TOL - 19th Feb, 2025

Should you buy the dip on ASX healthcare stocks CSL, Cochlear and Pro Medicus?

These three premier ASX healthcare stocks just reported half-yearly earnings – and each saw its share price dip…So, is now the time to buy?

In this article, we’ll investigate the best and worst bits of the recent first-half financial year 2025 results (“H1 FY25”) releases of three of the ASX’s premier healthcare companies, CSL Limited (ASX: CSL), Cochlear (ASX: COH), and Pro Medicus (ASX: PME).

We’ll also check out the market’s response to the results, including the dip in each of their share prices, as well as all the changes in major brokers’ ratings and target prices. Do the experts think you should buy the dip on these blue-chip ASX healthcare stocks? Let’s dive in!

CSL – Still the one to buy according to the brokers

Company Description

CSL is a true Australian success story, having grown from humble beginnings as Commonwealth Serum Laboratories founded in 1916, to a globally significant healthcare company. It operates across the world with divisions including CSL Behring (rare and serious diseases), CSL Seqirus (influenza prevention), and CSL Vifor (iron deficiency management).

5-year chart history

There’s a very good chance that you already have CSL in your portfolio, or if you don’t, it’s on your shopping list. The stock has, for most of this decade, traded above $300 per share. It has on occasion, however, dipped into the $200’s – only to eventually recover back to the top of its trading range around $340.

%205-year%20price%20chart.png)

This means the recent dip is either potentially good news (if you don’t own CSL shares), or bad news (if you do). Hey – if you do – you may be looking to add some more!

H1 FY25 & broker views

The H1 result generally missed the all-important “consensus estimates” on key earnings before interest and tax (“EBIT”) and net profit after tax (“NPAT”) lines due to higher general and administrative costs, and lower than expected revenues from the company's Seqirus unit.

CSL has declared a fully franked interim dividend of $2.07 per share, unfranked, and ex-dividend on 10 March (remember, you must be a shareholder prior to the ex-dividend date to be entitled to the dividend). CSL’s last 12 months dividend yield is approximately 1.7% based upon Friday’s closing price of $256.90.

This is what the major brokers had to say about the result:

Bell Potter: “While the declining US flu market has caused headwinds for Seqirus, Behring continues its strong growth outlook and positive margin recovery, which we expect will continue to drive double digit earnings growth for the group over the mid-term.”

Citi: “We think CSL offers good value at 23x FY26e PE (29x 10-yr avg)” (note PE stands for price to earnings ratio, FY26e stands for FY26 estimate)

Goldman Sachs: “Our Buy recommendation for CSL is driven by (1) Strong growth in the IG market…(2) CSL market share gains in the IG market, Hemophilia, Hereditary Angioedema (HAE) and influenza vaccines, and (3) Gross Margin accretion driven by operational improvements to its cost base.”

Macquarie: “We continue to see medium-to longer-term EPS growth as attractive, with current valuation undemanding.”

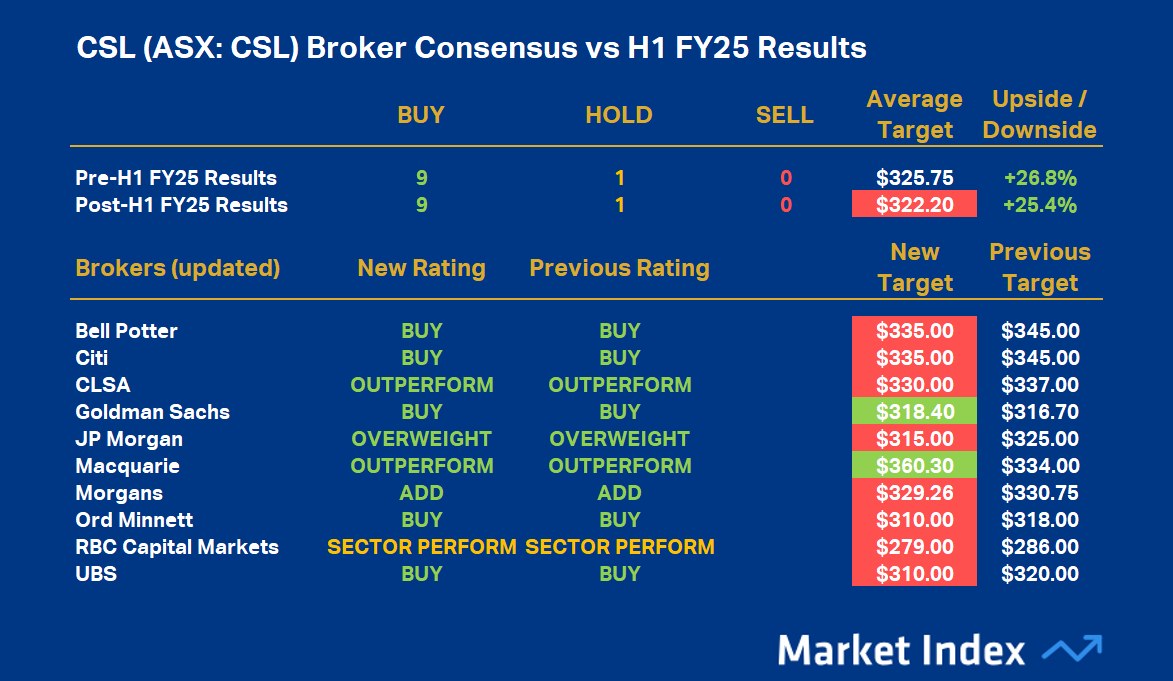

CSL broker consensus changes

To obtain a stock’s Broker Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5.

The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target prices as a 12-month forecast. Each target price is based on fundamental valuation assumptions.

%20Broker%20Consensus%20vs%20H1%20FY25%20Results.png)

CSL’s broker consensus rating is +0.90, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $322.20 (down 1.4% from $325.75 prior to its H1 FY25 results). This suggests brokers collectively believe the stock is around 25.4% undervalued based upon the closing price on Friday, 14 February of $256.90.

Cochlear – Hearing of a potential buy the dip opportunity?

Company Description

Cochlear is an Australian-based medical device company and a global leader in implantable hearing solutions designed for individuals with severe to profound hearing loss who do not benefit from conventional hearing aids. The company offers three main types of implants: cochlear implants, bone conduction implants, and acoustic implants, and is considered to be the industry leader in each area.

5-year chart history

There’s a very good chance that you already have one or both of CSL and COH in your portfolio, they have been for many years stalwarts of Aussie investor’s portfolios. Whilst CSL has traded in a fairly well-defined trading range, COH broke out of its long term trading range last year. The recent dip sees it trading back towards the top of the old trading range around $250.

%205-year%20price%20chart.png)

There is a widely used technical analysis technique that proposes the top of an old trading range tends to act as the bottom of a new / future trading range. If this is the case, then COH shares appear to be approaching a potential zone of historical support around $250.

H1 FY25 & broker views

The major bone of contention within COH’s H1 FY25 results was the lowering of full year guidance for NPAT towards the lower end of the previously guided $410-$430 million range. Management blamed lower than expected growth in the company’s Services segment. On the positive side, COH’s implant unit continued to perform strongly.

COH has declared a fully franked interim dividend of $2.15 per share, franked at 80%, and ex-dividend on 20 March. COH’s last 12 months grossed up dividend yield is approximately 2.1% based upon Friday’s closing price of $262.73 (grossed up dividend yield represents the potential after tax dividend to an Australian resident tax payer).

This is what the major brokers had to say about the result:

Citi: “A lower valuation and/or more clarity on the new products could see us consider a more positive view on the stock.”

Macquarie: “We see COH's current share price as fair based on our analysis and forecasts for CI unit sales growth and operating leverage.”

UBS: “Cochlear still faces the prospect of a vaccine against CMV, a major cause of neonatal deafness, developed by Moderna…We see a balance of residual risk from a data readout for a CMV vaccine against more sustainable CI implant growth and upgrade to Neutral.”

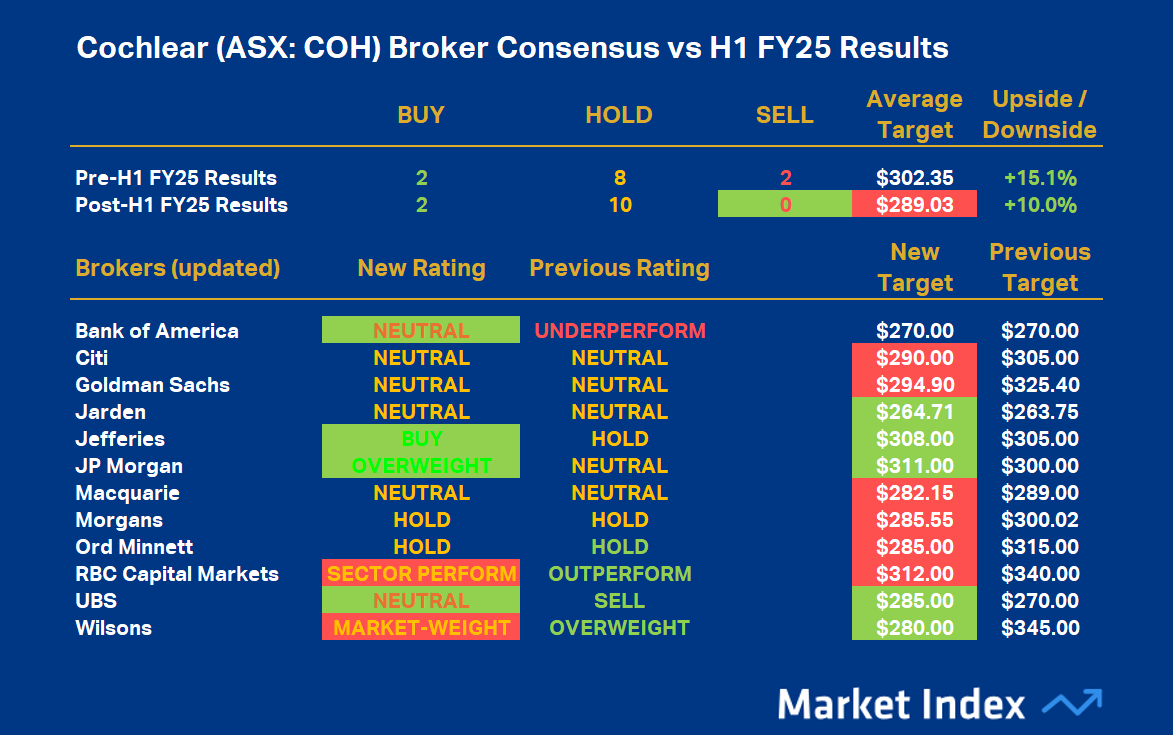

COH broker consensus changes

%20Broker%20Consensus%20vs%20H1%20FY25%20Results_UPDATED.png)

COH’s broker consensus rating is +0.17 (up from 0.0 prior to its H1 FY25 results), resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $289.03 (down 5.1% from $302.35 prior to its H1 FY25 results). This suggests brokers collectively believe the stock is around 10.0% undervalued based upon the closing price on Friday, 14 February of $262.73.

Pro Medicus – "Unprecedented" performance

Company Description

Pro Medicus is an Australian-based healthcare informatics company specialising in medical imaging software and services. The company offers a suite of products, including the Visage 7 Enterprise Imaging Platform, which provides fast and scalable imaging solutions for hospitals and healthcare groups worldwide. Pro Medicus has a significant presence in North America, Europe, and Australia, with the U.S. market accounting for nearly 90% of its revenue.

5-year chart history

PME is the relatively new kid on the block among ASX healthcare blue-chips. Its explosive earnings growth over the last five years has driven similarly explosive growth in its share price, as can be seen in the chart below.

%205-year%20price%20chart.png)

No doubt there are a few of you who consider PME as the one that got away (cue face palm and thought to self: “I knew I should have bought it at $30, $50, $80, $100…🤦”).

Dips have been few and far between on PME over the last 5-years, but when they appeared, they didn’t hang around long. There appears to be a very strong price uptrend in place, and there’s nothing to suggest that this current dip – albeit very small – won’t be yet another buying opportunity for this veritable ASX healthcare rocket! 🚀

H1 FY25 & broker views

The H1 result was generally considered a very small (approximately 2-3%) miss on revenue earnings before interest, tax, depreciation and amortisation (“EBITDA”) Overall, the company’s strong performance during the half with respect to major contract wins was lauded by the major brokers, with Goldman Sachs describing it as an "unprecedented" performance.

PME has declared a fully franked interim dividend of $0.25 per share, franked at 100%, and ex-dividend on 27 February. PME’s last 12 months grossed up dividend yield is approximately 0.24% based upon Friday’s closing price of $283.53.

This is what the major brokers had to say about the result:

Bell Potter: “The PME full stack solution continues to wipe the floor with competitors…we expect further growth in the cardiology space with the first small scale implementation to take place in April 2025. Following earnings revisions we upgrade to Buy”

Citi: “the current valuation implies even higher growth, which over time will become more difficult to achieve due to market share/size”

Goldman Sachs: “ PME is expanding into adjacent solutions including AI and Cardiology which could provide significant upside given we believe PME is the incumbent technology leader in radiology, and is well-placed to take share in both markets”

Macquarie: “While we see potential for increased penetration of the US addressable market, this is largely captured within our forecasts/the current share price. Delivery of new products (AI, other ologies) would present upside to our forecasts.”

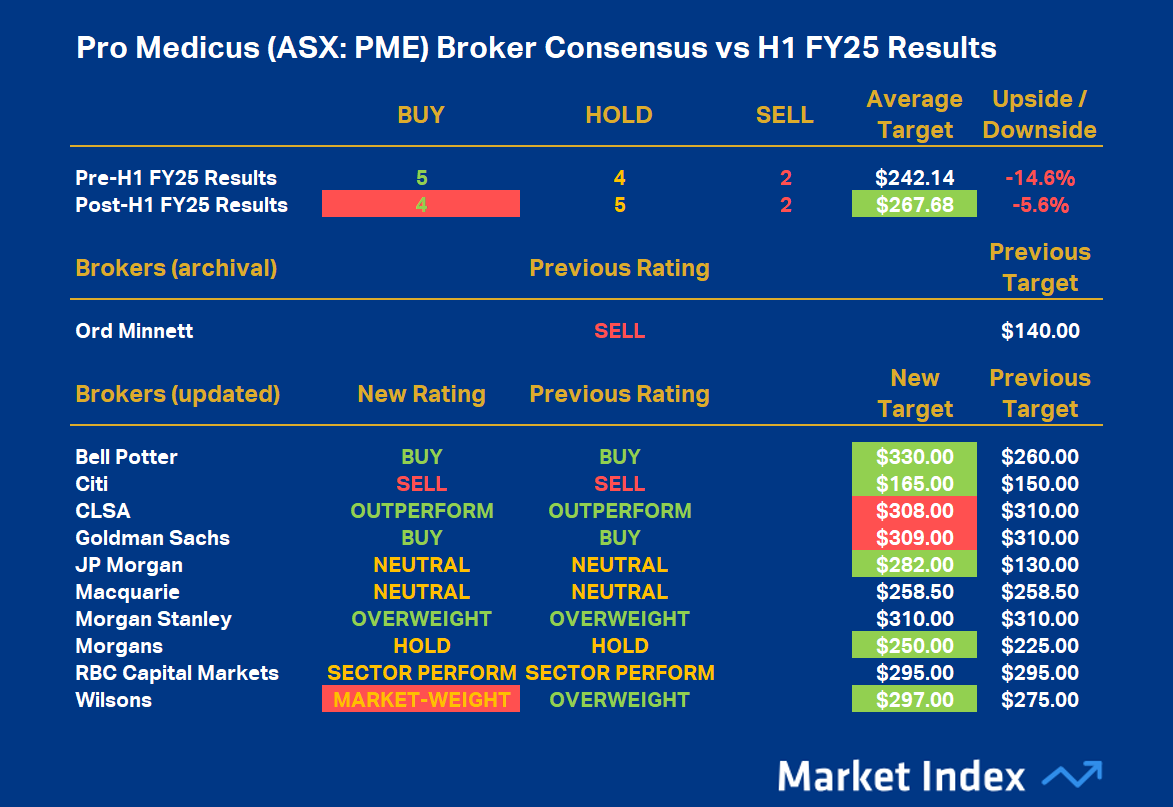

PME broker consensus changes

%20Broker%20Consensus%20vs%20H1%20FY25%20Results.png)

PME’s broker consensus rating is +0.18 (down from +0.27 prior to its H1 FY25 results), resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $267.68 (up 10.6% from $242.14 prior to its H1 FY25 results). This suggests brokers collectively believe the stock is around 5.6% overvalued based upon the closing price on Friday, 14 February of $283.53.

This article first appeared on Market Index on Monday 17 February 2025.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

%20Broker%20Consensus%20vs%20H1%20FY25%20Results.png){kind=link}

%20Broker%20Consensus%20vs%20H1%20FY25%20Results_UPDATED.png){kind=link}

%20Broker%20Consensus%20vs%20H1%20FY25%20Results.png){kind=link}

5 topics

3 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment