Recovery delayed, risks rising

Coronavirus is tightening its grip in the US and Eurozone, where it’s expected to cause significant economic disruption. This has repercussions for Asia Pacific (APAC), delaying economic recovery in the region and increasing the risk of a more protracted downturn.

Coronavirus fears infected global markets, prompting the Fed to act

The rapid advance of coronavirus has taken many by surprise. In Europe, cases have continued to rise, particularly in Italy, where the government has imposed a nationwide lock-down to contain its spread.

The extent and effect of the outbreak in the US is still uncertain. Reported cases have risen quickly but remain much lower than numbers reported in the Eurozone. However, the rout in world financial markets made it hard for the US Federal Reserve (Fed) to wait. The apparent increase in risk was severe enough to motivate an emergency 0.5% interest rate cut. Chair Jerome Powell noted that “the committee judged that the risks to the US outlook have changed materially”. He also appeared to leave the door open for future cuts.

Indeed, we expect the Fed to cut rates by a further 0.5%, either in one fell swoop in March, or split into two 0.25% cuts in March and April. Further cuts all the way to the lower bound (0-0.25%) could happen if the shock from the virus proves even more disruptive.

The outlook for the global economy has darkened, delaying the APAC recovery

We had initially expected a modest recovery in APAC growth in the second quarter of 2020, driven primarily by a recovery in China. But the additional headwinds from the US and Eurozone (which may go into recession) and a more prolonged drag from the virus within APAC are likely to delay the recovery and add considerable downside risks.

The global economy is now projected to see a severe slump in the first half of this year – with recessions in some major economies – and may not rebound strongly until the fourth quarter.

The initial shock to the Chinese economy may be bigger than we first thought…

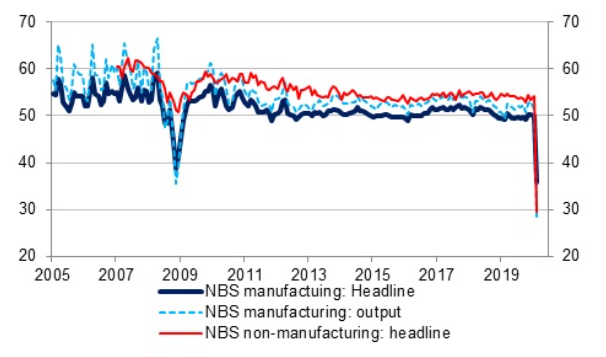

There is little data to judge how coronavirus has affected China’s economy. The Purchasing Managers’ Index (PMI) and trade data are the best indicators we have, and they do not paint a pretty picture. PMIs fell to record lows – much lower than during the global financial crisis even (see Chart 1).

Chart 1: China PMIs fell to record lows

Exports fared little better. Our estimate of seasonally adjusted export values fell by 25% between December and February (with the bulk of the fall occurring between Jan and Feb). This is the largest fall in exports outside of the global financial crisis.

Overall, this points to a somewhat larger contraction in China’s first-quarter growth than we had been pencilling in. Nowcasts based on the PMIs suggest that growth could be -1% quarter-on-quarter, compared with our initial forecast of -0.5%.

The qualitative nature of PMIs means they’re less reliable during such a large shock. PMIs are unlikely to capture increased government spending on healthcare, for example. But daily indicators spanning into March suggest China may be struggling to get back to business, even before any additional headwinds from the West.

…while the shock is yet to fully surface in other countries’ economic data

In the rest of APAC, the manufacturing shock emanating from China does not appear to have fully surfaced yet. PMIs indicate that output has fallen, but nowhere near the decline seen in China. However, there are signs of a bigger effect on supply chains. As the manufacturing shock filters through, we believe the picture across APAC will worsen in the coming months.

Some countries were already vulnerable. In Japan, for example, growth for the fourth quarter of 2019 was revised down, deepening its ‘growth pothole’ even before any disruption from coronavirus. Reflecting this, we now expect full-year growth of -1.0% year-on-year in 2020. But an insufficient policy response from the Bank of Japan and Ministry of Finance presents a large downside risk to this forecast.

The delayed recovery should spur further monetary support across APAC

A larger and more persistent shock would call for more forceful monetary support. Central banks in Asia may be keen to cut interest rates to narrow the surging rate differential with the US – at least to limit the potential for currency appreciation. The sudden fall in oil prices should also remove near-term inflationary pressures and help spur action.

Typically, monetary policy is not well-suited to deal with temporary supply shocks. But its benefits increase the longer the disruption persists. Headwinds from the US and Eurozone point to a far more protracted global shock, for which monetary policy would now be an appropriate weapon.

Most central banks across Asia have room to cut rates and we now believe they are ready to provide more notable support. However, we expect they will proceed cautiously until there is clear evidence of a US and Eurozone slowdown.

Never miss an insight

Keep up to date with Aberdeen Standards latest thinking by hitting the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

abrdn manages assets for a range of global and domestic clients. We invest worldwide and follow a predominantly long-only approach, based on fundamentally sound investments.

4 topics

abrdn

abrdn manages assets for a range of global and domestic clients. We invest worldwide and follow a predominantly long-only approach, based on fundamentally sound investments.

abrdn

abrdn manages assets for a range of global and domestic clients. We invest worldwide and follow a predominantly long-only approach, based on fundamentally sound investments.

Comments

Comments

Sign In or Join Free to comment