Key themes and takeaways from AREIT reporting season

It was a solid reporting season for the AREIT sector. In this wire, we review the performance, pull out the key themes to emerge, and identify ten specific takeaways from the retail, office and industrial sectors.

Let’s get the big takeaway in first. This was a rather good reporting season. Unfortunately, short term share price volatility is pushing this simple fact into the background. Between July 1st and December 31st last year, the total return (that’s capital growth plus dividends) of the S&P/ASX 200 AREIT Accumulation Index was a healthy 9.8%, outperforming the S&P/ASX 200 Accumulation Index by 1.4%.

Then US bond yields jumped by a third, prompting a fall in AREIT prices. In the first two months of this year, the AREIT sector’s total return declined by 7.0%, versus the equity market which has been flat over this period. Falls of this ilk get attention but are small beer for genuine long-term investors. In fact, they’re often an opportunity.

Anyone with an eye on long term performance should take reporting season as an opportunity to re-examine their investment theses and check whether everything is on track. What they should not be doing is making assumptions about the future based on short term swings in share prices.

What does this mean in practice? Well, income-focused managers like us concentrate on the factors that support the sustainability of income – rental growth, occupancy and asset values. Which is a polite way of saying we have little regard for short term total index returns and US 10-year bond yields than we do net operating income (NOI), NOI growth, occupancy and asset values.

In that regard, this reporting season was, just like last time around, rather good. The outlook for distribution guidance for every AREIT in which we invest was either re-affirmed by management or upgraded.

The interim results certainly supported prospects for continued delivery of the defensive income returns our investors are seeking.

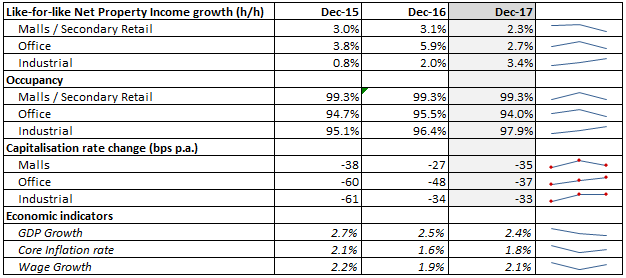

These satisfying results were achieved despite a domestic economy still stuck in second gear. The table below (calendar year) shows GDP growth, core inflation and wages growth lower than it was two years ago, as was the case in the reporting season covering the 2017 financial year.

Source: JP Morgan, Trading Economics, APN FM

However, this has not inhibited operating performance. The retail, office and industrial sectors each delivered positive comparable net income growth of between 2.3% to 3.4% to 31 December 2017 whilst maintaining high occupancy levels. This performance, along with capital and investment market dynamics, was also reflected in rising AREIT book values.

So, all good so far. Let’s now look at some specific takeaways from each sector:

Five takeaways from the retail sector

- Retail asset valuations increased by 4.2% for the half, driven by a number of property sales completed last year. This gives us confidence that book values are real and justified.

- Net property income growth in retail continues to keep pace with GDP growth. It would be a worry if net property income growth were much lower (or higher) than GDP growth. But it isn’t, and that suggests it’s sustainable.

- High quality malls are doing just fine, attracting profitable and growing retailers. Last calendar year, for example, Scentre Group let a total of 1,258 stores. This included 289 new brands and 592 existing retailers opening a further 943 stores across a portfolio of 39 assets. So much for the retail apocalypse.

- Total sales growth – as represented by Moving Annual Turnover (MAT) – improved by 20 basis points (bps) over the half year, coming in at 2.0%. Many AREITs also spoke of strong trading conditions in December persisting through January. Unsurprisingly, department stores recorded negative growth while mini-majors (like Sephora and JD Sport) recorded the strongest. We expect this trend to continue. Investors in the country’s best malls, APN AREIT investors included, have nothing to fear.

- While sales growth for specialty retailers slowed modestly, there were no signs of tenant weakness from arguably the most fundamental of measures – rental arrears. Of the major retail landlords surveyed, each noted tenant debtors remained in line with historical averages. With extremely high occupancy and tenants continuing to pay rent, the prospects for rental growth from this segment are good.

Three takeaways from the office sector

- The story of rental growth continues in the eastern-seaboard markets of Sydney and Melbourne, the cities in which most AREIT office landlord portfolios are concentrated. To 30 June 2017, effective rents were up about 20% in Sydney and half that in Melbourne (JLL) while Brisbane and Perth remained weak. This was good news for APN’s AREIT Fund, which is focused on the Sydney and Melbourne markets.

- The table above shows that net property income growth in the office market was 2.7% in the first half of the 2018 financial year, a decline on the prior period. This isn’t anything to worry about. Some office landlords were impacted by one-off tenant movements and expiries. Due to the term of an office lease (generally 3-5 years or more), market-based rent reviews do not occur annually. This means the protection a lease provides when rents decline can also limit a landlord’s ability to participate in strong rental growth.

- This leads to our final point. Whilst high occupancy levels and long Weighted Average Lease Expiry (WALE) profiles are desirable, they’re less important when rents are rising. Landlords in Sydney and Melbourne will have to wait before marking their leases to market rents but it will happen. AREIT investors will eventually get their fair share of rising rents.

Two takeaways from the industrial sector

- Compared with previous periods, net property income growth in industrial was the highest across the major AREIT sectors at about 3.4%. This occurred despite subdued economic activity and a rising Australian dollar making life difficult for exporters.

- Landlords enjoyed the benefits of tightening occupancy levels and strong market rental growth driven by expanding e-commerce and third-party logistics tenant demand. High quality industrial space located in urbanised metropolitan markets remains in tight supply, which will boost demand for such assets held by the industrial landlords in which we invest.

Whilst the residential sector accounts for only a small part of the AREIT sector, there were a few notable points. Despite a slowdown in sales volumes, Stockland may upgrade its profit margins from the previous 15% to a healthier 17% over the near term, a result of strengthening prices for residential land in major markets. Mirvac Group, with a broad exposure to high-rise apartments, reported an increase in pre-sales and increased profit margin guidance.

Major themes offering comfort to investors

Starting with the very thing that has brought the sector undone in the past.

Asset values continue to (justifiably) rise

Have we hit a peak in retail commercial property? We don’t believe so. The capitalisation or cap rate – the ratio of net operating income of a property to its market value – is a measure of the percentage return to an investor that purchased a property for cash. The above table shows that while the pace of capitalisation rate compression moderated through the period, this reporting season still delivered good results with tightening across all major sectors.

Retail malls saw cap rate falls of 24bps in this half year period alone. Scentre Group experienced 35bps falls to 4.91% and Vicinity 30bps to 5.45%. That may not sound significant but it contributed an additional $2.7 billion in upwards asset revaluations. Why? Because as cap rates fall, valuations rise. This re-affirms our view that, largely due to a lack of transaction evidence, the country’s highest quality, fortress-malls remain undervalued.

Both the office and industrial segments of AREIT portfolios also enjoyed valuation increases through the period, led by cap rates falling 17bps and 21bps respectively.

The evidence suggests asset valuation increases are justified and may continue.

Capital allocation is creating value

Capital management and efficient allocation of excess gearing capacity was again front and centre. Balance sheet gearing continues to fall with those property trusts within our coverage universe disclosing gearing of just 28.2%.

When one considers balance sheet strength and the fact that many AREITs are trading at discounts to book value, we as investors question company plans to close the gap between book values and share prices.

For Dexus and Mirvac Group, additional developments or acquisitions presumably appear less compelling. Instead, both will be buying back their own shares. This is a welcome vote of confidence by AREIT boards in the value of their portfolios.

The same cannot be said for Investa Office Fund and Vicinity Centres. Our interactions with management and further investigations suggest both might be looking to create greater value from relatively riskier acquisitions or development activities, rather than buy backs. Investors can be sure we’ll be monitoring these two AREITs closely.

Outlook

All up, this reporting season offered compelling evidence that the reasons why we hold the stocks we do remain strong. Still, any kind of investing entails some risk, and sensible investors constantly measure and monitor what those risks are.

For property trusts, modest growth in retail sales is the worry. Many commentators put this down to Amazon’s arrival and poor retail management. Anaemic wages growth is a better explanation. Without that we cannot expect much in the way of retail sales growth. This is an indicator on which we’re especially focused.

Overall, this reporting season offered convincing evidence that the AREIT sector remains an attractive option for income-focused investors.

This position is endorsed by JP Morgan, which forecast AREIT earnings growth of 3.8% for the current financial year and distribution growth of 3.0%.

This, along with the sector currently trading at a discount to NTA (excluding Westfield and Goodman Group), suggests our expectation that the sector will deliver a total return of between 8-12% over the next 12 months is on the money.

Outside of those sleeper risks that, in the main, are notoriously difficult to predict but when awakened scare all markets, insights from this reporting season only makes us more confident of meeting that goal.

Interested in real estate?

Check out our blog to access analysis and insights from the experienced team at APN Property Group.

This article has been prepared by APN Funds Management Limited (ACN 080 674 479, AFSL No. 237500) for general information purposes only and without taking your objectives, financial situation or needs into account.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Mark is part of the Investment Team tasked with analysing and investing in global real estate-sector equities. He is an Associate of the Australian Property Institute, a Certified Practicing Valuer and a CFA charterholder.

3 topics

6 stocks mentioned

Mark is part of the Investment Team tasked with analysing and investing in global real estate-sector equities. He is an Associate of the Australian Property Institute, a Certified Practicing Valuer and a CFA charterholder.

Expertise

Mark is part of the Investment Team tasked with analysing and investing in global real estate-sector equities. He is an Associate of the Australian Property Institute, a Certified Practicing Valuer and a CFA charterholder.

Expertise

Comments

Comments

Sign In or Join Free to comment