Telehealth: The hero Australia deserves or just the one it needs right now?

In one of the most significant events in digital health history, the merger of two of the largest publicly traded virtual care companies, Teladoc (NYSE: TDOC) and Livongo (NDAQ: LVGO) - soon to be called Telavongo, a virtual care behemoth at valued US$38bn was announced last week.

The stakes are heating up, and we're beginning to see significant scale achieved in markets such as the US for virtual healthcare. Hims & Hers a venture capital-backed business also announced its plans to IPO through a potential SPAC after raising USD$197m to date valuing the business that provides digital health prescriptions at over a USD$1bn.

We've been diving into the future of Telehealth & virtual care and whether it is here to stay and which companies are servicing this sector both in Australia, NZ and globally.

Enter COVID-19: Clearing the historical obstacles to adoption

Aggressive lockdowns caused many GPs and allied health professionals to become essentially closed or reduced to a minimal physical operating capacity. Hundreds of medical practices around Australia and thousands of doctors & healthcare professionals had to come up with technical solutions seemingly overnight. COVID provided the backdrop for the surge in telemedicine, but it wasn't enough on its own.

- Medicare Benefit Applied to GP e-consults:

Before COVID, the Medicare Benefits Scheme only applied to rural and remote medicine and Indigenous medicine in regional communities.

While there have been other remote options available for the last 10 years, customers would have to pay extra for the same services as going in-person to see a doctor, as much as $70-100 out-of-pocket per consultation. Acting as a natural handbrake on-demand and part of the reason adoption has been slow.

In March 2020, Prime Minister Scott Morrison announced a $669m package for Telehealth allowing for Australian "whole of population" Telehealth. Australians thus now have free telehealth access to GPs, as well as some medical specialists, mental health treatment, and chronic disease management, thanks to changes rushed through to combat COVID-19. Bringing the pricing of telehealth consults in line with that of in-person consults, effectively removing the price barrier of adoption.

2. B2B2C and two-sided marketplaces gain traction:

In the old system, a platform would have to either signup medical practices, who would, in turn, have to onboard and train doctors on how to use the software. Doctors are traditionally time-poor and in this use case are critical drivers required to push the online option to their customers during in-person consults or via messaging and signage in the GP surgery. Unsurprisingly, this was a complicated process and platforms have struggled to gather uptake.

Another model was a marketplace, a platform that would facilitate interactions between their in-house contracted practitioners and customers coming to their web platforms. This model previously has gained a level of traction but has battled with a small addressable market given the lack of government subsidy as the medical fees are entirely out-of-pocket.

Pre-COVID, the demand and supply sides faced structural disincentives to their embrace of healthcare as a technology-first approach and no need to innovate or push to change.

Since GP surgeries and health practitioners have had limited operational capacity under lockdown, the supply-side obstacles in the marketplace have been removed. Practices and GPs have signed up with technology providers actively pushing their patients to Telehealth. The step-change required to grow the telehealth ecosystem and force change by the practitioners. Interestingly, we already see a falling-off of usage and adoption as restrictions have eased-up (sorry Melbourne).

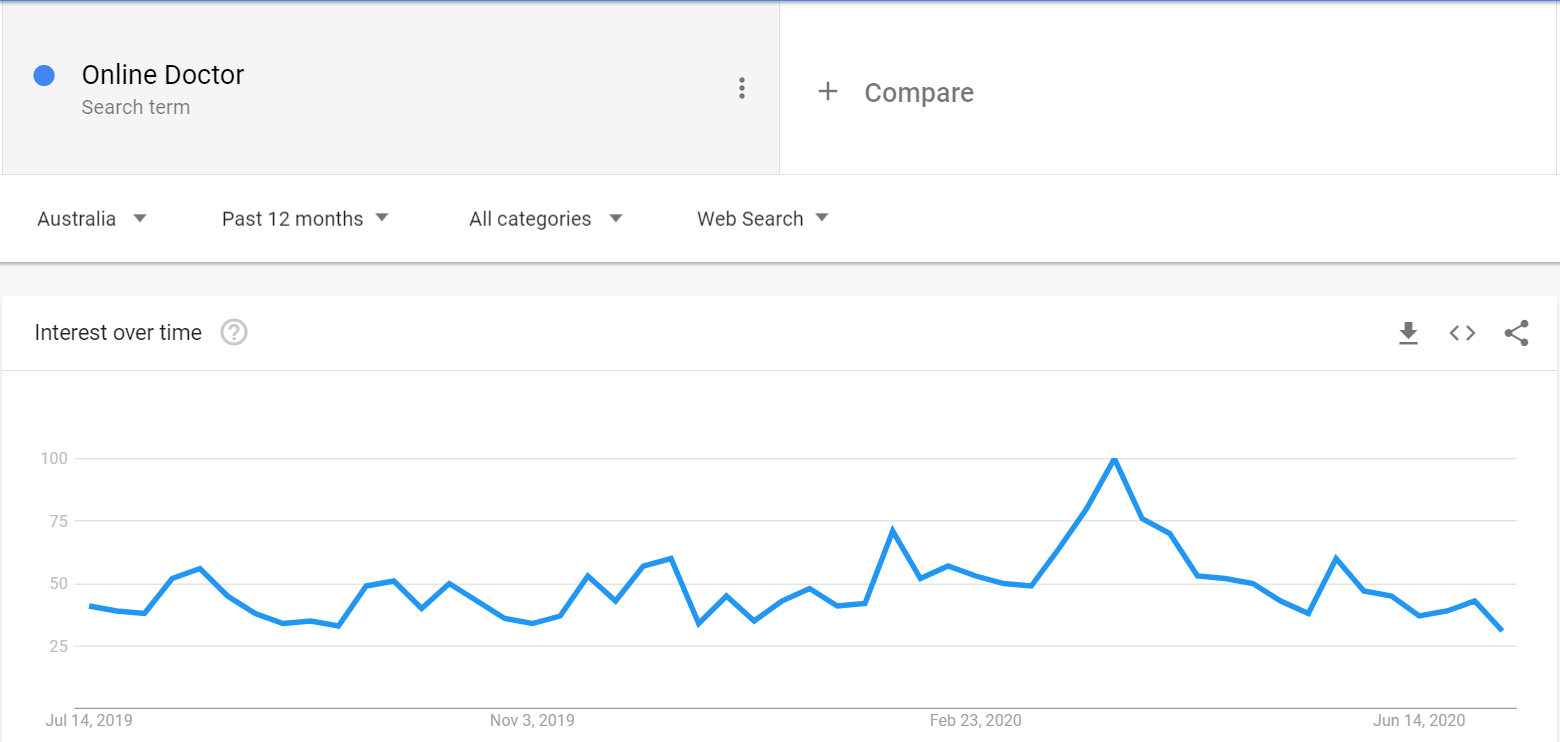

Demand Sharkfin: There's a pandemic, but will Telehealth stay?

During the peak of the first lockdowns in mid-late March 2020, there was a spike in traffic across all trend data for Telehealth, and then a steady decline.

Source: Google trends

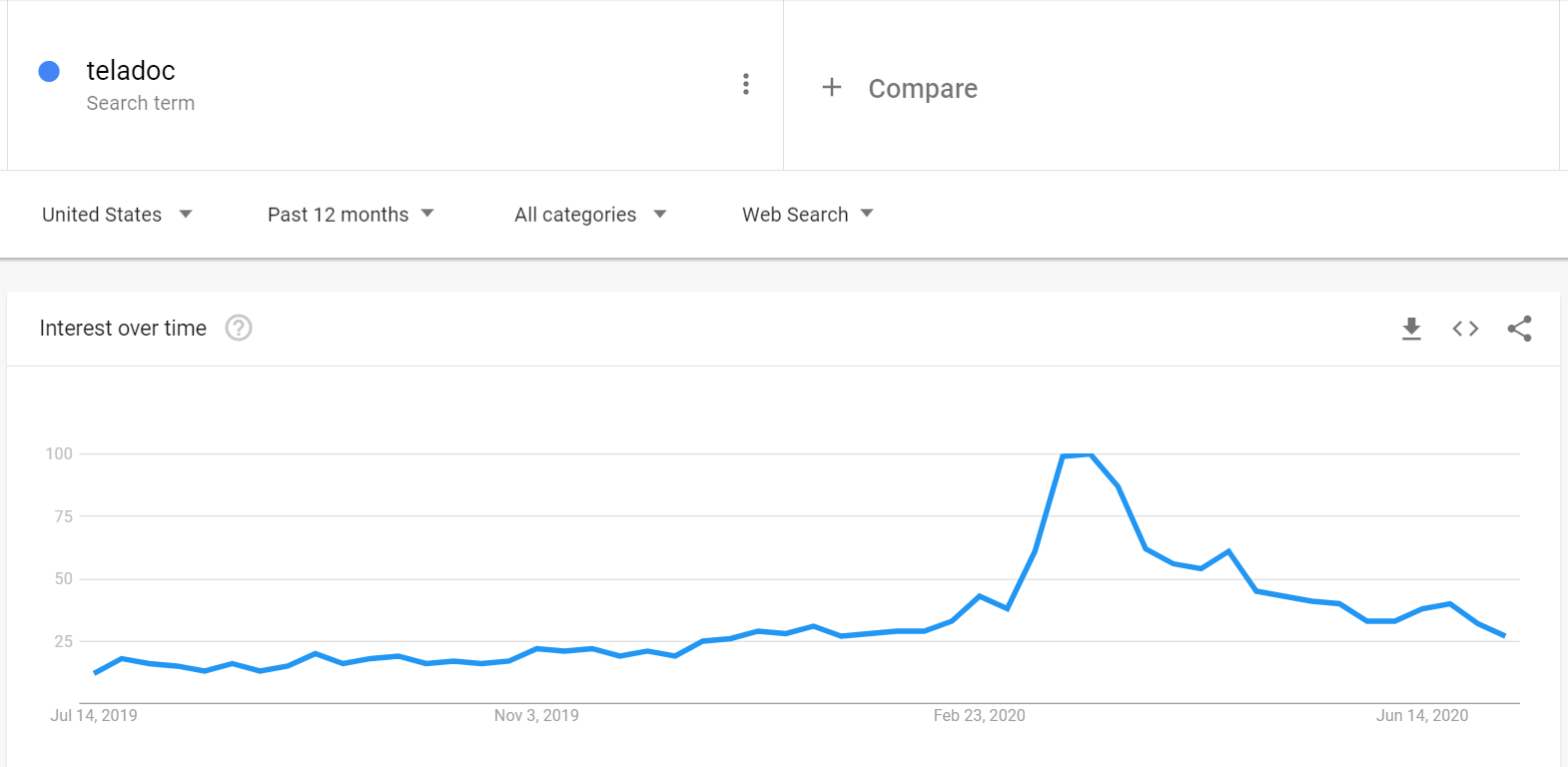

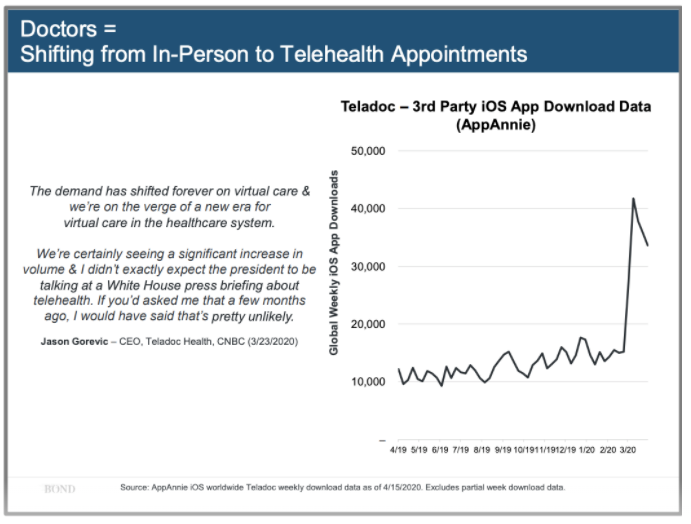

None more so than in the search trends for Teladoc. Teladoc (NYSE: TDOC) is up almost 200% ($193.72 from $65.39) in 12 months and has doubled since the spread of COVID. Public markets (in the US) are viewing Telehealth as one of the markets where there will be a permanent change in consumer behaviour post-COVID.

Source: Google trends

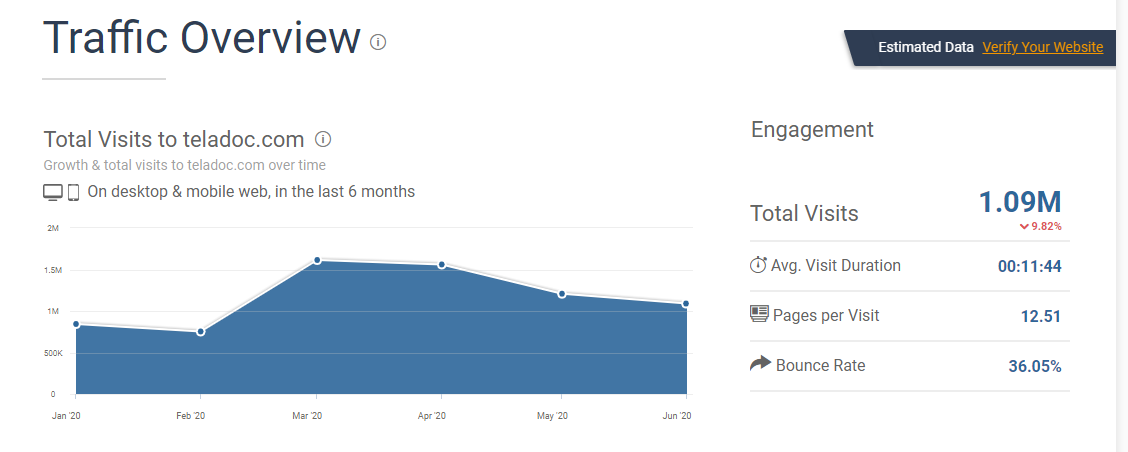

And rightly so. At first glance, the data might suggest that demand is returning to pre-COVID levels, but web traffic data is telling a different story. Telehealth businesses are riding the sharkfin in organic search and retaining the customers they gained during the pandemic. Telehealth is a seasonal business (as people get sick more often during winter) and Teladoc is now experiencing 10-20% more web traffic (in US summer) than at its season peak in January (US winter).

Source: https://www.similarweb.com/website/teladoc.com/

Source: https://www.axios.com/mary-meeker-coronavirus-trends-report-0690fc96-294f-47e6-9c57-573f829a6d7c.html

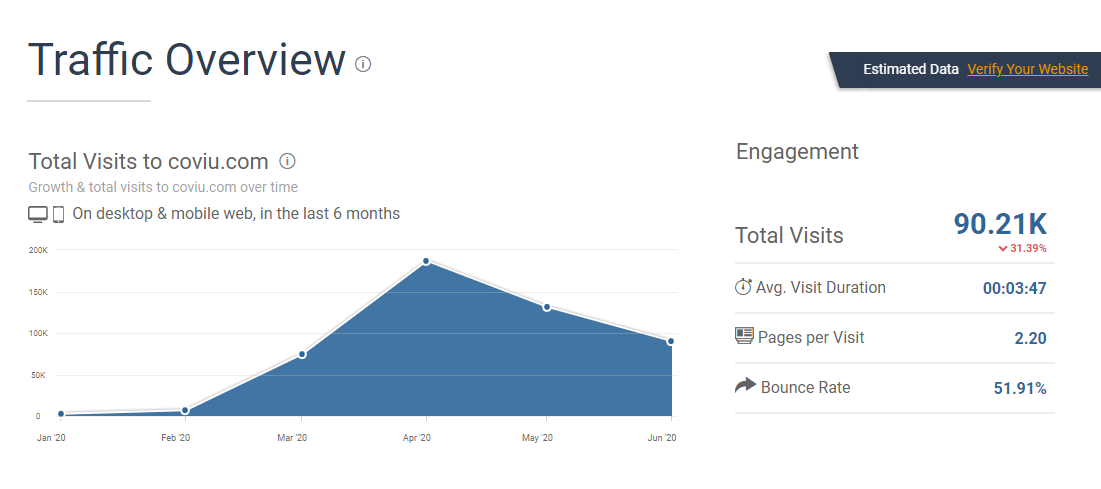

Australian Startups are showing similar trends:

Source: https://www.similarweb.com/website/coviu.com/

Coviu is a private company that provides a telehealth platform as a service, and have recently signed a significant deal with the government to power their HealthDirect service.

We have seen many players move into this space with companies like Coviu, Medinet, and Well Revolution in NZ growing exponentially and shipping weeks worth of product in just days to meet the exponential demand of Telehealth over the last 6 months. In the US, we expect that the Telehealth companies will convert some of their customers to remote-first healthcare evangelists in a post-COVID world. Still, Australian telehealth adoption faces a different headwind to long-term adoption when regulation reverts to pre-COVID levels.

Rise of Direct-to-Consumer (D2C):

We expect that the first wave of successful virtual health brands will come from the rise of primary & elective care solutions delivered via D2C brands and platforms across the Australian market such as Eucalyptus - raising money from W23 (ASX:WOW venture arm) to create a pool of D2C brands such as Kin (female fertility) and Pilot (men's health), or Rosemary Health which recently launched their asynchronous healthcare offering covering a wide array of conditions. Others such as Eugene Labs - creating at-home genetic testing for couples before pregnancy and cancer risk tests. Maxwell Plus leveraging AI to provide prostate cancer testing and Helfie recently launched to detect skin cancer.

Innovation starts at the fringes and keeps working until it gathers momentum. With D2C you can market directly to the consumer and provide a service that is far superior to the existing format. Customers pay out of their pocket yet value the service and solutions enough to continue to pay.

Australia v.s. US

In the US, telemedicine was already on the rise before COVID. We know this from the growth in Teladoc and Livongo, as well as investor interest in platforms such as Oscar and Doctors on Demand. We expect that in the US many of the customers will remain converted post-COVID.

D2C healthcare brands are a well-trodden path with similar successful models growing at spectacular rates with US players such as Hims, Hers, Roman Healthcare (closed US$200m raise last week) & Lemonaid.

The US healthcare system run on a user-pay system, where customers have private health insurance, platforms such as Oscar and Teladoc are getting integrations with insurers so that users can access their benefits in-app and straight away. While some customers fall under Medicare social security and can benefit from subsidised Telehealth, the US is far from a universal healthcare system such as Australia's. From a pricing standpoint, visiting a doctor in person and over video is the same. The customer purchasing decision isn't underwritten or influenced by anything other than the core healthcare value proposition of telemedicine against in-person healthcare, which isn't the case for Australia.

Remote medicine in Aus: will it stick?

There is a view that post-COVID the Federal Government's focus will be on getting the economy back in shape and repairing the fiscal deficits racked up during COVID. Accordingly, widely government-supported Telehealth is unlikely to continue in its current form and is anticipated to roll-back to its pre-COVID position without medicare subsidies.

In Australia, a roll-back of the Medicare subsidy will re-institute the old barriers to primary care telehealth adoption, which existed pre-COVID-19. Customers will be substantially more out of pocket for e-consults, and doctors will be left without a monetary incentive to join with lagging customer demand. We hope that there will be a permanent and lasting increase from the 235k telehealth consults which occurred last year. Still, we don't believe that Telehealth will become a significant threat to in-person healthcare until there's some form of Medicare subsidy.

In a cruel irony, one of the best systems of universal healthcare in the world such as Australia has created this perverse incentive for non-remote healthcare and hence may end up with a system where healthcare is less accessible than in US.

Telehealth is the hero Australia deserves and the one it needs now and in the future. But it's unlikely to be on the payroll after COVID.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Stew Glynn is the Managing Partner & Co-Founder of TEN13. A co-investment platform that provides sophisticated investors access to exciting private early-stage technology deals.

........

TEN13 Management Pty Ltd ACN 634 071 579 (CAR No 127663) and TEN13 Nominee Pty Ltd ACN 634 071 597 (CAR 1276658) are Corporate Authorised Representatives of Lanterne Fund Services Pty Ltd ACN 098 472 587, under Australian Financial Services Licence 238198 (together the 'TEN13 Entities') and are authorised to provide advisory and dealing in connection with investments to wholesale clients only.

Any advice provided by the Ten13 Entities is without taking account of your objectives, financial situation and needs. Potential investors should do their own due diligence and make their own investment decisions, consulting with licensed legal professionals and investment advisors for legal, tax, insurance, or investment advice. The provision of information in this email does not constitute an offer of securities or interests of any kind. No warranty is made as to the accuracy of the information in this email and, to the maximum extent permitted by law, the TEN13 Entities disclaims all liability for any loss or damage which may be suffered by any recipient through relying on anything contained or omitted from this email.

4 topics

1 stock mentioned

Stew Glynn is the Managing Partner & Co-Founder of TEN13. A co-investment platform that provides sophisticated investors access to exciting private early-stage technology deals.

Expertise

Stew Glynn is the Managing Partner & Co-Founder of TEN13. A co-investment platform that provides sophisticated investors access to exciting private early-stage technology deals.

Expertise

Comments

Comments

Sign In or Join Free to comment