RMBS risks rising fast as house prices fall

In assessing whether to get long or short residential mortgage-backed securities (RMBS), we undertake a great deal of quantitative analysis, including revaluing the homes that protect these bonds at regular intervals and developing globally unique RMBS default and prepayment indices. (Regular readers will know that we exited most of our RMBS in February 2018.)

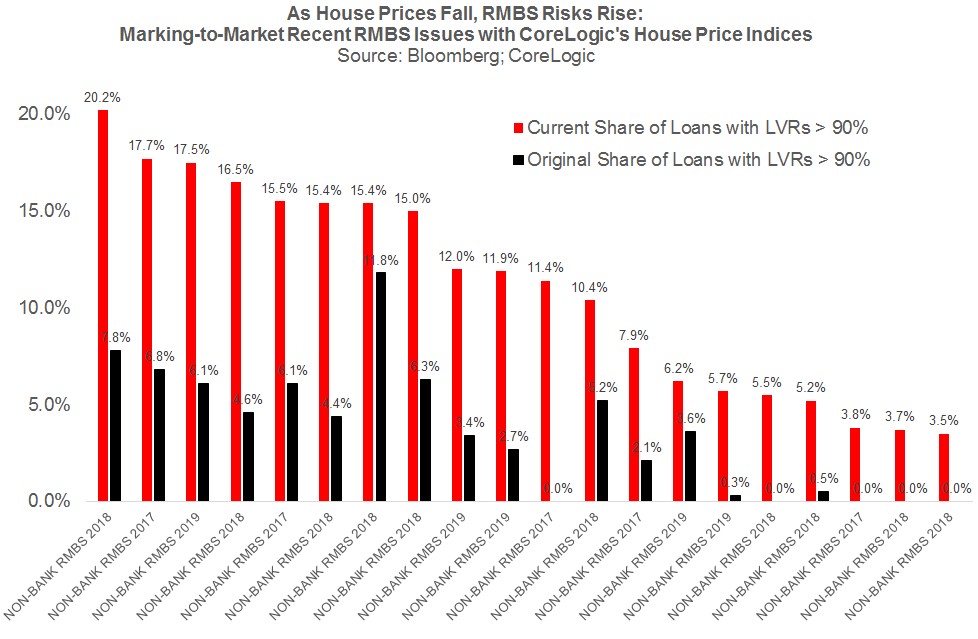

As house prices fall, the loan-to-value ratios underpinning an RMBS issue rise in lock-step, which reduces the equity protecting the bond. Using Bloomberg data on the current amortised value of the home loans in all Australian RMBS pools, the LVR distribution of the loans, and the geographic location of the properties, we have marked-to-market all the 2017, 2018 and 2019 issues after accounting for the amortisation or pay-down of loans through to the end of February 2019.

What we find is some huge increases in the share of an RMBS issue's assets with LVRs over 90% compared to the leverage reported when the bond was originally sold to investors (often jumping from 5% of loans to 15% to 20% of loans).

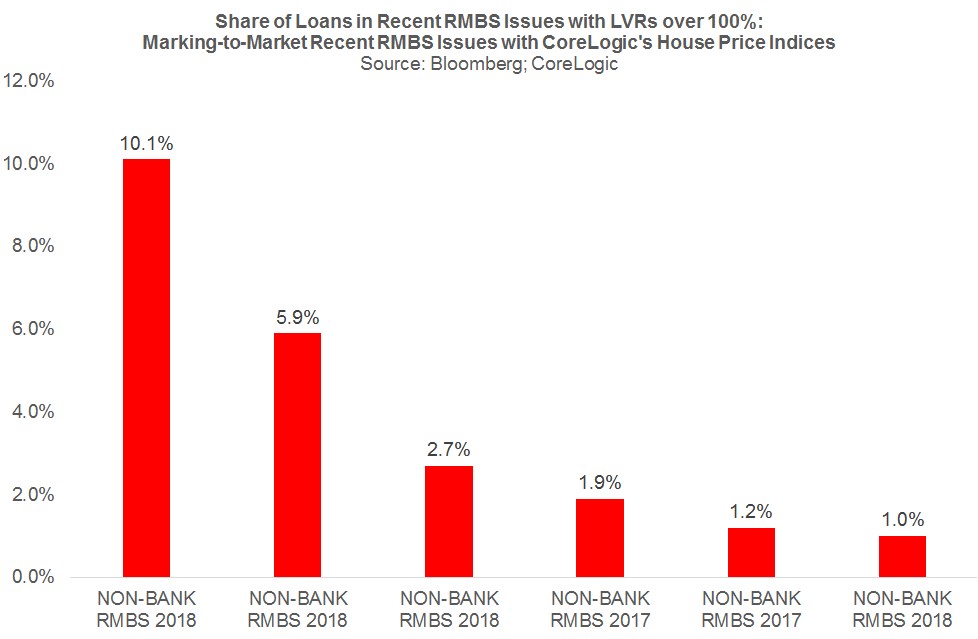

We have also documented some recent RMBS deals where the share of loans that are underwater, or have LVRs over 100%, has increased strikingly, including one transaction where more than 1-in-10 loans appear to be underwater.

All of this analysis would look worse if we marked everything to market at the end March, as house prices have continued to fall.

It is possible that there is a difference between the CoreLogic index price changes and the individual property changes, but we have used the state-wide indices and deals with metro biases (as is common) would likely have even poorer performance than these numbers imply. Also, the automated property valuation models used to revalue individual homes are commonly based on the CoreLogic indices.

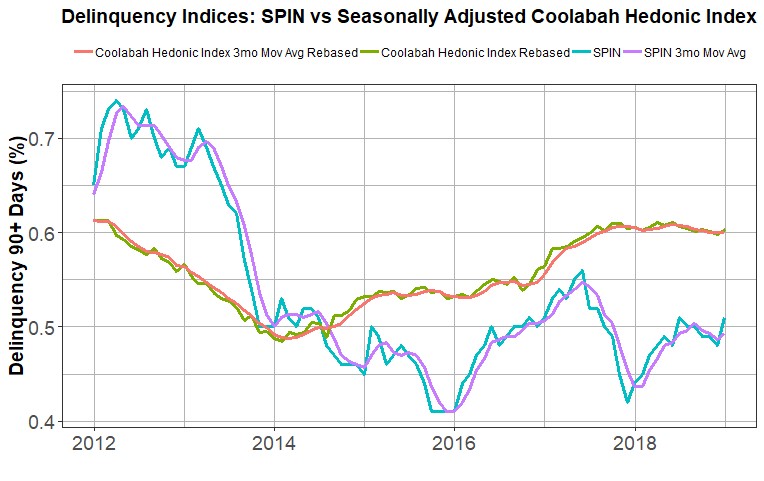

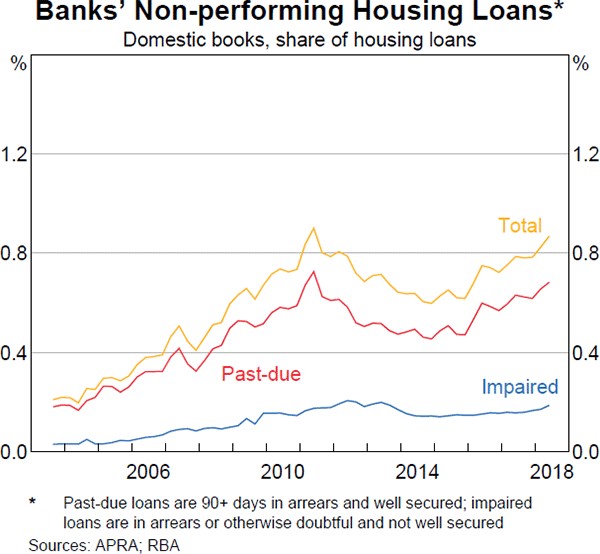

At the same time as the equity protecting RMBS is shrinking, we have demonstrated that RMBS default rates are trending higher back to GFC peaks using our compositionally-adjusted hedonic index of RMBS arrears. This is consistent with the RBA's data on mortgage arrears, which I have enclosed below our index chart.

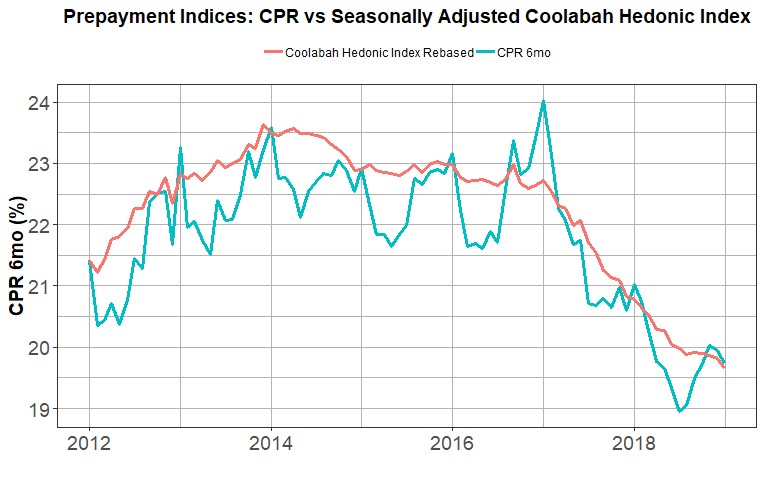

There is also the problem of declining mortgage prepayment rates, which is blowing out the expected life of RMBS bonds (adversely impacting assumed credit spreads) as borrowers struggle to prepay loans at the same rate as they have done in the past.

And finally, we have had an incredible surge in RMBS supply, with the highest level of issuance since the heady days before the GFC (about $100bn of supply since the start of 2017), which will inevitably put pressure on these bonds’ prices.

After we banged the table about these risks early last year, S&P belatedly warned in November:

- “Falling property prices pose a greater risk for the lower-rated tranches of less-seasoned transactions, particularly for loans underwritten at the peak of the property cycle;”

- “The RMBS sector is now facing more elevated risk than it was 12 months ago. Alongside high household debt and low wage growth are emerging risks such as lower seasoning levels in new transactions and increasing competition.”

- “Lower-rated tranches of more recent transactions with lower seasoning levels are more exposed to this risk, particularly for loans underwritten in the past 12 months, at the peak of the property cycle”

- “Less-seasoned loans and highly leveraged loans are most exposed to a more protracted decline in property prices.”

- “Loans originated in more recent years, at the peak of the property boom, will be more exposed to property price declines, particularly those with higher loan-to-value (LTV) ratios.”

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

3 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment