Lessons from the crash: property trusts 10 years on

Matthew Coleman

Dexus

‘Those who do not learn from history are condemned to repeat it’. So said Spanish-American philosopher George Santayana.

This saying has not been lost on the Australian real estate investment trust managers. The sector, much to the relief of income-focused investors, has learnt much from the mistakes that hurt so many investors during the global financial crisis (GFC) a decade ago.

It’s instructive to understand how. A leading factor that led to the widespread collapse in property trust prices during the GFC was the high level of debt, which fed ill-conceived property purchases and unsustainable investor distributions.

You may remember the names; Macquarie DDR Trust; Macquarie Countrywide; Babcock & Brown Japan Trust; and Tishman Speyer Office Trust. All carried debt levels of between 50-60%, all are now gone.

As the crisis unfolded readily available credit evaporated, property valuations moderated and banks introduced restrictive loan covenants, subsequently breached by many REITs. To meet creditor demands, they sold high quality assets at reduced prices and raised capital at significant discounts to their underlying asset value. When the tide turned it did so quickly.

The subsequent price falls were swift and unforgiving. Many REITs collapsed under the covenant and debt burdens, others merged or were acquired.

The first place to look as to whether the lessons have been learned is in current debt levels. Cromwell Property Group, for example, carries a gearing ratio of around 44%, Growthpoint 40% and Centuria Industrial and ALE Property Trust 43%.

We’d suggest this is no reason to panic although it’s certainly worth focusing on – higher debt levels will require us to earn a higher equity yield to own these REITs. Most AREITs have reduced their debt levels significantly over the past decade and none have a gearing ratio above Cromwell’s 44% (in the last few days, Cromwell has even completed an equity placement with the proceeds bringing this figure down further). In 2007, the S&P/ASX 300 A-REIT Index was geared at around 40%. Now it’s around 28%, the fall assisted by asset sales and rising valuations of underlying real estate assets.

Since the GFC, most AREIT managers have also diversified their debt sources away from domestic banks, recapitalising through equity capital raisings and sourcing new lines of credit from offshore banks and bond markets. This has resulted in lower gearing levels and a diversified debt book.

Recently, large cap AREITs including GPT, Goodman Group and Mirvac have all issued long term debt at attractive rates through the bond market. Any shareholder concerns regarding AREIT debt appear not to be shared by bond market investors. That’s another big tick.

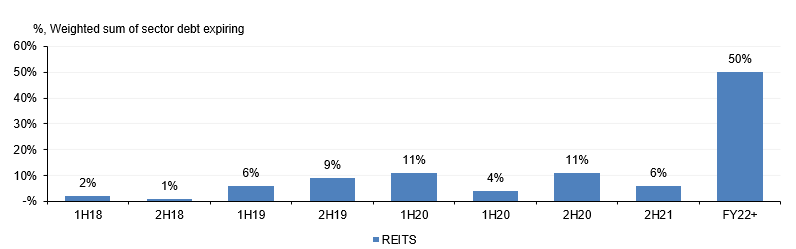

The sector has also extended the average duration of debt to over five years as of 30 June 2017. As the chart below shows, this financial year only about 3% of debt is due to expire. In each of FY19 and FY20, about 15% expires. In fact, over 50% of debt expires in five years’ time and beyond.

Extended Debt Maturity Profile Across the Sector

Source: APN Property Group company data, June 2017

This is a debt burden easily managed, contrasting starkly with the period prior to the GFC when average debt expiry terms were around 2.5 years1. Today’s average debt expiry profile highlights little short-term refinance risk, offering downside protection in the event of any market shocks.

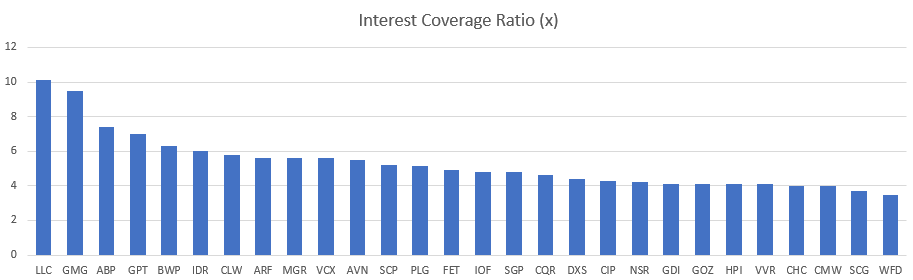

The third factor that mitigates the debt risk is an increase in the interest coverage ratio (ICR), a measure of a REIT’s ability to pay interest expenses on its outstanding debt as a multiple of earnings.

In March 2009, the ICR for the sector averaged 2.9 times earnings2. As at June 2017, it was 5.4 times. Property trusts now have a much greater ability to cover interest payments using earnings. The chart below shows the clear variance in the ICR across the sector. All REITs feature ICRs well above those seen prior to the GFC – even allowing for today’s low interest rates the metrics are very healthy.

Stronger Interest Cover Across the Sector

Source: APN Property Group company data, June 2017

Finally, AREIT managers have taken advantage of lower interest rates, raising new debt or refinancing existing arrangements at a lower cost. This has led to improved cashflows and value-enhancing property acquisitions where yields on the properties purchased are higher than the interest rates on the loans that finance them.

These four data points offer sound evidence that the sector has learnt the lessons of the GFC. As a consequence, the temptation to gear up to acquire more assets with cheap debt has been generally resisted.

For property trust investors this is good news. If markets turn and costs rise, AREITs will enjoy a level of protection they lacked during the GFC.

As long term investors in commercial real estate we welcome the return to prudent capital management and long-term sustainability. It’s taken a while but property trusts have returned to what they do best – delivering steady income and modest capital growth to risk averse investors. In this sector at least, we doubt history will repeat.

Did you enjoy that?

Check out the APN Property Group blog for more articles covering a range of real estate investment topics.

This article has been prepared by APN Funds Management Limited (ACN 080 674 479, AFSL No. 237500) for general information purposes only and without taking your objectives, financial situation or needs into account.

1. Source: Macquarie

2. Source: BAML, 2012

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matthew is tasked with analysing and investing in Australian property trusts.

He brings fundamental property knowledge, experience across a number of property sectors and a genuine interest in the AREIT sector.

4 topics

1 stock mentioned

Matthew Coleman

Analyst, Real Estate Securities

Dexus

Matthew is tasked with analysing and investing in Australian property trusts. He brings fundamental property knowledge, experience across a number of property sectors and a genuine interest in the AREIT sector.

Expertise

Matthew Coleman

Analyst, Real Estate Securities

Dexus

Matthew is tasked with analysing and investing in Australian property trusts. He brings fundamental property knowledge, experience across a number of property sectors and a genuine interest in the AREIT sector.

Expertise

Comments

Comments

Sign In or Join Free to comment