theory being that the management of any acquisition would forecast low, and then upgrade. JBH told the market they were keeping their expectations the same. This also impacts margin forecasts. This is probably a good thing longer-term as for a supplier there is nothing worse than giving a customer a bigger discount to see all of it taken as profit, rather than growing the supplier’s sales. The old Woolworths was a past master at hitting up suppliers for margin when needed. It doesn’t engender great long-term relationships.

Our view on the stock after today

Given we presented it on BuyHoldSell, it comes as no surprise we thought the stock would do well and had a positive view on the stock. Has it changed in light of the result? Yes, at the margin it has to: when you forecast something to happen and it doesn't, one must re-calibrate and accept that the reality isn’t quite what you thought.

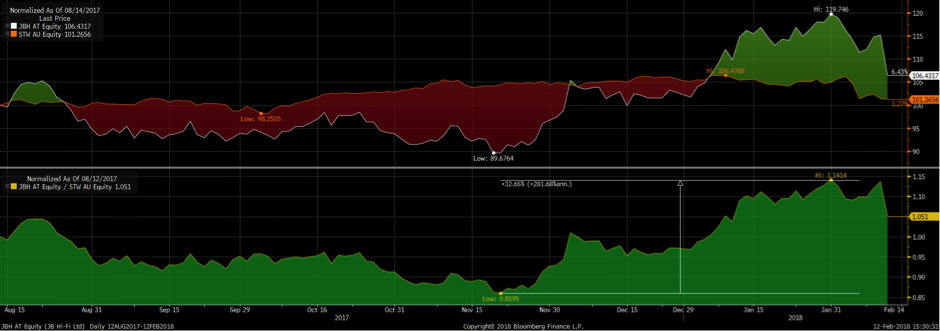

Having said that, some perspective is needed: Off its October lows, the stock had outperformed the market by 32%. Even after today’s fall, it has beaten the market by 7% this year. The issue for the stock price was at $30, it needed an upgrade to justify that size of rise.

Whilst there are many bears on the stock, today’s fall does little to fix their P&L on losses. One could even argue that how little it has given back of the gain is a warning to the bears.

But today was their day – let them enjoy it.

Three things the market is missing about this company

A lot of the above is minutiae and short term. If we take a step back though, firstly, one sees a management team that marginally grew EBIT margins in the core Australian business into a backdrop of Myer’s profit woes and did it without pushing up the Gross Profit margin (which would suggest price gouging). I would suggest even a bear should begrudgingly acknowledge management that.

Further, management isn’t focused on playing the short-term game. As they say – “retail is detail” and these guys have done a good job. One has to feel for them being quizzed by a twenty-something on the call who has never run a business about why they haven’t upgraded synergy forecasts for the next 6 months. They are integrating a large acquisition of another business that will improve market share and buying power over the coming years.

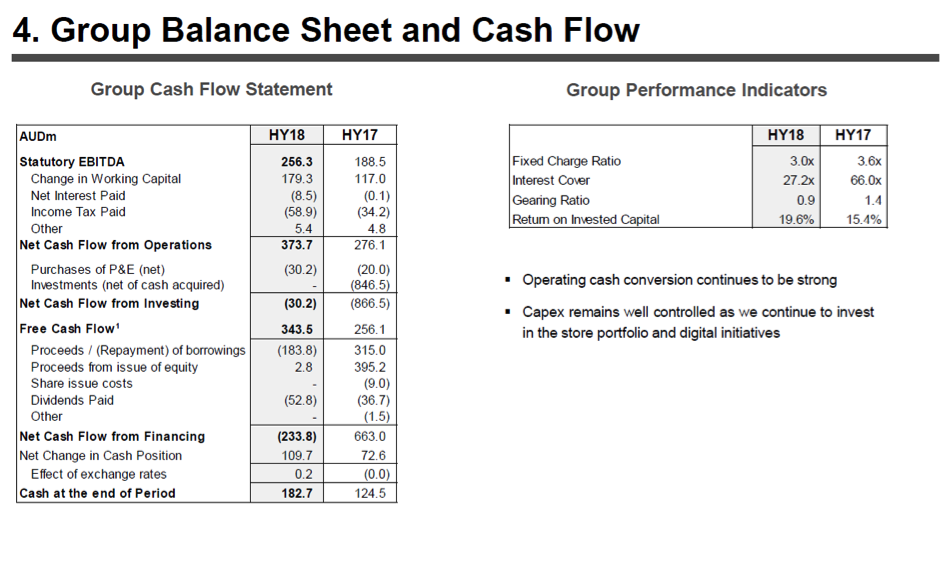

The last thing I think being overlooked today is the level of cash generation. They took on debt for the GG acquisition, and even allowing for some timing on Christmas inventory, cash conversion rates are good with net debt falling to $192mn from $486 (it will rise over the coming half).

For further insights from Morphic Asset Management, please visit our blog

For further insights from Morphic Asset Management, please visit our blog

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chad co-founded Morphic Asset Management in 2012. As a stock picker Chad is also a generalist but has strong regional knowledge of Europe and the Americas. He has also been awarded the CFA Charter.

3 topics

1 stock mentioned

Chad Slater

Co Head Global Equities (ex-Asia)

Ellerston Capital

Chad co-founded Morphic Asset Management in 2012. As a stock picker Chad is also a generalist but has strong regional knowledge of Europe and the Americas. He has also been awarded the CFA Charter.

Expertise

Chad Slater

Co Head Global Equities (ex-Asia)

Ellerston Capital

Chad co-founded Morphic Asset Management in 2012. As a stock picker Chad is also a generalist but has strong regional knowledge of Europe and the Americas. He has also been awarded the CFA Charter.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management