TOL - 11th Apr, 2025

Sometimes the best offence is a good defence

Private credit now rightfully stands a long-term strategic allocation within a balanced portfolio of investments

For many Australian advisers, building a balanced portfolio for their clients has rested on a central principal. To manage volatility, a portfolio should be diversified, combining a mix of defensive and growth assets. The rationale is derived from Nobel prize winning economist Harry Markowitz, who pioneered the theory of diversification in his paper “Portfolio Selection”, which was first published in 1952.

“A good portfolio is more than a long list of good stocks and bonds. It is a balanced whole, providing the investor with protections and opportunities with respect to a wide range of contingencies”. Harry Markowitz.

It is interesting to consider what Markowitz would make of financial markets today. Given the continued evolution of capital markets, there is now a huge breadth of asset classes and instruments for advisers to use for their clients, that go far beyond the traditional “60/40” portfolio (where 60% of a portfolio is broadly invested in equities, 40% in fixed income). Unfortunately, the traditional negative correlation between equities and bonds broke down from 2020, with both asset classes tending to move in a slightly positive, rather than negative manner.

Chart 1: Australia Bond/Equity correlation over discreet time periods. Source: Bloomberg, Pinnacle, April 2025.

Perhaps, like many Australian investors, Markowitz would have looked at private credit to complement the traditional fixed income exposure in his portfolio. The ability to capture attractive risk-adjusted returns, and the uncorrelated nature of private credit to both government and corporate bonds, means that private credit has been a favoured destination for superannuation funds[1] and retail investors for much of the last decade.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

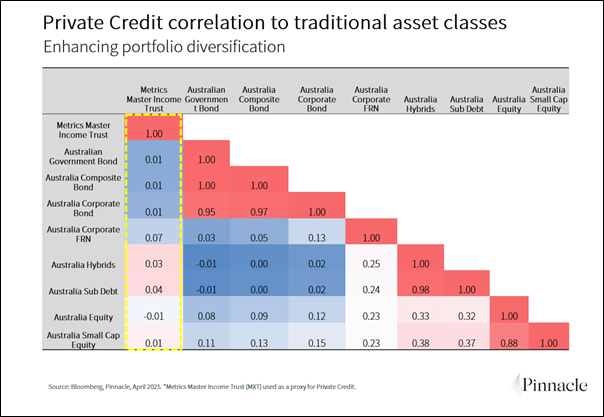

Private Credit’s correlation with traditional asset classes

The relevance of private credit to portfolio construction, and its role in delivering portfolio diversification benefits, lies in the fact that private credit performance typically moves independently from traditional asset classes. The chart below highlights the low or negative correlation of private credit to both bonds and equities.

Chart 2: Private Credit* correlation to traditional asset classes. Metrics Master Income Trust (ASX: MXT) used as a proxy for Private Credit.

A positive correlation of +1.0 indicates different assets will perform in tandem, whilst a negative correlation of -1.0 indicates assets will move in the opposite direction to each other. As public market assets have moved in tandem, private credit’s low correlation profile (-0.01 and 0.01 with Australian equities and government bonds respectively) provides critical diversification for the Australian investor.

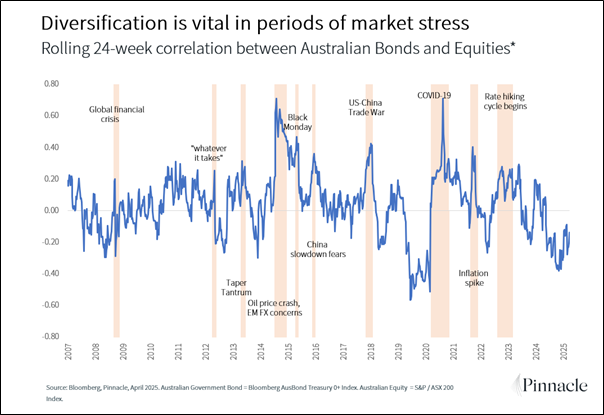

These benefits are particularly important in periods of market stress, when correlations between asset classes tends to spike higher and move into positive territory.

Chart 3: Rolling 24-week Australia Bond/Equity correlation. Source: Bloomberg, Pinnacle, April 2025.

Recalibrating portfolios for evolving market regimes

Private credit now stands as a critical component of a balanced portfolio of assets. Public markets have become more and more short-term in nature, with turnover rates and average holding periods rapidly declining. Sentiment swings can drastically move prices higher and lower.

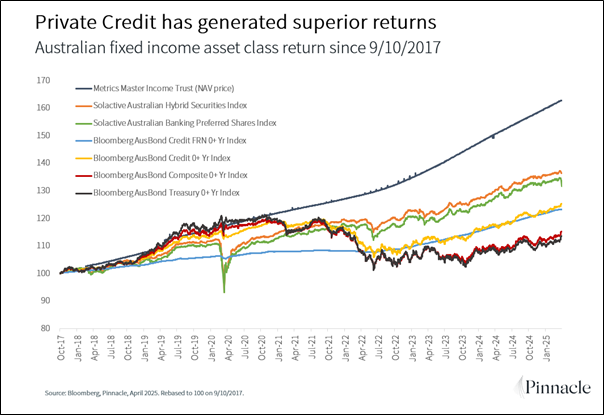

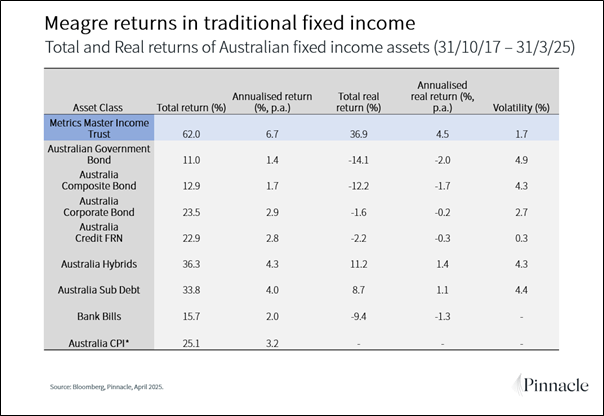

This decade, the public fixed income asset class has not provided the diversification benefits that it has done in the past. This was largely the result of a cocktail of low yields, high inflation, and rising interest rates.

Total returns from fixed income have been poor since 2017, while high inflation has meant that the average real fixed income return has been negative (i.e. the return adjusted for inflation).

Chart 4: Total returns of Australian fixed income asset classes (9/10/17– 2/4/25). Source: Bloomberg, Pinnacle, April 2025. Past performance is not a reliable indicator of future performance. IPO of Metrics Master Income Trust 9 October 2017.

Table 1: Total and real returns of Australian fixed income asset classes (31/10/17-31/3/25). Source: Bloomberg, Pinnacle, April 2025. Past performance is not a reliable indicator of future performance. NAV price used for Metrics Master Income Trust. IPO of Metrics Master Income Trust 9 October 2017.

Adjusting defensive allocations for current and future markets

Since 2017, the Metrics Master Income Trust (ASX: MXT) has produced superior returns with lower volatility. Its low correlation profile to both Australian equities and bonds, has provided critical diversification for those investors seeking attractive risk-adjusted returns.

Private credit’s diversification benefits stem from three structural factors:

- Lower volatility: Unlike public fixed income, private credit valuations reflect contractual cash flows rather than daily changes in the views on the direction of interest rates and overall market sentiment swings.

- Borrower-Lender Alignment: Direct lending agreements include covenants, controls and collateralisation absent in public markets, decoupling the investment from the heavy impact of broader macroeconomic drivers seen with public bonds.

- Economic sensitivity: Metrics Credit Partners lends to large-scale corporates who are less impacted by the economic cycle. According to ASIC Corporate Insolvency Statistics for FY24, over 99% of insolvencies were from businesses with $10M or less in assets - small businesses that Metrics does not lend to.

Empirical validation comes from the 2022–2024 rate hike cycle, where Australian private credit maintained 6–8% net returns despite 15% declines in composite bond indices, demonstrating negative beta to duration risk.

An opportunity to modernise the 60/40 portfolio

While many investors may focus on the ability of private credit to diversify and lower overall risk within their portfolios, the ability of the asset class to meaningfully enhance returns cannot be overlooked. The long-term nature of many private credit investments makes their potentially enhanced return profile even more appealing to Australian investors.

Additionally, as private credit investments are unlisted, short term ‘mark-to-market’ valuation volatility within a portfolio, likely during periods of market stress with listed investments, is less of a concern.

Private credit now rightfully stands as a long-term strategic allocation within a balanced portfolio of investments, and one that is likely to continue to provide important diversification and return benefits in the years ahead.

In times of market stress and uncertainty, sometimes the best offence is a good defence.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Anthony Doyle, MBA (Lond.), MEcSt, BCom, is a distinguished voice in global financial markets with over two decades of expertise spanning asset management, investment strategy, and economic analysis. As Chief Investment Strategist at Pinnacle he provides strategic guidance on investment portfolios and assists in building strong relationships with clients and stakeholders across the financial industry. Doyle's career has been marked by influential positions at leading firms including Firetrail, Schroders, Fidelity International, M&G, and Macquarie Group. His deep expertise encompasses global equities, multi-asset portfolios, and fixed income investments.

........

This communication is prepared by Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as distributor of the Metrics Master Income Trust (the Trust) and is intended for advisers only. The Trust Company (RE Services) Limited ABN 45 003 278 831 AFSL 235 150 (Perpetual) is the responsible entity of Metrics Master Income Trust (the Trust). Metrics Credit Partners Pty Ltd ABN 27 150 646 996 AFSL 416 146 (Metrics) is the investment manager of the Trust. Pinnacle believes the information contained in this communication is reliable, however, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. To the extent permitted by law, Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Pinnacle.

Past performance is not a reliable indicator of future performance, and the repayment of capital is not guaranteed.

The information is of a general nature only and has been prepared without taking into account your objectives, financial situation or needs. Before making an investment decision, you should consider obtaining professional investment advice that takes into account your personal circumstances and should read the current product disclosure statement (PDS), Target Market Determination (TMD) and any ASX announcements of the Trust. The PDS for the Trust is available from invest@metrics.com.au and the TMD for the Trust is available at www.metrics.com.au.

5 topics

2 stocks mentioned

Anthony Doyle, MBA (Lond.), MEcSt, BCom, is a distinguished voice in global financial markets with over two decades of expertise spanning asset management, investment strategy, and economic analysis. As Chief Investment Strategist at Pinnacle he...

Expertise

Anthony Doyle, MBA (Lond.), MEcSt, BCom, is a distinguished voice in global financial markets with over two decades of expertise spanning asset management, investment strategy, and economic analysis. As Chief Investment Strategist at Pinnacle he...

Expertise

Comments

Comments

Sign In or Join Free to comment