Myer: Winter is coming

Daniel Mueller

Vertium Asset Management

What do Amazon, Buffett and Sydney CBD retail have in common? You know about Amazon and its potential to destroy retailers. While Amazon’s Australian launch last December was somewhat underwhelming, one could consider it a ‘soft’ launch. Whether it’s next year or next decade, odds are Amazon will get its offering right. It plays the long game.

You may know Warren Buffett has personally bought a significant stake in Seritage Growth Properties (the REIT spin-off of Sears Holdings). On the surface, this is a puzzling investment with Seritage’s earnings largely tied to the fate of Sears.

You may not know what is happening in the Sydney CBD retail district. Scentre Group (the REIT that owns Australian Westfield shopping centres) bought the David Jones building on Market Street in August 2016. This asset sale in isolation may seem insignificant. But here we find a close parallel to what is happening with Seritage and Scentre. At the centre of both REITs is the downfall of their incumbent department store retailer.

Battle lines drawn

Between Amazon’s entry into Australia and Scentre’s acquisition of the David Jones building, we have just seen the first shots fired in what is likely to become a multi-year ‘pincer movement’. And the target of this movement – Myer Sydney City.

But wait just a moment. Myer is a major tenant of Scentre’s Sydney city property, which raises a lot of questions. How would Scentre hasten its demise?

Can’t wait 10 years to find out how this plays out? Then let’s hit the fast forward button and look across the Pacific to the US, which foretells what might happen.

Looking across the Pacific

Seritage Growth Properties is the REIT spin-off of Sears Holdings, owner of retailers Sears and Kmart. It listed in July 2015 and has 230 wholly-owned properties leased to either Sears or Kmart. As part of the spin-off’s master lease agreement, Sears Holdings stores have favourable terms, currently $4.44 per square foot compared to $15.03 per square foot for third-party leases.

Like Myer, Sears has been struggling in recent years. If not for several loans from billionaire CEO, Eddie Lampert, it may not be around today. Sears’ share price has declined 92% over the past four years, with the company being unprofitable since 2012. In that time, sales have halved and store numbers have dropped from just over 4,000 to under 1,500.

Surely this would be a major negative for Seritage?

Not so fast.

The more unprofitable Sears becomes, the easier it is for Seritage to reposition its properties from the anchor tenant to other retailers willing to pay substantially higher rent.

Seritage is making steady progress diversifying away from Sears as its main tenant. When Seritage first listed, Sears Holdings comprised 93% of its floor space and 81% of its rent. Fast forward to today and Sears comprises 80% of its floor space but more importantly just 55% of its rent. Seritage benefits from the removal of underperforming Sears stores and replacing them with tenants who pay higher rent. This will be a crucial driver of earnings growth. The Seritage story is so compelling that it has attracted famed investors Warren Buffett, Bruce Berkowitz and Mohnish Pabrai onto its register.

Which brings us back to Scentre and Myer.

Australian version of Sears and Seritage

Like Sears, Myer’s recent history has been tumultuous. Since relisting as a stand-alone business in November 2009, its share price has decreased by 87% and the company has slowly reduced its store footprint. While it has managed to turn a profit each year, 2017 NPAT of $69m is almost $100m less than what the company earned in 2010.

At its November 2017 strategy day, Myer warned that 19 of its 63 stores were at risk of closing if sales failed to improve. However, there was no question over it vacating flagship stores like Sydney City. But based on the rental income Scentre receives from specialty retailers versus Myer, it would be in Scentre’s interest to replace Myer with more profitable tenants. And why not? Its business model for the last 50 years is based on replacing weaker retailers with stronger ones.

Upscaling the shopping centre experience is something Scentre excels at. For example, in 2003 when the refurbished Westfield Bondi Junction opened, it sucked foot traffic away from nearby Oxford Street into its new shopping centre. Retail trade in Oxford Street dropped 30% in the four months after Westfield Bondi Junction opened, while neighbouring suburbs experienced similar declines. Shortly after Oxford Street looked like a ghost town of retail shop vacancies.

But one transaction occurring well before Myer’s 2009 IPO helped ensure the company’s long-term survival. Myer’s flagship Sydney CBD property was sold to Westfield (now Scentre Group) in 2003 and leased back to Myer as an anchor tenant. Like Sears spinning off Seritage, Myer entered into a favourable long-term leasing arrangement with Scentre for 20 years with six 10-year options.

However, Myer’s decline has created a conundrum for Scentre. An anchor tenant enjoying favourable rents with a poor retail proposition is not what a retail landlord wants. If Scentre can reposition Myer’s floorspace, especially in its Westfield Sydney location, the valuation uplift would be significant.

Scentre’s upside

To work out the upside for Scentre, Myer Sydney City sales must be estimated as it is not disclosed by the company. At Myer’s strategy presentation in September 2015, the company disclosed that flagship stores generate about 2.6 times more sales per square metre (psm) than local community stores. Given local community stores generate about $6,000 psm in sales, it would imply Myer’s flagship store generates $15,600 psm in sales. So, this is a good proxy for Myer Sydney City sales productivity.

That may look fine versus community shopping centres, but versus sales productivity in the middle of the Sydney CBD it falls way short. In Scentre Group’s 2017 Property Compendium, specialty retailers in Sydney CBD are about 42% more productive and generate $22,194 sales psm. It also shows Myer is an anchor tenant and rents 46,754 sqm of gross lettable area.

Based on 46,754 sqm and an estimated $15,600 sales psm, the Myer Sydney City store would generate about $729m in retail sales. Replacing Myer with specialty retailers means the same floorspace could generate $1,039m in retail sales. The value creation will be significant for Scentre if it can transition away from an anchor tenant paying 7% occupancy cost (rent as % of revenue, 2016 Myer annual report) to specialty retailers willing to pay 18% occupancy cost (Scentre Group 1H18 results presentation). Hence, the rent from Myer’s Sydney floor space could shift from $51m (7% of $729m) to $187m (18% of $1,039m). The increase in rent of $136 million based on Scentre’s latest Sydney CBD capitalisation rate of 4.12% implies a $3.3 billion valuation uplift. This represents about 16% of Scentre’s current market capitalisation.

But despite Scentre’s track record in remixing its portfolio with stronger tenants, it can only replace Myer once leases expire or when rent cannot be paid. Scentre can’t force Myer to vacate on its own. It needs help. And that help is a multi-pronged pincer move that will likely crush Myer.

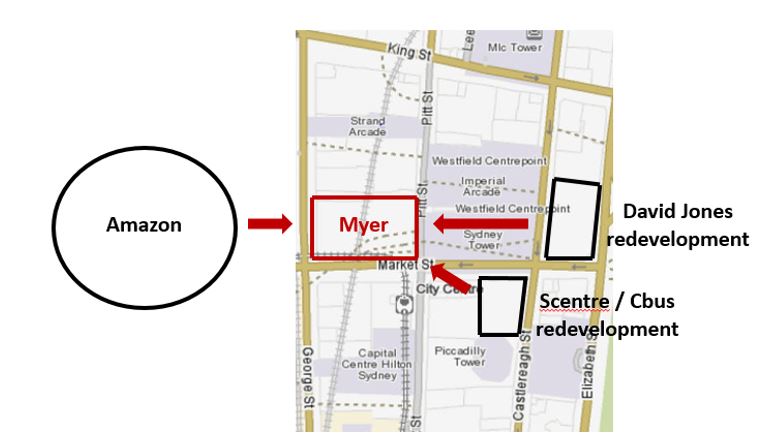

Pincer 1: Amazon

In the US last year, 44% of e-commerce sales were made through Amazon’s marketplace. Amazon grew US online sales by 32% in the last 12 months. And Amazon is a category killer in apparel. In 2017, it overtook Walmart as the largest apparel retailer in the US with an estimated 11% market share. And its market share is expected to almost double in the next three years. Chances are Amazon will replicate its success in Australia at some point. And when it does, consumer sentiment will be akin to when Aldi became an overnight sensation (and supermarket killer) in 2015 despite entering Australia in 2001. These things take time.

Pincer 2: Scentre’s redevelopment of the David Jones Market Street building

A crucial part of the pincer movement has only become apparent recently. In August 2016, David Jones sold its Market Street building to a Scentre / Cbus joint venture for $360m. While David Jones will continue to occupy the site until late 2019 with a 1-year option, Scentre will then take possession and redevelop the 10,000 sqm site and integrate it with Westfield Sydney. This site will potentially draw in over $200m of sales from neighbouring stores, including Myer.

Cbus plans to build a 22-storey luxury apartment tower above the redeveloped 10 storey retail and office building, providing a somewhat captive, steady flow of foot traffic. This is an advantage Myer’s Sydney City store doesn’t have.

Pincer 3: Refurbished David Jones Elizabeth Street building

Compounding the threat to Myer, David Jones has put aside $200 million from its Market Street property sale to renovate its adjacent 30,000 sqm Elizabeth Street store. The redevelopment of David Jones Elizabeth Street has already begun and is expected to be complete by late 2019. When finished, it is expected to be Australia’s premium department store. Unfortunately, for Myer it’s right around the corner.

Diagram 1: Sydney CBD retail district

Myer’s downside

Despite today’s known risks associated with running a department store like Myer, the abovementioned pincer move looms large. Amazon’s growing online threat and a combined 40,000 sqm of luxury retail development in Sydney’s CBD is like an arms race to capture a larger share of the consumer wallet. Retailers like Myer that are not spending as much as their competition will be left behind. Fickle consumers will always gravitate towards the newest or most convenient retail offerings.

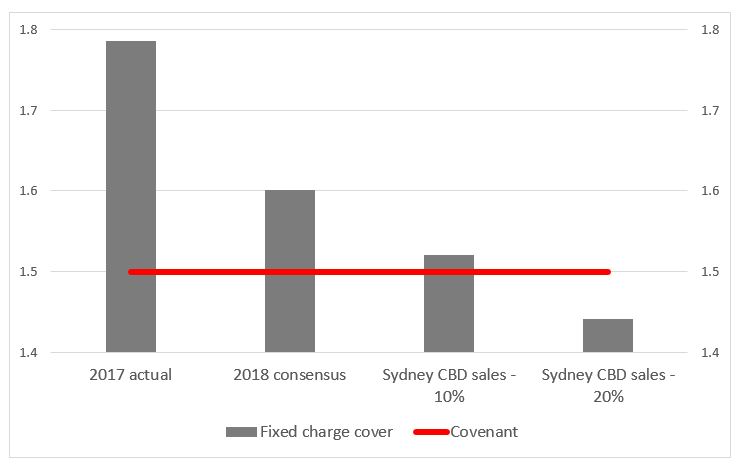

The effect of the multi-pronged pincer move could prove to be dire for Myer. Its Sydney City estimated sales of $730 million represent about 23% of Myer’s total FY17 total revenues. So, if its Sydney City sales collapsed, it would be a major wound for Myer. Any change in Myer’s operating results will be amplified given the company is flying close to its debt covenants. In particular, its fixed charge cover (earnings before rent / interest expense + rent) would be most at risk of a breach.

To be clear, we don’t expect Myer’s Sydney City sales to go to zero. But we expect it to be materially impacted by these new developments. The chart below shows the impact of a 10% ($73m) and 20% ($146m) decrease in sales for Myer Sydney City.

Chart 1: Myer fixed-charge cover

Source: Myer, FactSet, Vertium

A 10% decline in sales at Sydney City would put Myer on the cusp of breaching its fixed-charge covenant, while a 20% decline would almost certainly require Myer to raise fresh equity.

Conclusion

There are glaring parallels between Seritage and Scentre. Both are transforming their tenant base from large retailers (including incumbent department stores) to specialty retailers from which they can command higher rent. Similarly, the plights of Sears and Myer have striking parallels as both embark on a path of survival. But while the threats to Sears are well known, the risks to Myer are growing. Sears is well down the path, whereas Myer is about to face the biggest challenge in its corporate life.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Daniel joined Vertium Asset Management in 2017 as a Portfolio Manager / Equity Analyst and brings with him nearly 15 years’ Australian equity investment management experience. At Vertium, Daniel assists the CIO and is responsible for researching and analysing Australian companies.

Prior to Vertium, Daniel was a Senior Equities Analyst / Portfolio Manager at Forager Funds where he was responsible for assisting with Forager’s Australian equities portfolio.

Before Forager, Daniel held similar roles at Morningstar, Northward Capital, Investors Mutual, Cannae Capital and MMC Asset Management.

12 topics

Daniel Mueller

Vertium Asset Management

Daniel joined Vertium Asset Management in 2017 as a Portfolio Manager / Equity Analyst and brings with him nearly 15 years’ Australian equity investment management experience. At Vertium, Daniel assists the CIO and is responsible for researching...

Expertise

Daniel Mueller

Vertium Asset Management

Daniel joined Vertium Asset Management in 2017 as a Portfolio Manager / Equity Analyst and brings with him nearly 15 years’ Australian equity investment management experience. At Vertium, Daniel assists the CIO and is responsible for researching...

Expertise

Comments

Comments

Sign In or Join Free to comment