Scruffy Accounting at Greencross

Well that was an interesting update from pet and vet company Greencross (GXL). New CEO Simon Hickey only joined the company in February. So clearing the decks is not surprising. But this one is a doozy.

Alongside the usual writeoffs of inventories, previously capitalised expenses and the expensing of labour costs that were going to be capitalised, there was this little paragraph to get your head around:

"In the first half of FY2018, the Company made an onerous lease adjustment to write back a provision previously made in relation to the retail leases for certain Western Australian stores acquired as part of the City Farmers acquisition. The effective impact of that writeback has been to add rental expenses in the second half which were previously unbudgeted."

You might need to read that a few times. I did. But the new management team seems to be suggesting that the old management team included a writeback of a previous provision in rental expense for the first half of the year.

Indeed note 6 to the half year report spells it out quite clearly:

The $3.5m provision writeback allowed them to report a lower rental expense in the half year, despite a larger store network and one less week compared with the previous corresponding period.

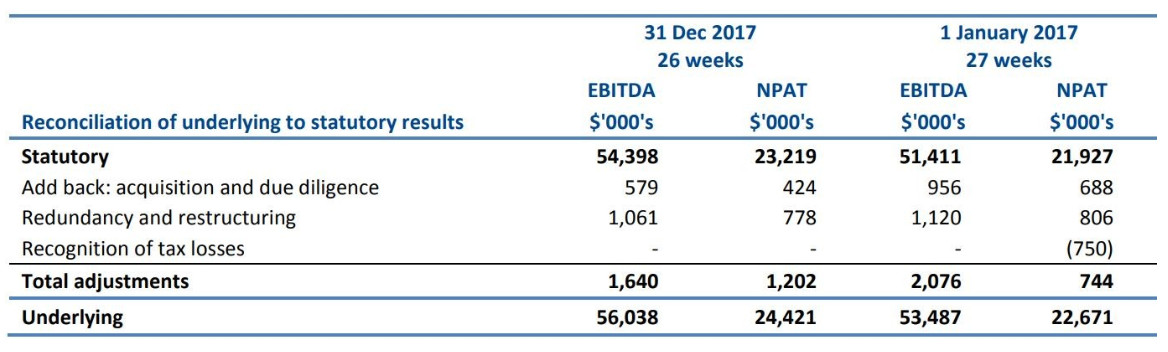

The provision reversal might be justified. It certainly isn’t underlying. And this company is a big fan of adjusted earnings and “underlying EBITDA”. So I went looking for the reconciliation:

Funny that. No mention of onerous lease provision releases. In fact, the word onerous is only found once in the half-year report and isn’t mentioned in the accompanying presentation. Including the one-off reduction in rental expense, EBITDA grew 5%. Factoring in the real ongoing number would have meant a reduction.

Best to leave that explanation for the new guy.

If you are interested in receiving the please register here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Steve began Forager Funds in 2009, and now manages approximately $400m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and redemptions. Steve focuses on long-term investing in undervalued and sometimes unloved companies.

.jpg)

.jpg)

Steve began Forager Funds in 2009, and now manages approximately $400m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and...

Expertise

Steve began Forager Funds in 2009, and now manages approximately $400m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management