TOL - 19th Jul, 2021

One of the most compelling opportunities on the ASX today

Lendlease (ASX: LLC) is one of the most compelling opportunities on the ASX today. While all the attention has been on the company's (now sold) engineering business, the significant progress made in a key area of shareholder value creation over the coming years has been overlooked.

Lendlease is a global leader in property development and investment management. Their expertise and reputation in property development has seen the development pipeline grow from $71 billion to over $110 billion in just three years.

In this article, we explain why we believe Lendlease presents a compelling investment opportunity and why a strategy to accelerate its highly sought-after developments has the potential to unlock value for its shareholders.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

Lendlease 101

Lendlease operates across three business segments:

1. Property Development – Partnering with large capital partners to design and develop high-quality precincts in key gateway cities around the world.

2. Investment Management – Management of these property assets on behalf of large capital partners such as pension funds, insurers, and sovereign wealth funds for a recurring annual fee.

3. Construction – The construction of both external and Lendlease projects

Why is Lendlease undervalued?

Lendlease began reporting cost overruns and issues at its engineering projects in 2017. Several issues within the division such as tunnelling in North Connex, construction delays at Melbourne Metro and the recent provision on completed legacy projects has resulted in losses of almost $1 billion. A poor experience for Lendlease and their shareholders.

In late 2019, Lendlease sold its Engineering business to Spanish firm Acciona. We believe that the Engineering business has been a major reason the firm’s financial underperformance, in addition to the large valuation discount applied to the total business by the market. Exiting engineering has created an opportunity for Lendlease to simplify its business and focus on Property Development and Investment Management.

More recently, due to COVID, Lendlease has had to pause the development of some of its major urbanisation projects. Property sectors like Office have seen a slowdown in tenant demand which has negatively impacted near term earnings. However, the outlook for planning approvals and capital partners has improved. At its recent operational update, Lendlease announced the approval of its residential tower at One Sydney Harbour, secured an investment partner at Innovation District development in Milan and secured an anchor tenant at its third office tower at Melbourne Quarter and sold 100% of the development, with an end value of $1.2 billion.

Beyond some of the challenges today, the acceleration of the development pipeline looks very promising. As the development of major projects accelerates, we see upside to Lendlease’s Property Development and Investment Management segments. We explore both in further detail below.

The potential upside?

1. Accelerating the development pipeline

Lendlease’s reputation and property development expertise has resulted in significant growth in their development pipeline across key gateway cities including Sydney, London and Chicago. Over the last three years, project wins have accelerated, and the development pipeline has grown from $71 billion to more than $110 billion. Importantly, many of these projects have been secured with large capital partners, reducing the capital intensity and sharing the risk involved in major developments. Lendlease’s capital partnership model also allows them to leverage their strong relationships with large investors and institutional partners to accelerate future projects.

The development pipeline features several high profile and highly sought-after developments in key gateway cities such as:

1. The $21.5 billion Google project in San Francisco partnering with Google for the next 10 to 15 years to redevelop the tech firm’s land holdings into mixed-use communities including office, retail, residential and hospitality.

2. Silvertown Quays in East London which includes a mix of office, 3,000 residential units across build-to-sell and build-to-rent and retail space.

3. The Exchange TRX in Kuala Lumpur which comprises of over 2,000 residential units and 122,000sqm of retail property plus a hotel.

Figure 1. Lendlease’s development

projects in San Francisco, East London and Kuala Lumpur

Source: Company Data, Firetrail, June 2021

Lendlease also specialises in build-to-rent projects. These projects involve the development of major residential projects on behalf of long-term capital partners which are then leased out to provide a recurring income (yield) for the investor. Build-to-rent makes up 21% of the current development pipeline and Lendlease are seeing significant growth in the asset class due to undersupply of housing in cities like London, New York and Chicago.

Lendlease’s broad pipeline of highly sought-after developments have secured future earnings for the firm. Beyond the near-term challenges, Lendlease is well placed to grow future earnings by leveraging its capital partnership model and development expertise.

2. Growth in high-quality investment management earnings

As property development projects are completed, a large portion of these assets are managed by Lendlease’s Investment Management business. Upon completion, capital partners like superannuation and pension funds can outsource all management activities to Lendlease for a recurring annual fee (usually a % of the value of assets).

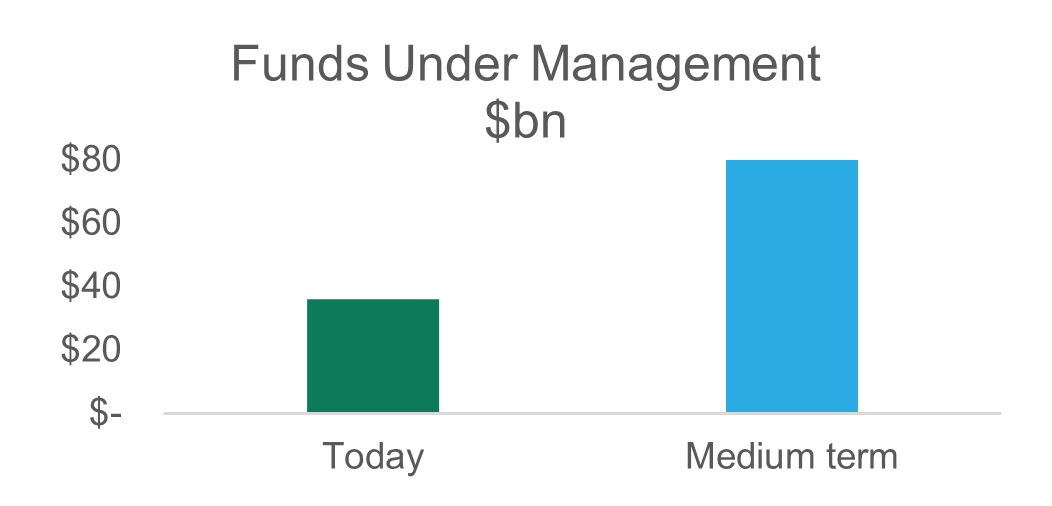

Today, Lendlease has $36 billion in Funds Under Management (FUM) which is expected to grow to over $80 billion in the coming years. In our view, Investment Management could account for around 50% of earnings in the next five years (compared to an average of 31% over the past five years).

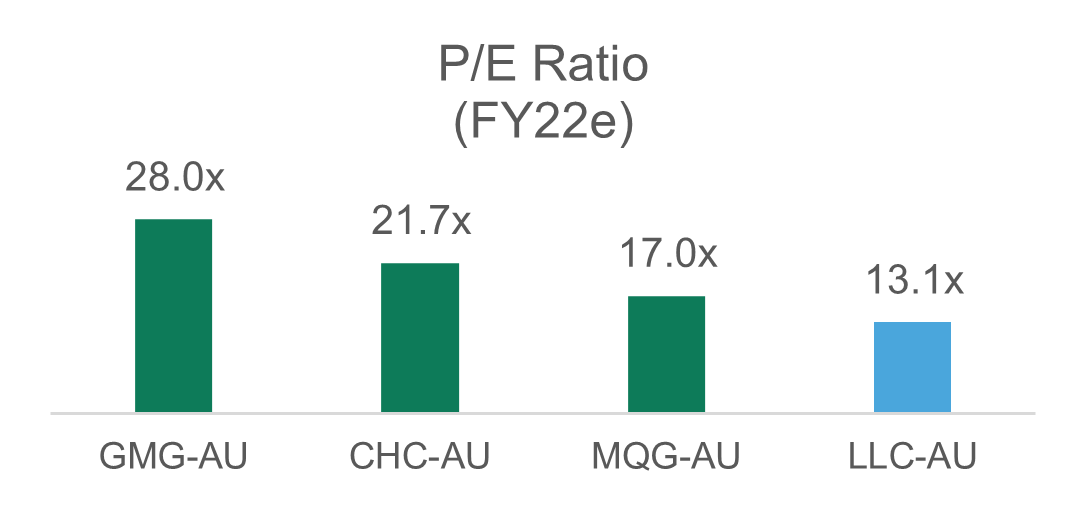

Investment management businesses generally trade at a premium to reflect the stable, recurring nature of their earnings. As seen in Figure 2., Lendlease currently trades at a discounted valuation to peer asset managers such as Macquarie (MQG) or Goodman (GMG). As FUM grows (Figure 3) and Investment Management becomes a larger part of Lendlease’s earnings, we expect the Lendlease valuation to re-rate to reflect the higher quality mix of its Investment Management earnings, and the sale of its problematic Engineering business (which generally trade at a lower valuation multiple).

Fig 2. Funds management businesses demand a premium

valuation to reflect their stable, recurring earnings

Source: Factset, Firetrail,

June 2021

Fig 3. Over the medium term, development completions will drive significant growth in funds under management

Source: Company data,

Firetrail, June 2021

Conclusion

Lendlease is a global

leader in Property Development and Investment Management. With a development

pipeline in excess of $110 billion and growing FUM in its investment management

business, Lendlease is a compelling investment opportunity currently unloved

and undervalued by the market. Lendlease is a holding in the Firetrail

Australian High Conviction Fund and Absolute Return Fund.

Want more market analysis?

We hope you enjoyed this wire on Firetrail's investment thesis behind LLC. If you want to read more market analysis like this, click the follow button below. We hope you enjoyed this wire. If you did, give it a like.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Welcome to Livewire, Australia’s most trusted source of investment insights and analysis.

To continue reading this wire and get unlimited access to Livewire, join for free now and become a more informed and confident investor.

Already have an account? Sign in here

Advertisement

This article is for members only

Join Free to unlock all exclusive content

To continue reading and gain unlimited access to all Livewire content, join free to become a more informed, confident investor.

Already have an account? Sign in

Blake is the Deputy Managing Director at Firetrail as well as Portfolio Manager for the Firetrail Australian High Conviction Fund. Blake’s primary sector responsibilities are Resources, Oil and REITs. Blake has over 21 years’ experience investing in equity markets. Prior to joining Firetrail, Blake spent 12 years at Macquarie Group where he was Co-Lead Portfolio Manager of the Macquarie High Conviction Fund. Blake holds a Bachelor of Mathematics and Finance (First Class Honours) from the University of Wollongong (Australia). Blake is also a Chartered Alternative Investment Analyst (CAIA).

........

This document is prepared by Firetrail Investments Pty Limited (‘Firetrail’) ABN 98 622 377 913 AFSL 516821 as the investment manager of the Firetrail Australian High Conviction Fund ARSN 624 136 045 and Firetrail Absolute Return Fund ARSN 624 135 879 (‘the Funds’). This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Pinnacle Fund Services Limited ABN 29 082 494 362 AFSL 238371 ('PFSL') is the product issuer of the Funds. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) ABN 22 100 325 184. The Product Disclosure Statement (‘PDS’) of the Fund is available at https://firetrail.com/products/firetrail-australian-high-conviction-fund. Any potential investor should consider the PDS before deciding whether to acquire, or continue to hold units in, the Fund.

Whilst Firetrail, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Firetrail, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

The information is not intended for general distribution or publication and must be retained in a confidential manner. Information contained herein consists of confidential proprietary information constituting the sole property of Firetrail and its investment activities; its use is restricted accordingly. All such information should be maintained in a strictly confidential manner.

Any opinions and forecasts reflect the judgment and assumptions of Firetrail and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future.

Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Firetrail. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Firetrail.

MORE INFORMATION

General enquiries 1300 010 311

Existing client enquiries 1300 360 306

www.firetrail.com

3 topics

1 stock mentioned

Blake is the Deputy Managing Director at Firetrail as well as Portfolio Manager for the Firetrail Australian High Conviction Fund. Blake’s primary sector responsibilities are Resources, Oil and REITs. Blake has over 21 years’ experience investing...

Expertise

Blake is the Deputy Managing Director at Firetrail as well as Portfolio Manager for the Firetrail Australian High Conviction Fund. Blake’s primary sector responsibilities are Resources, Oil and REITs. Blake has over 21 years’ experience investing...

Expertise

Comments

Comments

Sign In or Join Free to comment

dani ecuyer

Lend Lease is also removing valuable koala habitat in south west Sydney at the Gilead project.

I agree wholeheartedly Blake. But like Boral, it needs a shake from the outside. Just been an executive enrichment club for many years. Long term performance of this company has been atrocious, despite the many macro tailwinds. IMHO, takeover fodder for Brookfield or Blackstone.

M

Mark M

Yes, Lend Lease are removing valuable koala habitat which has been supported by the NSW Government. #gladysthekoalakiller

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Macro

Tariffs, trade, and tumbling markets: What it means for investors

Jamieson Coote Bonds