Quantifying the risk of bonds with S&P credit ratings

Elizabeth Moran

Elizabeth Moran Consulting

Each year S&P Global releases a global report that shows defaults as well as rating movements (upgrades and downgrades). Yet again, the report shows that investment grade bonds and other securities are a statistically low risk way to invest.

The most recent Global Corporate Default Study and Rating Transitions report covers the 2017 year and reviews S&P Global’s actions taken worldwide including rating upgrades and downgrades.

Over the 2017 year, there were less rating actions compared to 2016. While there were fewer downgrades, there were more upgrades. The largest single driver of downgrades was the downgrade of China (from AA- to A+), with 31 Greater Chinese entities downgraded by one notch, on average. This is because many companies receive a rating uplift linked to government ownership, hence the rating on companies will generally move in tandem with the sovereign rating.

In 2017, 95 global corporate issuers defaulted – down from the 163 defaults in 2016.The decline in defaults accordingly pushed the speculative grade default rate down from 4.2% at the end of 2016 to 2.4% in 2017. Of these 95 corporates that defaulted, three were Australian companies.

It’s important to note that a default means the company failed to meet its interest or principal obligations by the due date and does not mean the investor lost money – see a definition at the end of the note.

The 2017 year proved to be the best from a credit quality perspective since 2014. Over half of all 2017 defaults were from two sectors: energy and natural resources - 28.4% and consumer services 25.3%.

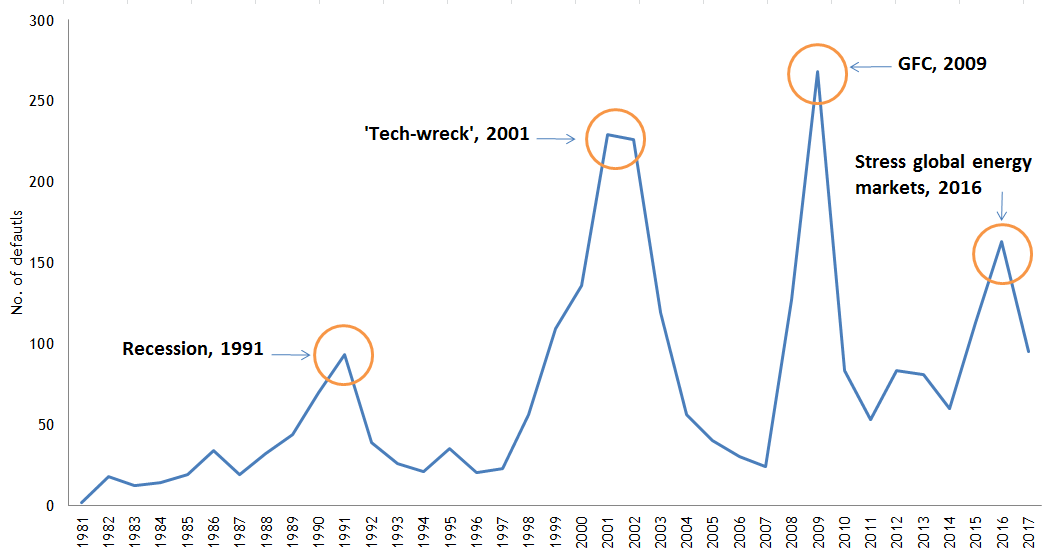

We note that markets continue to recover post the global financial crisis when defaults hit a historical peak of 268 in 2009 (see Figure 1). The study, which goes back over 30 years demonstrates the cyclical nature of markets as shown in the graph where there are distinct peaks in defaults which align with the GFC in 2009, the recession surrounding the ‘tech wreck’ in 2001 and the recession a decade earlier in 1991.

Global corporate defaults chart

Source: S&P Global Fixed Income Research

The graph depicts the global corporate default numbers from 1981 – 2017

Figure 1

This 10 year cycle, which coincides with global or large scale recessions, highlights the need for portfolio diversification. Each of these default peaks corresponded to significant drops in equity prices. While the peak was 268 rated defaults in 2009, global investment grade defaults peaked at 14 in 2008 – from a sample of over 3,000. For investors looking to protect their capital, investing in investment grade bonds is shown to be a statistically safe way to diversify holdings and recession proof investments.

Over a 20 year timespan, cumulative global default rates for an investment grade security was substantially less than 10%, while ‘BB’ rated securities were close to 20%, circa 30% for ‘B’ securities and over 50% for ‘CCC/C’.

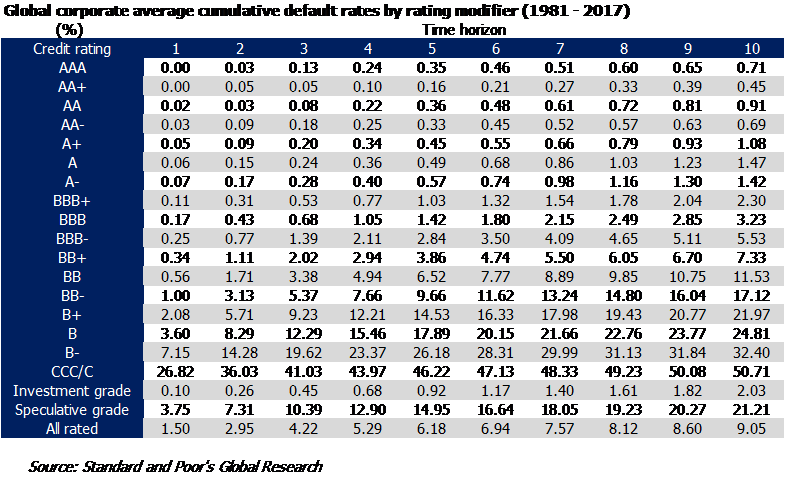

Investment grade stacks up over the life of the study

The statistics over the 36 year study period should give confidence to investors in highly rated bonds. The table shows the probability of default given the term to maturity. For example, an A- rated bond has a probability of default over five years of 0.57%. This increases for the lowest investment grade credit rating ‘BBB-‘ to 2.84%.

If you run your eye down the five year time horizon, you can see the probability of default rises as credit ratings decline. A five year ‘BB’ rated security has a 6.92% probability of default while a ‘B’ rated security a 17.89%. The average of all speculative grades over five years is 14.95%. See Table 1 below.

Source: S&P Global Fixed Income Research

The table shows the probability of default for AAA rated to CCC/C including average default rates of investment grade, speculative grade and all rated. Data from S&P’s 2017 annual global corporate default study and rating transitions report.

Table 1

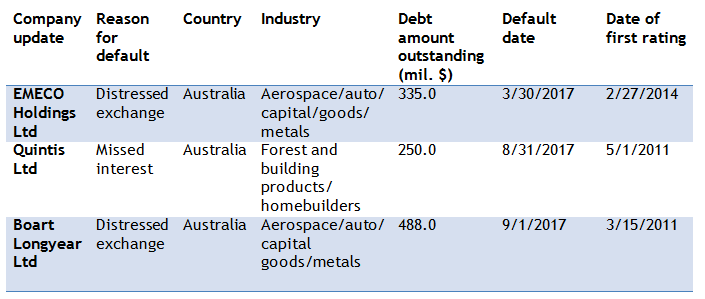

Three Australian defaults

Historically, the Australian default statistics are lower than the global statistics, in part due to our almost exclusively investment grade market, but also due to our concentration towards stronger, larger financial institutions.

In the 2017 year, three Australian rated companies defaulted on USD obligations:

Global publicly rated corporate defaults

Source: FIIG Securities, S&P Global Fixed Income Research

Table 2

A closer look at Emeco – its default ultimately resulted in an improved credit rating

On 31 March 2017, S&P Global Ratings announced that it considered that Emeco Holdings Ltd had selectively defaulted under its debt. This view was based on the company implementing a creditor’s scheme of arrangement that swapped senior secured notes for 34% of ordinary shares for a newly merged group. S&P Global Ratings viewed the transaction as ‘distressed’ as noteholders would receive less that the original securities promised.

A little over a week later S&P raised the corporate credit rating, indicating that it no longer considered that the default was continuing.

What constitutes a default?

For the purpose of the S&P study, a default is recorded on the first occurrence of a payment default on any financial obligation that is rated or unrated – other than when subject to a bona fide commercial dispute. An exception is when an interest payment is missed on the due date, but is made within the contracted grace period. Preferred stock is not considered a financial obligation; a missed preferred stock dividend is not normally equated with default. Distressed exchanges are considered a default; that is when bond holders are coerced into accepting substitute instruments with lower coupons, longer maturities, or any other diminished financial terms.

S&P deem ‘D’ (default); ‘SD’ (selective default); and ‘R’ (under regulatory supervision) as defaults for the purpose of the study.

Remember credit ratings relate to debt securities and not equities. Equities have no repayment date so cannot be rated.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

3 topics

1 stock mentioned

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Comments

Comments

Sign In or Join Free to comment