The link between US 10-year Bond Yields & US Stock Returns is Nebulous

Andrew McCauley

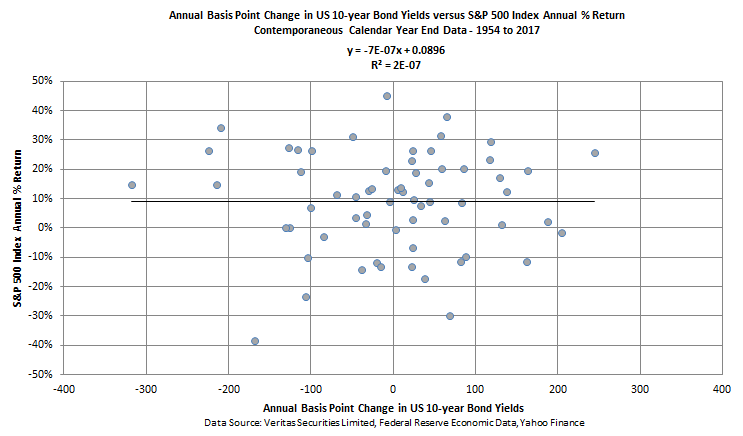

Recently, it’s been hard to miss the inordinate increase in the number of fearful articles written about rising US 10-year Bond Yields and its almost certain negative impact on US equities. The 3% level has had its fair share of the limelight. Well, the data suggests that these fears are largely imaginary. The scatterplot below illustrates the very weak relationship between yield increases and equity returns.

The contemporaneous linear relationship between Annual Basis Point Change in US 10-year Yields versus the S&P 500 Index Annual % Return is described by the equation -7E-07x + 0.0896. The Pearson Correlation between the two series is -0.05% and the R-squared statistic is 2E-07 or 0%, indicating that annual Basis Point fluctuations in US 10-year Yields explains approximately 0% of calendar year S&P 500 Index returns. A myriad of other phenomena (or randomness) explains the other 100% of US equity returns.

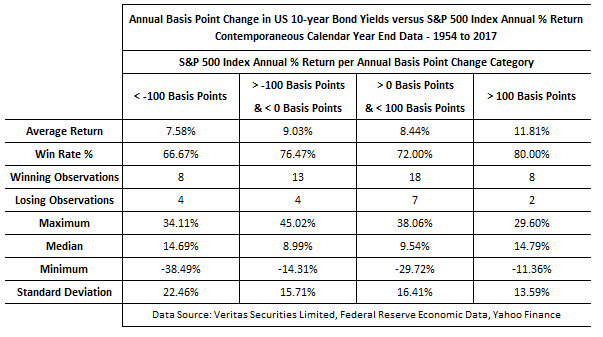

Perhaps placing Annual Basis Point changes in US 10-year Yields into simple categories (low, middle, high) can provide a basis for understanding why so much fear is associated with rising bond yields. As is readily observable from the table below, US equity returns in the lower, middle, and higher categories, basically display average return profiles that are not significantly different. However, I would highlight, that a calendar year yield increase of greater than 100 basis points or 1% provides the highest contemporaneous average return for the S&P 500 Index of 11.81% with 8 up years and 2 down years.

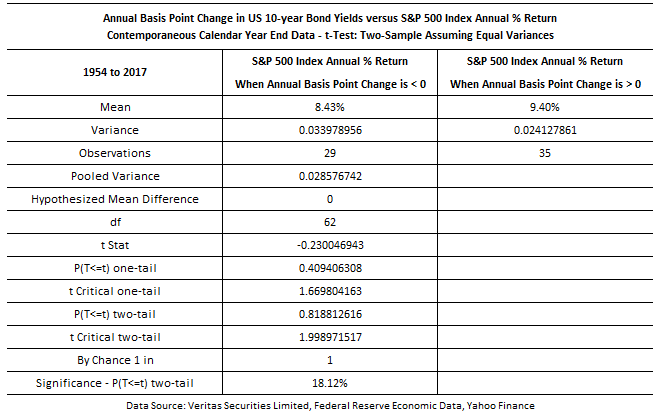

So, in an effort to justify the yield increase fear mongering, I decided one more test was in order. This time I split the data into only 2 categories, Annual Basis Point Change < 0 and > 0, to see whether the respective equity return profiles were statistically different. After running a Two Sample T-Test, it is clear, that Basis Point movements in US 10-year Yields as a stand-alone diagnostic of equity market performance are largely useless. Due to return variability, the mean difference of increasing and decreasing bond yields and its impact on equity returns, is not statistically significant at the conventional 5% level (1 in 20 by chance), and therefore is nebulous at best.

After the Sex Pistols' last gig in San Francisco (1978), Johnny Rotten famously chided his audience, "Ever get the feeling you've been cheated?" Given the continual promotion of financial flapdoodle with regard to rising yields and its universally negative impact on equities, I do, you should.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 25 years’ experience in the Australian financial markets sector with extensive knowledge of both equity derivatives and statistical analysis (predictive techniques). Andrew is responsible for delivering evidence based market analysis to Institutional and High Net Worth clients. Andrew recently co-authored a paper on High Frequency Trading that was published in The Journal of Trading.

Andrew McCauley

Statistical Research & Data Analyst

Andrew has over 25 years’ experience in the Australian financial markets sector with extensive knowledge of both equity derivatives and statistical analysis (predictive techniques). Andrew is responsible for delivering evidence based market...

Expertise

Andrew McCauley

Statistical Research & Data Analyst

Andrew has over 25 years’ experience in the Australian financial markets sector with extensive knowledge of both equity derivatives and statistical analysis (predictive techniques). Andrew is responsible for delivering evidence based market...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why "buy and manage" is the better way to invest in stocks

Livewire Markets