Pureprofile Limited (PPL.ASX) Cheap turnaround + is chairman spill setting up corporate play?

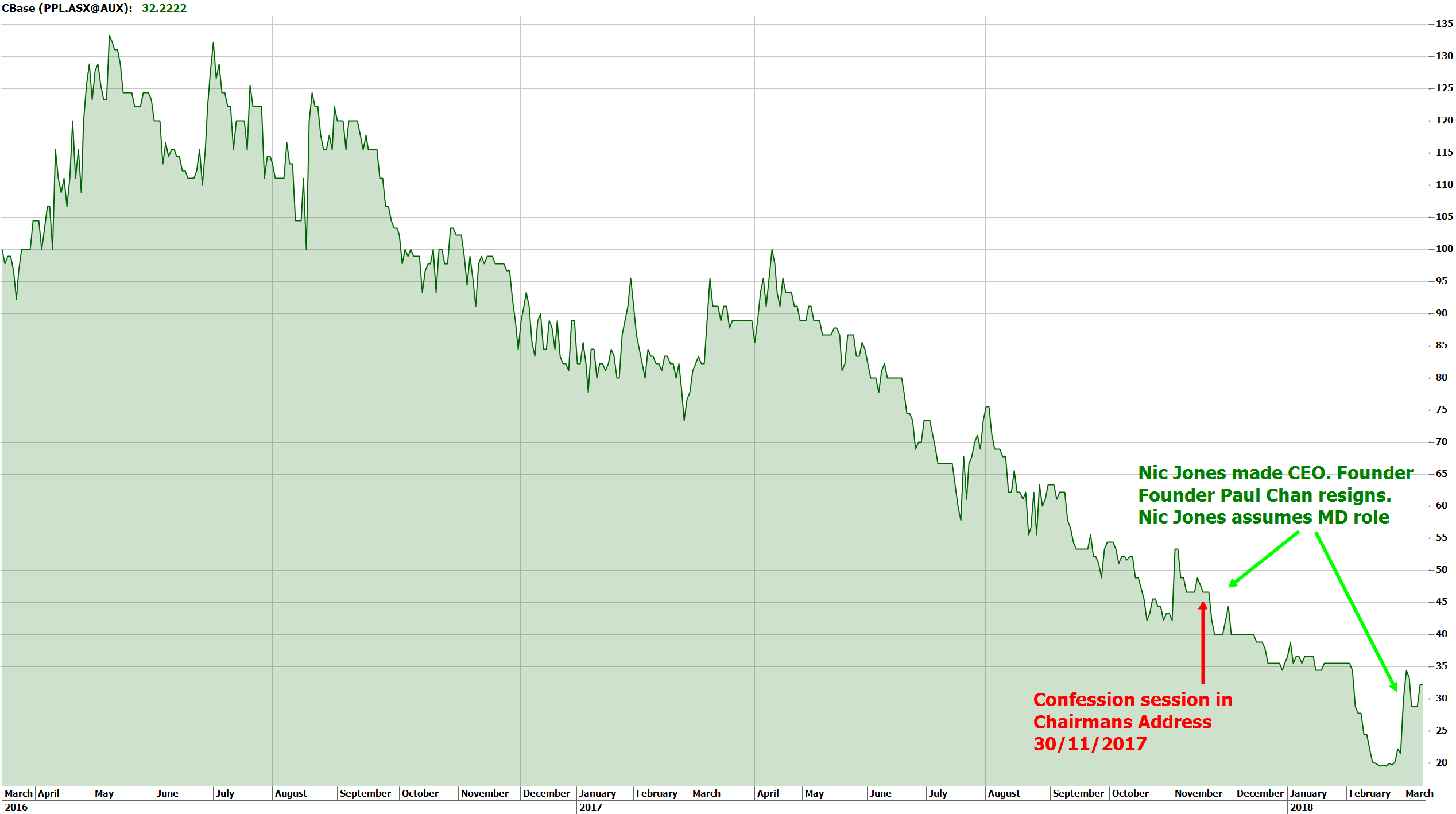

PPL has suffered a 2-year price decline and tore up around ~$40m in value since acquiring the Cohort business. I am more convinced now a turnaround is underway. Why? This is a real business that can benefit following management changes and substantial write-downs. I met with the MD recently, and if successful in delivering on his plan, the company may deliver NPAT between $1m - $4m in the next 2 years. The company could also be a prime corporate play at these levels. There is currently a requisition to remove and replace the Chairman with the former Cohort Founder/CEO, which may be cloaking the interests of other industry participants. Either way, at an $18m mkt cap ($0.15c), both scenarios are worth discussing. (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth management" for Alpine's HNW clients, and are now openly available online through the website. Everything starts with the macro, and then we work back from there in terms of asset allocation and positioning for risk. We work with leading independent research providers and have a structured approach that has worked very well over time. Outside of the core portfolios, we look for opportunities in the small to mid-cap sectors of the market, where our experience can add value.

2 topics

1 stock mentioned

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth...

Expertise

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth...

Expertise

Comments

Comments

Sign In or Join Free to comment