Getting perspective on markets

They say that truth is the first casualty, but I would suggest that ‘perspective’ is actually the first to go. Case in point: 2 people in a supermarket having a punch-up over a roll of toilet paper.

Our markets have definitely lost perspective. So at times such as these, it’s useful to be reminded of the poem by Rudyard Kipling that Warren Buffet quoted in his 2017 Berkshire Hathaway letter:

If you can keep your head when all about you are losing theirs ...

If you can wait and not be tired by waiting ...

If you can think – and not make thoughts your aim ...

If you can trust yourself when all men doubt you ...

Yours is the Earth and everything that’s in it.

Let's try and establish some perspective.

Market Moves are Now Quicker

In 25 years advising and managing money, Friday the 13th of March 2020 rates in my top 5 most extraordinary days. From a low of 4,940.1 the market rallied hard over the final hour to close at 5,590.9 – an extraordinary intraday swing of 13.2%.

In the fullness of time, we may look back at Friday the 13th as the inflexion point. But whether that is the case or not, the more certain learning that we can take away, is that we are in a new era where the market consistently moves more rapidly than at any time in history. Whether it be through the totally pervasive spread of technology, better education and understanding of market drivers, algorithmic trading, more rapid dissemination of information or a combination of all of the above, what is clear is that swings that previously took months to unfold, now take days and in some cases hours.

Proof positive, in the fabled GFC the market took 10 months to fall 27% and then a further 6 months to fall a further 27%. The same move just occurred in under 3 weeks!

This should provide some comfort for investors, as faster down = faster up. As was evident on Friday the 13th, when sentiment changes, the pent-up buying can be just as forceful. This provides the opportunity for investors who are both well-funded and well-grounded.

There is a New Safety Net

The 2008/09 GFC was a watershed era for a host of reasons. But front and center was that it established a new playbook for global central bank coordination. In 2008/09, the US Federal Reserve System set out on a journey which would ultimately involve the People’s Bank of China (PBC), the European Central Bank (ECB), the Bank of Japan and even the Bank of England. It would be a journey that would re-define monetary policy (negative interest rates), lead to record FISCAL policy and ultimately end in Quantitative Easing (QE).

In effect, coming out of the GFC, Central Banks agreed that moving forward they would insulate the wider community from the effects of economic mismanagement, cyclical downturns and general panic. How this ultimately ends in the coming decades is the discussion for another day. But the salient point for us right here right now, is that there is a new playbook and Central Banks will do whatever it takes to prevent contagion. We should therefore expect to see ‘shock and awe’ followed by more ‘shock and awe’, until confidence and stability is returned.

Why Has the Market Fallen so Heavily?

It is important to understand why the market has been so heavily sold. Some reasons that make sense to us include:

- The market was in overbought territory and there was a well held belief that a (10-15%) correction was due.

- Containing the Covid-19 virus will have a real and material impact on global economic growth.

- We are in unchartered territory: we have never previously experienced the invocation of containment on this scale. There is no case precedent and as it is often quoted, markets hate uncertainty.

- Forced selling; from equity fund redemptions, passive ETFs and margin calls: from currently available data, ASX margin calls on Monday the 9th of March was the highest on record.

- Panic

Some Perspective on Covid-19

Firstly, let’s be clear: despite the World Health Organization (WHO) labelling this a pandemic, we don’t actually have a pandemic. The US Centre for Disease Control (CDC) estimates that 42.9 milllion people in the US alone were infected by influenza during the 2018-19 season, of which 647,000 were hospitalized and 61,200 died. To date Covid-19 infections globally are less than 1% of this number. What we have is a major, concerted effort to prevent a true pandemic from occurring. This requires that medical outcomes are prioritized over economic outcomes (as they should be).

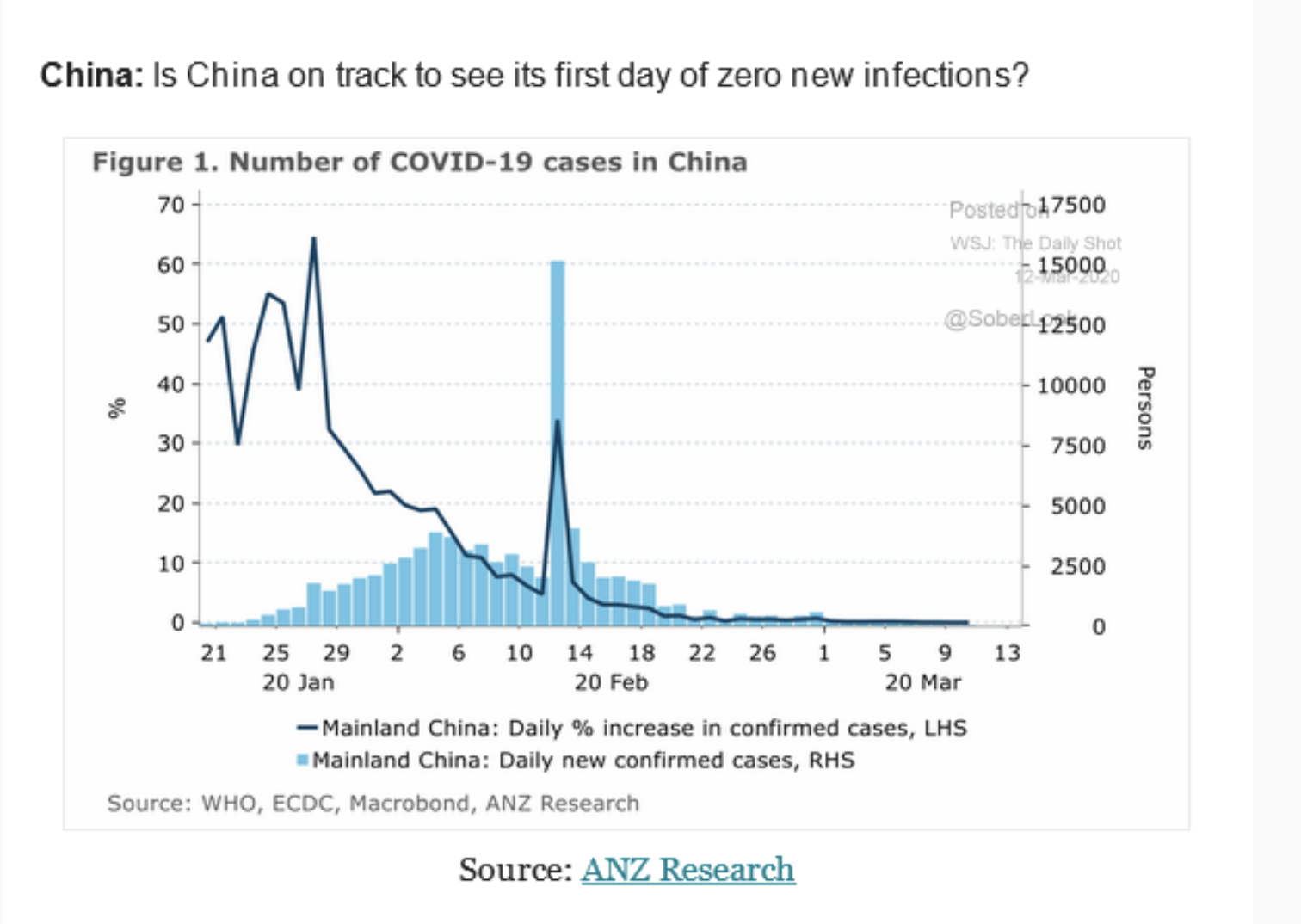

Secondly, the aggressive and far-reaching measures enacted to curtail the spread of Covid-19, are likely to be temporary in nature. As we have seen from countries such as China and South Korea, containment is measured in weeks and months not quarters or years. In China, daily infections peaked at over 5,000 per day. Within a month, this number has fallen to under 100. Whilst this data was initially greeted with a high degree of skepticism, it has now been validated by the experience in South Korea.

Some Perspective on Market Volatility

The old adage ‘volatility is the price you pay for a seat at the table’ has rarely been so true. Equities are the most volatile asset class. But they also provide the best long term returns.

Whilst it is always possible that this market ‘crash’ may morph into something even more dramatic (such as we saw during the GFC), we need to play probabilities not possibilities. We need to understand what is normal. And we need to understand that even if this crash does get worse, in the fullness of time the market will recover.

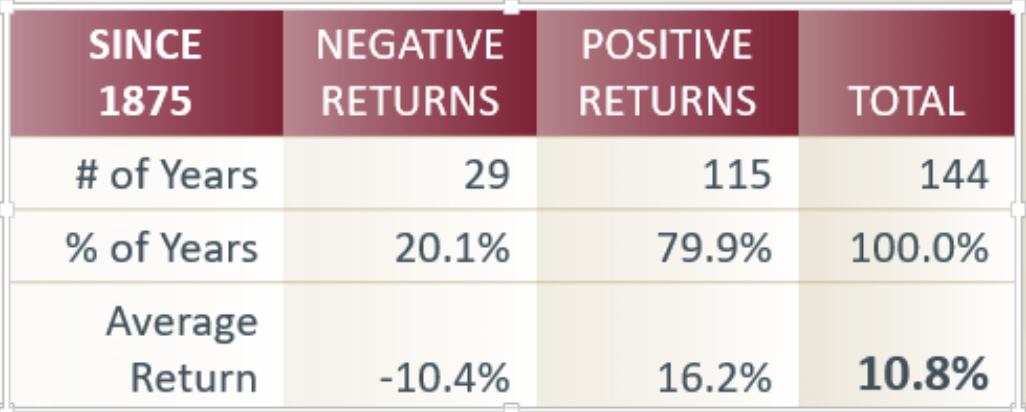

Source: Katana Asset Management

As we can see above, over the past 144 years, the ASX has generated a positive return in 4 out of 5 years, by an overall average of 10.8%.

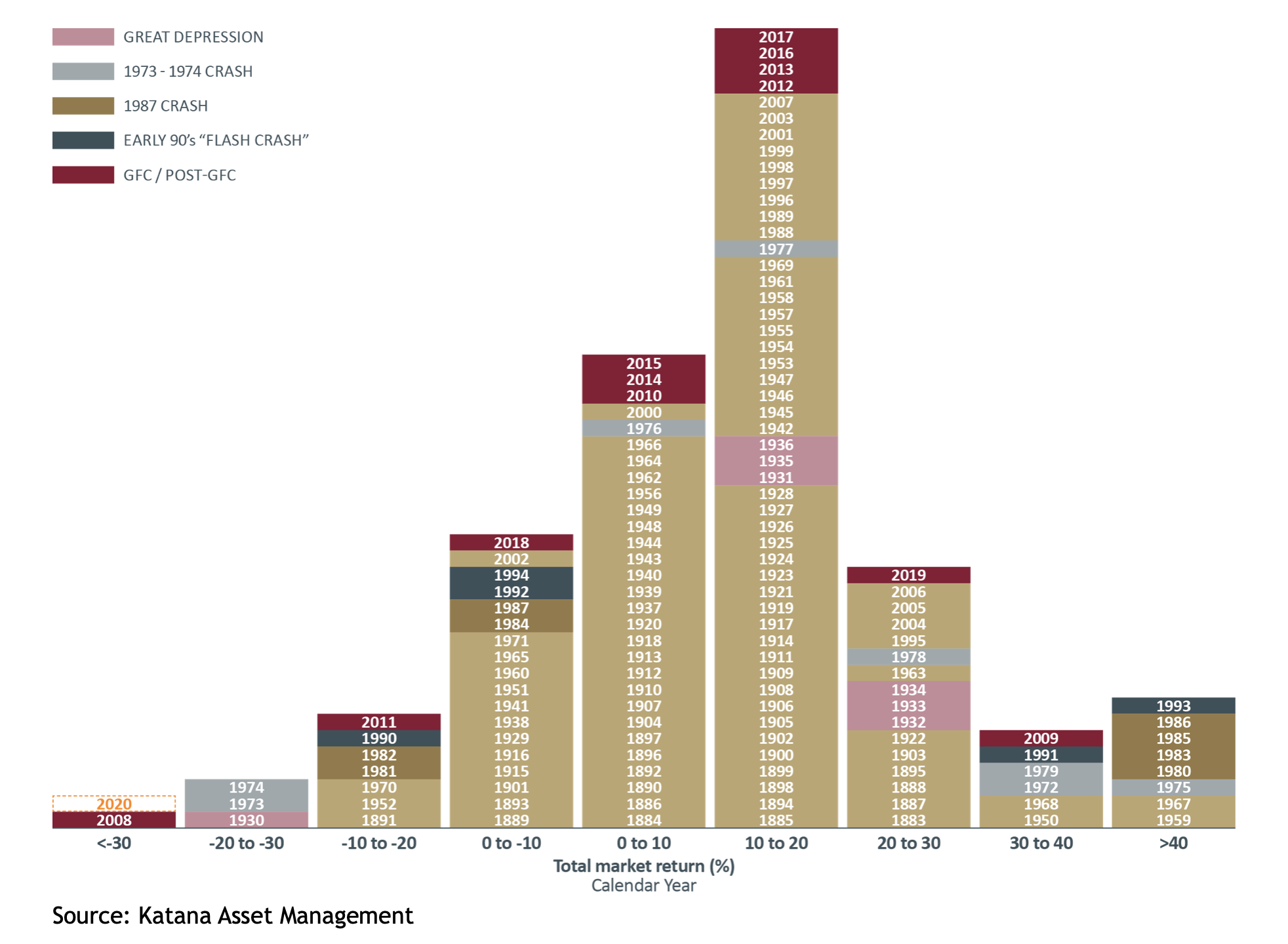

And history sounds out loud and clear, that following periods of volatility and losses, markets inevitably recover.

In the 2008 GFC, many investors panicked and sold at the bottom. And what was the subsequent outcome? In 2009 the market was up by 39.6% and rose in 9 of the 11 years following the crash, including by 18.8% in 2012, 19.7% in 2013 and 24% in 2019Source: Katana Asset Management.

This is not to say that you will not have any further days where your heart is in your mouth! And it is possible that by the time the Covid-19 crisis runs its course, the market may fall further – even by 30% or more (in total). But if it does, it would only be the second time in history that we have experienced a fall in one year of this magnitude. And after the first time this occurred (2008), the market rebounded very solidly for more than a decade.

When is it Time to Capitalize on the Opportunity?

For most investors the time to sell has passed, as has the time to put in place protection given the impact that high volatility has had on premiums.

But along with crisis comes opportunity: the opportunity to recover losses and make some on top. The human, economic and societal impacts of Covid-19 are amply documented, and simply regurgitating some already reported facts doesn’t really help. What we need is a clear pathway towards knowing when it is time to deploy (additional) capital. We are looking for 3 things.

Firstly if we were to see a further dislocation from this level, then that would progressively increase the risk-reward of investing further. Ideally we would like to this in conjunction with points 2 and / or 3 as well, but a sufficient price dislocation from this point is in itself a trigger, particularly in stocks we know well.

Secondly, we are watching for signs of ‘fear fatigue’. A good example of this is the recent US-China Trade War. The lowest point in that market was not encountered when the trade war was actually at its worst – by that time, a large swathe of inventors had already become desensitized to the news flow. The maximum fear was reached much earlier in the piece. We expect the same to occur here. We expect the point of maximum fear to occur well before the maximum effect on the economy materializes. To this end, we are actively monitoring all mainstream media to identify when the headlines dissipate. And of course a clear guide that we are past peak fear will be a reduction in volatility and a stabilization of share prices.

Thirdly and inter-connected, we need to ideally see the US progress along the ‘new infections bell curve’. Whilst China and South Korea are clearly riding out the tail, the US looks to be in its infancy. This means that new infections will accelerate every day and with it the level of panic and hysteria. Where this level peaks at is unknown, but in an ideal world we would not go ‘all in’ until such time as we are well past the hump of new infections.

Of course this is great in theory, but it is very unlikely that prices stay depressed until this point. Markets are forward looking, and hence we will need to form a view on this ahead of the data.

“Don’t Waste a Crisis”

When the dust settles, investors will wake to the reality that the RBA has an official rate of 0.25% (at best) which means that deposit rates will be 1.25% (at best) which means that after inflation and tax, investors will receive a return of negative 1% (at best).

Under this scenario there will be an inevitable migration out of cash back into equities. Reluctant at first, but inevitable in the end.

The time to panic has most likely passed. We need to raise our eyes, look over the horizon and stay focused on long term returns. We also need to remember that the biggest and the best stocks will recover first and this this not the time to be a hero and bet on stocks that have stressed balance sheets or a high cash burn.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

.jpg)

3 topics

.jpg)

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

Expertise

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

Expertise

Comments

Comments

Sign In or Join Free to comment