Strike While the Iron Ore is Hot

Iron ore, the bulk commodity that underpins the Australian economy, has continued to power along largely undisrupted despite the global economic uncertainty from COVID19.

Demand never faltered as expected whilst supply has continued to be challenged with Brazil supply the main culprit. This has resulted in booming iron ore prices across all benchmark grade specifications, which have reached multi-year highs in mid-2020.

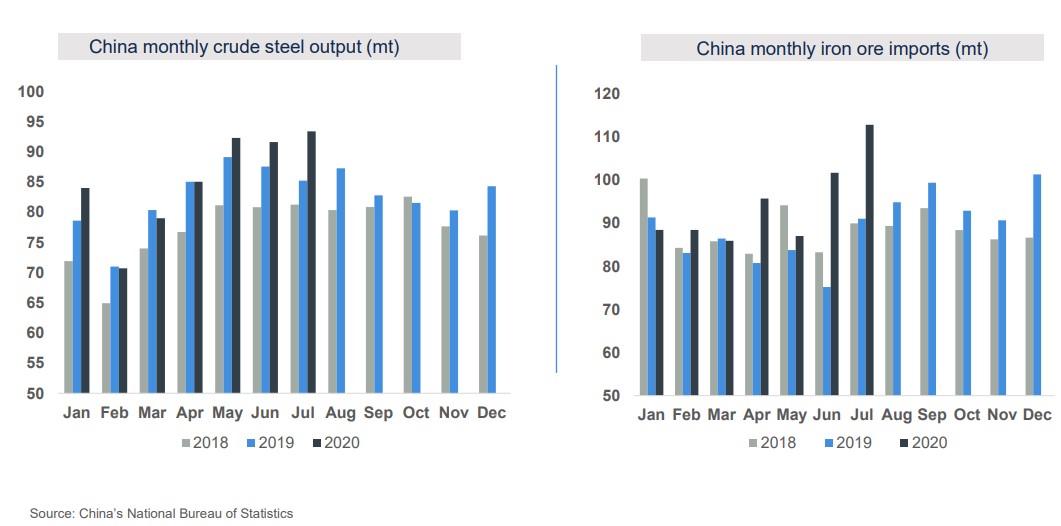

Supporting iron ore demand, we’ve seen China sustain high rates of steel production despite an elevated domestic steel inventory build-up and unwind. Adding to demand pressure is the increase in steel production, from the rest of the global economy as it emerges from COVID19 lockdowns.

Source: Fortescue Metals Presentation August 2020

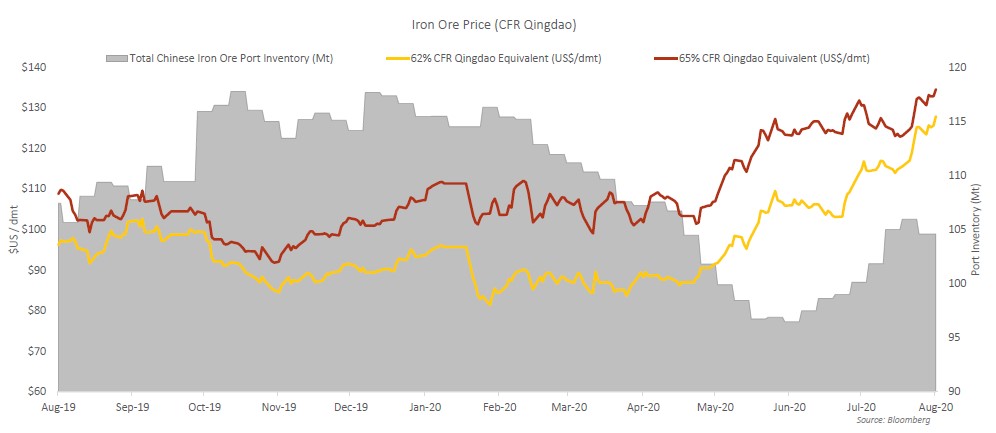

This has led to sustained iron ore demand and weaker port inventory levels in China.

Source: Fenix Resources Presentation August 2020

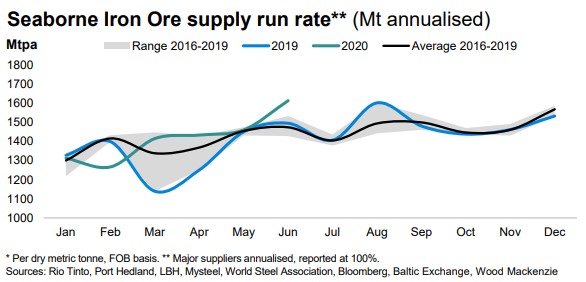

At the same time supply has languished from major producers with Vale in particular having issues getting product to market. The remaining seaborne market has barely kept up with demand and despite being above historical trend recently, it has not slowed down price pressures.

Source: Rio Tinto Presentation July 2020

The initial consensus was that these conditions would unwind in a rapid fashion, but that now looks unlikely. It is more likely to unwind over a few years as production growth returns from Vale and FMG and that provides an opportunity to capitalise on these buoyant conditions in the near term. I believe Fenix Resources (ASX:FEX) and Strike Resources (ASX:SRK) are two stocks to play this thematic.

Iron ore is essentially a scale infrastructure game thus it is generally hard for a company to take advantage of a price boom in the short-term unless it already produces and can squeeze incremental tonnes out of its assets. It can take years and billions of dollars for large scale projects to get product to market and in that time, prices could moderate and jeopardise the ROI of a major investment. In addition, since the peak in 2011, shorter prices cycles have not been supportive of funding major new projects with incremental supply additions being concentrated amongst the major producers.

However, smaller DSO (Direct Shipping Ore) projects, which are typically lower capex but higher opex, can take advantage of price booms as they can be in production and selling product within a much shorter time frame (3 to 6 months from decision to mine). What I think ones needs to look for in these types of projects are the following attributes:

- Relatively high grade and relatively low impurities to attract broad customer interest

- At or near surface ore which requires little to no processing and has a low strip ratio i.e. DSO that only requires being crushed and sorted into lumps and fines

- Easy access to higher cost logistics options such as trucking thus avoiding infrastructure capex typical of larger iron ore operations whilst also controlling your route to market

- Local customers short of supply or available port capacity to export to customers, with the later important for Australian projects

- Located in a jurisdiction that has a smooth permitting and approvals framework that supports speed to market

When scouring through the few remaining iron ore juniors on the ASX, only two meet these criteria being Fenix Resources (FEX) with their Iron Ridge project and Strike Resources (SRK) with their Paulson’s East project.

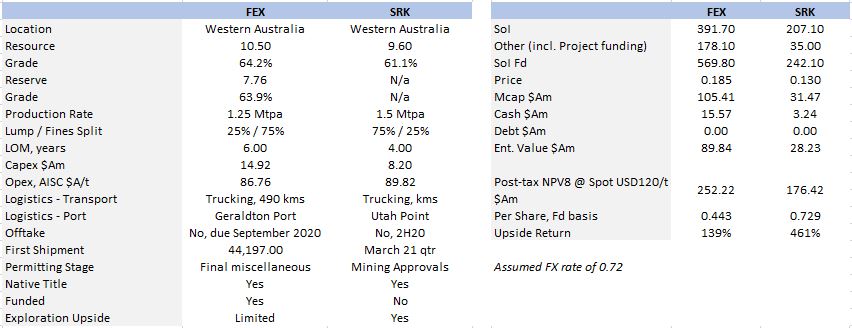

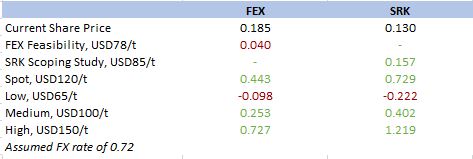

FEX acquired its project from a private group who vended it in late 2018. The project was originally discovered by Atlas and sold off when they were struggling during the lows of the iron ore market in the mid-2010s. FEX has since proved up the resource, approximately doubling it to 10.5mt @64%, and has progressed feasibility and the requisite major approvals to be in a position to mine and ship in January 2021. The project has mining inventory of 8Mt @64% and is aiming to produce 1.25Mtpa over 6 years. At the time of the feasibility, the project was expected to deliver $16.4m in EBITDA per annum at a price of USD78/t ($0.70 FX rate), however, at current levels EBITDA would be $85m+ p.a., in which EBITDA is approximately equal to pre-tax free cashflows. The post-tax NPV8 of the project at spot is ~$252m or ~$0.44/sh. Whilst exploration upside is limited, FEX has flagged they would look to partner or acquire similar deposits in the surrounding area or along its transport route otherwise cash would be returned to shareholders.

SRK has held the Paulson’s East project since 2006 and has been the smallest of a portfolio of projects held over the company’s history. With the bust in the iron market in the mid-2010s, the company put the project on the back burner until late last year after the initial resurgence in the iron ore market. The project has a resource of 9.6Mt @61% and an indicative mining inventory of ~6Mt @60%+ with a big skew to lump. SRK also has exploration upside along strike that could increase the resource by up to ~50% (subject to a drill campaign to confirm). The revised scoping study in April 2020 explored a mine producing 1.5Mtpa over 4 years and a move from shipping via Onslow to shipping via Utah Point, Port Headland. At the study price of USD85/t ($0.63 FX rate), the project would be expected to deliver $35.12m in EBITDA, whilst at current levels EBITDA would be $89m+ p.a. The post-tax NPV8 of the project at spot is ~$176m or ~$0.73/sh. SRK is relatively higher risk as it is dusting off an old project and is earlier in the timeline of progressing a project relative to FEX, however, this is compensated by the higher upside it offers should they successfully go into production in early 2021. None of the valuation includes SRK’s Peruvian iron ore, Argentinian lithium or Queensland graphite projects, which offer development optionality from the cash generated from the Paulson’s East project.

A summary of each company and the key details of their projects are listed below:

FEX and SRK meet the key project attributes listed earlier, thus I believe they make compelling investment opportunities to capitalise on the current elevated price level in iron ore. Both companies have:

- Relatively high grades at 64% and 60% respectively with low impurity penalties. SRK has a bias to higher valued lump ores which attracts premium pricing.

- Both are DSO operations with ore from surface and low strip ratios of 2.86 and 2.50 respectively, which only requires basic on site crushing and screening operations.

- Both have trucking options that can get product to ports capable of handling iron ore.

- High demand for higher grade ores from offshore buyers as indicated by multiple offtake offers FEX has received to date.

- Both assets are in WA, one of the best mining jurisdictions in the world, and have had little issues progressing permitting, approvals and native title agreements to date. Once all approvals are in hand, both operations can be shipping ore within 4 months from decision to mine.

Outside of a collapse in the iron ore market, the main risks for both companies from here are typical of project development and includes completing all permitting & approvals, securing offtake, securing funding, securing contractor window and meeting production timeframes, etc…

FEX is much more progressed, and de-risked, on its project with just offtake, final port agreements and smaller miscellaneous permits to go to enable production in early 2021. As SRK is less progressed to date, it still several key hurdles to progress including the final feasibility study (due Sept 2020), various mining permits and approvals in addition to securing offtake, funding, securing port access, transport and mine contractors, etc…

Whilst iron prices are high now and pressure remains to the upside, one has to be cognisant that prices could moderate and correct from here, particularly if Vale can get production and sales back on track (short-term) whilst some growth projects out of other majors like FMG come on line (medium term), when dealing with high costs production assets like FEX and SRK.

As such, assessing NPVs over a range of price levels is key to determining the risk/reward of these opportunities. As both have all in costs of ~$A90/t, the iron ore price would have to collapse to relatively extreme lows to knock these projects out completely and with little indication this is a high probability event near term, it rules out the most extreme downside risk from investing in FEX and SRK. Even if the price moderates materially too US100/t, both projects will generate material profits whilst the NPVs remain above their current fully diluted market caps. This means investors can still generate attractive returns and realise value creation as both companies move into production even in a moderating iron ore price environment going forward.

The iron ore price has continued to surprise to the upside over 2020 and at this point in time it looks like relatively higher prices will persist near term. The larger pure play producers, such as FMG and CIA, have re-rated materially in line with the iron price and their cashflow generation, however, as higher prices persist, I expect more attention to flow through to the remaining juniors which is the typical progression in flow of capital in a mining price cycle.

All junior names will run, however, I believe the most durable returns will likely come from those who can quickly bring projects to market quickly and generate cash flow from sales.

For that reason, FEX and SRK are my two top picks.

Disclaimer: Any information contained in this article is limited to general information only, whilst the opinions and views detailed are those of the author only, and as such does not constitute advice or a recommendation in any capacity. The information contained in this article has not taken into consideration your specific financial needs, goals or objectives, so please consider consulting a licenced adviser before considering acting on this information.

The author owns shares in FEX and SRK at the time of publishing.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Joshua has worked as an Investment Analyst across different verticals of the financial sector for 10+ years. Experience includes equities research (long/short), manager research and multi-asset portfolios.

3 topics

4 stocks mentioned

Independent Analyst

Joshua has worked as an Investment Analyst across different verticals of the financial sector for 10+ years. Experience includes equities research (long/short), manager research and multi-asset portfolios.

Expertise

Independent Analyst

Joshua has worked as an Investment Analyst across different verticals of the financial sector for 10+ years. Experience includes equities research (long/short), manager research and multi-asset portfolios.

Expertise

Comments

Comments

Sign In or Join Free to comment