Telstra's Trump moment

Daniel Mueller

Vertium Asset Management

Prior to Telstra's FY17 result, media articles abounded speculating the company was going to announce the securitisation of its recurring NBN payments. The media cited various analyst reports that a securitisation of up to $18 billion was about to create a capital management bonanza for shareholders.

Investors expecting an $18 billion securitisation windfall were soon to be disappointed. At the FY17 results, Telstra announced the intended securitisation of just 40% of its recurring NBN payments worth between $5-5.5 billion, implying $13-14 billion of value for the entire infrastructure cash-flows. And less than a fortnight later, the proposal was blocked by NBN Co.

But don’t blame the media or analyst community for the fake news. We should look no further than Telstra itself.

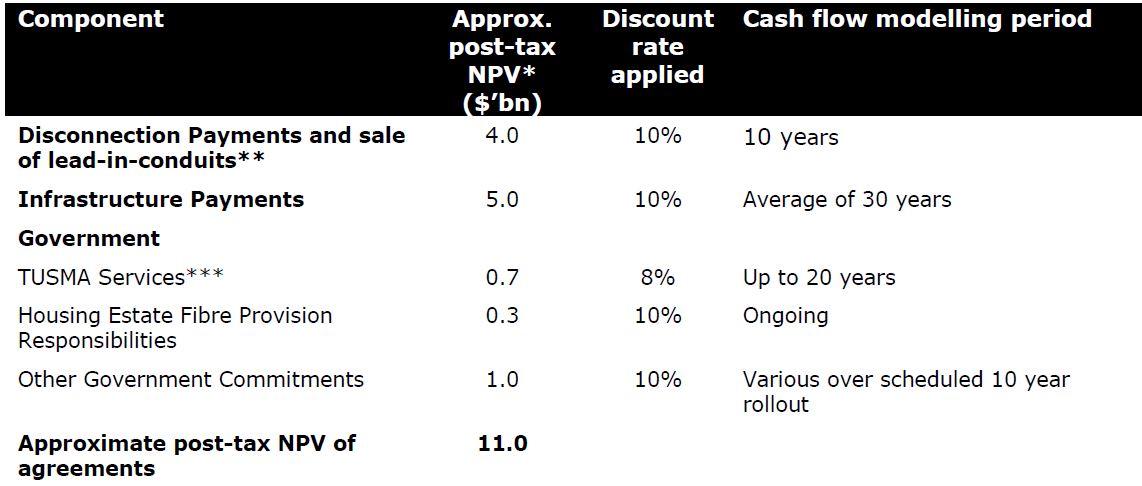

In June 2011, when Telstra’s share price was languishing around $3, the company signed an agreement with NBN Co estimated to be worth $11 billion post-tax net present value (NPV) to Telstra’s shareholders.

Figure 1. NBN compensation to Telstra

Source: Telstra signs NBN Definitive Agreements, 23 June 2011

Since 2011, shareholders have been wondering whether Telstra was adequately compensated for the earnings loss resulting from the NBN. In 2011, we just had the cloak and dagger number of $11 billion NPV and it seemed like a good deal for Telstra shareholders. Management even took the deal to shareholders who voted in favour of it.

But these NBN payments have been shrouded in mystery. Telstra management has treated NBN payments with the secrecy afforded classified information. They would have done ASIO proud.

The information vacuum has led to fake news. Millions of mum and dad shareholders want to know what’s going on with their investment and most importantly, what dividend stream they can expect. Analysts and journalists have desperately tried to provide this information. So, perhaps it wasn’t strictly fake news as there was no intention to mislead. Rather, the intention was to inform, but the quality of information was low.

The Rumsfeld factor

What exactly is low-quality information?

To quote former US Secretary of Defence, Donald Rumsfeld, “known unknowns”. Telstra has had lots of known unknowns associated with the NBN. We believe the greater the unknowns, the lower the conviction we should have in supporting an investment idea. And Telstra’s information disclosure was the perfect example.

In keeping with Rumsfeld speak, Telstra shareholders had to figure out three main known unknowns associated with the impact of NBN:

- NBN one-off disconnection fees

- NBN recurring fees

- Loss of fixed-line earnings

Known unknown 1: NBN one-off disconnection fees

The one-off payments refer to NBN disconnection fees where Telstra gets paid every time a customer switches from the Telstra network to NBN. In 2011, these were valued at a NPV of $4 billion, using a 10% discount rate. Telstra has been reticent to give much about the timing or amount of these payments. Perhaps this is partly because it depends on the speed of the NBN roll-out.

However, at its FY17 result Telstra finally gave some guidance around the one-off NBN receipts. From 2011 to 2017, about $1.5 billion one-off payments have been paid to shareholders. And management finally provided a rough road map to the remainder of the one-off payments with $4 billion expected from the end of FY17 to the end of the NBN migration. However, given their new dividend policy of paying out 75% of the one-off payments, shareholders will only receive $3 billion.

Known unknown 2: NBN recurring fees

The recurring payments refer to the fees NBN Co pays for leasing Telstra’s ducts, racks and backhaul. In 2011, these were valued at a NPV of $5 billion, using a 10% discount rate. Like the non-recurring NBN payments, Telstra has been reluctant to give much away.

The ‘whisper’ cash-flow numbers around the market were that these payments would be around $1 billion per annum once NBN was rolled out. And this is where much of the speculation has been in regard to their true value, because some investors believe they should be valued on infrastructure-type multiples.

At its FY17 result, Telstra confirmed the speculation by guiding to just under $1 billion per annum of NBN recurring cash-flows by the end of the migration period. And contrary to what they revealed in 2011, where the infrastructure payments were worth $5 billion NPV (or $9 billion in the 2017 time frame using a 10% discount rate), it was worth an astonishing $13-14 billion if securitised. This extremely large value was implied by their guidance of monetising $5-5.5 billion of value from their 40% share of the infrastructure payments sold. The key reason for the uplift in valuation was the hope infrastructure investors would value the infrastructure cash-flow stream at a much higher multiple (or lower discount rate) than the rest of Telstra’s business. Unfortunately for Telstra shareholders, two weeks after their results, NBN Co blocked the securitisation proposal.

Known unknown 3: Fixed-line decline

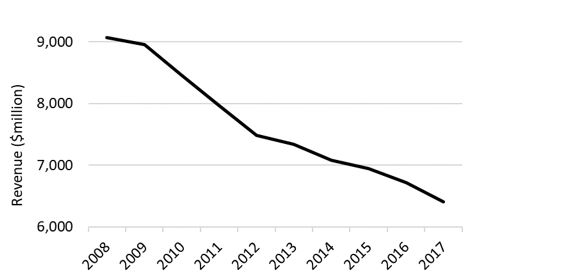

Telstra’s fixed-line business has been in decline for over a decade. As broadband superseded dial-up, customers no longer needed to rent multiple lines. This was compounded by fixed-to-mobile substitution, with some customers deciding they no longer needed a fixed line at all. It was difficult to forecast when this decline might end and at what base level of revenue.

Figure 2. Telstra’s fixed-line revenue

Source: Telstra

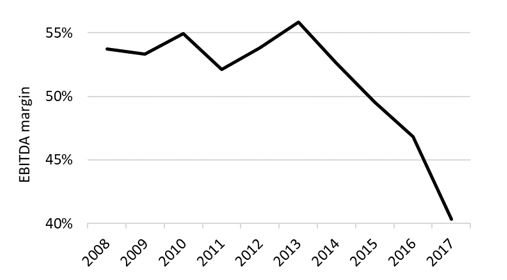

Despite this, fixed EBITDA margins had held up remarkably well, at least prior to NBN. For me, this phenomenon was almost inexplicable. How can a business with high single-digit revenue declines maintain a stable margin?

Part of the answer lies in the accounting treatment around how Telstra allocates costs. While Telstra’s revenue transparency is fantastic with dozens of metrics provided across all products, cost transparency is poor. The company reports just three lines across the entire group for operating expenses: labour, goods and services purchased and other expenses. It would appear costs are largely allocated by product revenue. In other words, if fixed-voice revenue declines, Telstra simply allocates less cost to it. So, the margin impact was minimal up until 2014, as can be seen from the following chart.

Figure 3. Telstra’s fixed-line EBITDA margins

Source: Telstra

But all that changed once the NBN roll-out commenced. The wholesale access cost of NBN was now identifiable. Each customer on NBN now had an associated cost that had to be allocated to the revenue they generated. Fixed margins could no longer be artificially supported by allocating costs to other products. As a result, they have gone into freefall.

Where fixed margins ultimately end up remains largely unknown. In 2011, Telstra provided no guidance as to how the NBN might impact their fixed-line earnings. In 2016, the company guided to a wide range of $2-3 billion per annum loss of fixed-line earnings. And then, at its FY17 result, Telstra guided to around a $3 billion per annum loss. However, this loss in earnings includes the $1 billion per annum NBN infrastructure payments. Hence, the real earnings loss is gross $4 billion per annum.

Smoke and mirrors? You be the judge.

Known knowns

After six years, starting with the opaque NPV values, the known unknowns have slowly morphed into known knowns. The tables below illustrate how investors could have tried to work out the NBN valuation impact on Telstra. Rather than use NPV calculations, which can create quite a lot of confusion, we have used simple earnings multiples to assess the value impact.

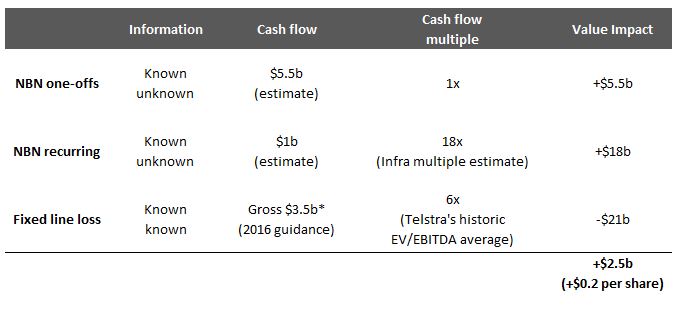

Let’s start with the key NBN information just prior to the FY17 result.

Figure 4. NBN impact on Telstra’s value prior to the FY17 result

*In 2016, Telstra originally guided to $2–3 billion ($2.5 billion mid-point) EBITDA loss from the loss of fixed line earnings. However, this loss in earnings includes the $1 billion per annum NBN infrastructure payments. Hence, gross fixed-line earnings loss is $3.5 billion based on the mid-point of their guidance range.

Prior to the FY17 result, the NBN compensation looks like a marginally positive deal for Telstra shareholders.

Now let’s turn our attention to immediately after the FY17 result.

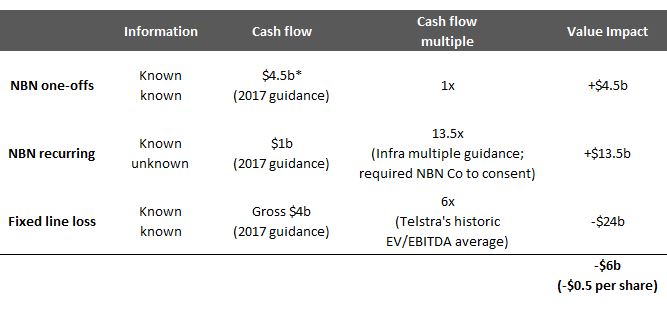

Figure 5. NBN impact on Telstra’s value at the FY17 result

*Telstra paid $1.5 billion to shareholders prior to 2017 from NBN one-off payments based on a 100% pay-out ratio. Under their new dividend policy of paying out 75% of the NBN one-off payments, they plan to distribute another $3 billion from FY17. Hence, the total NBN one-offs that will be paid to shareholders will be $4.5 billion.

NBN compensation now looks inadequate, but not a disaster for Telstra shareholders.

But less than a fortnight after the FY17 result, NBN Co blocked Telstra’s securitisation proposal. Now that it is off the table, the market should value the one-off NBN payments at a lower multiple, say 6x like the rest of the company.

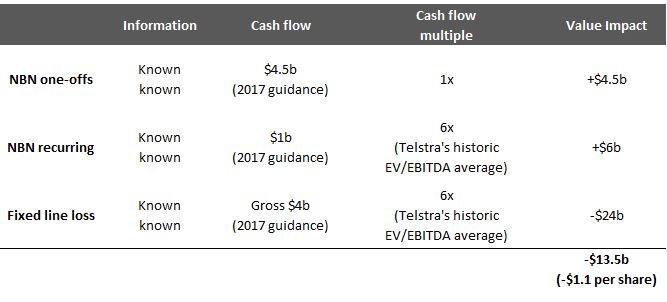

Figure 6. NBN impact on Telstra’s value after the FY17 result

Based on what we know today with a lot of the unknowns becoming knowns, the value loss has become much greater for Telstra shareholders.

Surely the NBN payments are worth more even if there is no securitisation?

In our view, those who valued the recurring NBN payments on an infrastructure multiple were drawing a long bow. The infrastructure company in this instance is NBN Co, not Telstra. If a road maintenance contractor won work from Transurban, should that portion of their earnings be valued on an infrastructure multiple? Or, if an IT services firm won a long-term government contract, should that earnings stream be valued on the same yield as a government bond?

We don’t think so, which is why we value the recurring NBN payments on the same multiple as the rest of Telstra’s divisions.

Some investors may argue that even though Telstra retails fixed-line services, it still owns infrastructure, which it leases to NBN Co. Let’s draw an analogy to illustrate the counter-argument, taking Woodside as an example. It has significant gas pipelines with long-term contracts that it owns on its balance sheet. But the market does not value these infrastructure assets because management does not intend to financially engineer the company to realise their value. Similarly, the market doesn’t value Harvey Norman on a REIT multiple just because the company has a very large property book. And if the property book is unlikely to be securitised, the market values Harvey Norman’s NPAT on about 10 times, an appropriate multiple for a retailer. Another example is Aurizon. More than half of its earnings are derived from below rail infrastructure but the whole company trades on a normal corporate multiple. We can go on and on but you get the picture.

Lessons from Telstra’s known unknowns

Sourcing information from the grapevine is often low quality and should never play a big part in investment decisions. In Telstra’s case, investors relying on the $18 billion securitisation number reported in the financial press should be extremely disappointed. What was considered great compensation in 2011 for a fixed-line business in decline, now seems inadequate as NBN costs are crimping Telstra’s fixed-line margins.

It has become clear there’s no way NBN receipts compensate Telstra for the loss of fixed-line earnings. In other words, there has been a permanent destruction of shareholder value. But it has taken six years for management to make this clear to shareholders.

However, Telstra is not alone in providing opaque information. Scores of other companies often provide vague information to feed a market hungry for it.

As investors, we need to understand the nature of the information we use. The danger is when we create stories based on low-quality information to make the numbers feel real and accurate. Under these circumstances, large spreadsheets with detailed modelling will only give you a false sense of security.

It is only when the information we assess morphs from known unknowns to known knowns, that the information becomes more transparent and reliable. Only under these circumstances can we assess whether to risk clients’ capital on the investment idea. At other times, we will preserve clients’ capital by tuning out potentially fake news.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Daniel joined Vertium Asset Management in 2017 as a Portfolio Manager / Equity Analyst and brings with him nearly 15 years’ Australian equity investment management experience. At Vertium, Daniel assists the CIO and is responsible for researching and analysing Australian companies.

Prior to Vertium, Daniel was a Senior Equities Analyst / Portfolio Manager at Forager Funds where he was responsible for assisting with Forager’s Australian equities portfolio.

Before Forager, Daniel held similar roles at Morningstar, Northward Capital, Investors Mutual, Cannae Capital and MMC Asset Management.

7 topics

1 stock mentioned

Daniel Mueller

Vertium Asset Management

Daniel joined Vertium Asset Management in 2017 as a Portfolio Manager / Equity Analyst and brings with him nearly 15 years’ Australian equity investment management experience. At Vertium, Daniel assists the CIO and is responsible for researching...

Expertise

Daniel Mueller

Vertium Asset Management

Daniel joined Vertium Asset Management in 2017 as a Portfolio Manager / Equity Analyst and brings with him nearly 15 years’ Australian equity investment management experience. At Vertium, Daniel assists the CIO and is responsible for researching...

Expertise

Comments

Comments

Sign In or Join Free to comment