The recession we had to have?

The 24th Prime Minister of Australia and the 2023 bond market may not have a lot in common at first glance.

Many can recall the famous words of Paul Keating (PJK) in 1990 and cold comfort were they to households at the time. The RBA yesterday provided a parallel of icy resolve, this time to financial markets – with the implication being the same: crush inflation by inducing a recession.

Rates – PJK: “Because mate, I wanna do you slowly” 1

The RBA did not surprise the market with a 25bps hike. The RBA did surprise markets with its statement and guidance. The reference to being on a pre-set path was dropped and the Board expected “further increases in interest rates will be needed over the months ahead”.

Whilst this might seem like minutia, the colours have been nailed to the mast, our central bank will continue to raise rates to break the back of inflation. Subliminally they have echoed the famous comments of Paul Keating in 1990 – as continuing to raise rates increases the chance of a local economic downturn.

Local cash rates have increased 325bps in 10 months. This is the largest increase on record since the RBA has been determining the cash rate. Before the meeting, markets were pricing in an implied terminal rate of 3.70%. After the meeting, this is 4.00%. The terminal rate is the expectation of where rates peak, or in other words, what the terminal destination is.

Yesterday, bond and equity markets were sold off the back of this hawkish statement. We have narrowed into the movement of the generic two-year government bond in Figure 2. The generic means the interpolated yield – given the actual bonds themselves have maturities that are not exactly two years, but in between one and three years. The +15bps move took the yield to 3.23%. This move was large compared to history, however, could be run further by markets, given at the back of 2021 and into 2022 we have seen 5 day changes in yields of circa +40-60bps on several occasions. So once this has washed through the system, we still view incrementally and cautiously adding duration as the right trade at this point in the cycle. Cash is also a great trade given the carry and optionality offered.

Many market participants, including the RBA, are concerned about inflation sticking around at elevated (>3%) levels. Stagflation, where the economy grinds to a halt but inflation persists, is also a premonition many talking heads have had (us included); however yesterday the RBA actually reduced that risk. This is because the RBA made clear it will crusade to crush inflation and growth simultaneously. Forward pricing of inflation agreed with this narrative and our 5y5y breakeven ripped tighter. This number (see Figure 3) can be used to imply the market’s average expectation of inflation for 5 years, in 5 years’ time – in other words the average inflation for 2028-2033.

Importantly, even though 5y5y breakevens fell yesterday, they remain within the mid-point of the RBA’s 2-3% target objective. Nonetheless these expectations sit on the higher side of recent history.

In relation to cash rate futures, we remind readers that these are probabilistic in nature, but the movement of the cash rate is deterministic. What this means, is that the futures price all possible outcomes and arrive at the average. The future very rarely plays out to the average – it plays out to a path.

Take the example of a left and right turn in a corridor. Say you are at the end of a corridor with a T-intersection (picture example here), you can only turn one of the two ways, if the chance of turning left and right are both 50%, then the average path would be to go straight through the glass window. This is obviously not a reasonable option.

We view the same dynamic being present in markets now. The left turn is a recession, where inflation comes down quickly, unemployment rises quickly and the RBA is forced to cut rates to help the economy. This is currently our base case in the longer term.

The right turn is stagflation, where inflation sticks around, unemployment rises and the RBA is forced to keep rates high in pursuing its sole-mandate (in effect noting technically it has a triple mandate) of low inflation. We cannot yet rule this case out, but yesterday actually made it less likely.

The walk through the glass, the unreasonable option, is the soft-landing narrative. We currently rule this out – that could change, but not in this environment.

So, whilst the cash rate futures curve in Figure 4 illustrates soft and steady rate cuts to begin in mid-2023 and into 2024, this needs to be viewed through the paths:

- (Right turn) In the event a recession occurs, the RBA will cut rates very quickly. As illustrated in Figure 5, the average cutting cycle is 340bps over 15 months.

- (Left turn) in the event inflation sticks around above target, the RBA will be forced to keep rates high, and possibly even embark on a second hiking cycle (a U-turn if you like).

The RBA are concerned about inflation sticking around (i.e. they do not want a right turn). This is long-term positive to bonds, as the RBA are campaigning to quell inflation and growth simultaneously – which makes high quality fixed income very attractive from a capital return perspective!

For more complicated players a good trade in our thinking is short 2y, long 10y. The RBA’s statements make inversion of our yield curve more likely, as growth expectations should fall. Yesterday in the domestic session that flattened only 2bps – that seems well unders. Our expectations is that the line in Figure 6 will head towards zero.

Amplifying this conviction is the difference between the shape of yield curves locally versus the US. Figure 7 plots the 10y2y yield spread in Australia and subtracts that from the 10y2y yield spread in the US. We are at unseen levels based on the limits of readily accessible historical data.

Takeaways - Rates:

- We view the actions of the RBA yesterday having increased the chance of a local economic recession. Whilst duration (think government bonds) may underperform in the coming days, the RBA has counterintuitively improved the medium to longer term performance prospects. The same cannot be said for more speculative assets like risky credit or equities.

Inflation – “You’re the fella that put the interest rates up” 2

The RBA is rightfully concerned in reducing inflation. It is critical to ensure that price rises are only temporary in nature, otherwise the economy runs the genuine risk of a wage price spiral.

There are positive leading signs out of the US in regard to inflation. This is important because the US has largely led the Australian economy in terms of its experience. Figure 8 shows the close relationship between fertiliser and food prices. Blood and bone has dropped dramatically and it is reasonable to assume inflation drops with it.

Moreso positive, has been the extreme reduction in money supply. We have spoken about this several times, and have viewed it as key to the recent inflation that has been seen.

Going back more than 60 years, the change in the supply of money has never been lower – and this means the number of transactions required to maintain inflation (also called velocity) would be enormous and unsustainable.

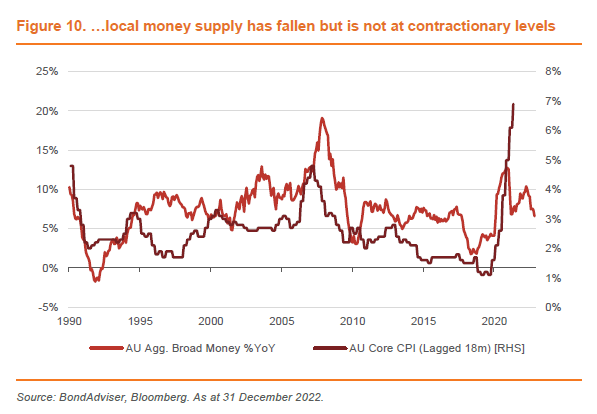

Contrastingly, our local measures of money supply have not fallen as robustly. However, as illustrated in Figure 10, they have fallen, and we expect inflation to fall with it. This chart was key to our initial predictions that inflation would return with a bang and today it provides unsurprising evidence that inflation needs to moderate further.

Indeed, it could be said that the level of broad money is still too high and the RBA could be quicker to tighten or ramp-up its quantitative tightening (taking back the cash it took for bond purchases). Contrary to that argument is Figure 11, which expands on Figure 10 by plotting the differential between the two figures over time. The last time this differential was so low (and we expect it to get lower), core CPI fell from 6.5% to 2.0%. This is when Mr Keating was Treasurer.

Takeaways – Inflation:

- There are distinct positives to the deflation story, both locally and in the US. The unknown remains the prospect of wage price spirals. We are watching this very closely.

- Often wrong never in doubt – the RBA were wrong calling inflation on the way up, why is the market pricing them to be right on its expectations on the way down?

Growth – “Give him a Valium” 3

The mortgage belt is suffering from higher rates. This is not isolated to Australia, nor mortgages. As illustrated in Figure 12, in the US, according to the University of Michigan it has been the most difficult time on record to buy a house, car or durable – stretching back to 1978.

In Australia, far more borrowers than typical are currently on fixed mortgage rates. This has dampened the impact of rate hikes. Unlike the US however, these are not 30-year fixed mortgages. The overwhelming majority are short-term, and CBA expects half of these fixed rate mortgages locally to expire this year.

This means the average borrower with a 2023 mortgage expiry will roll off a 2.25% loan into a >5.00% loan. In that example, on say, a million dollar, 25-year mortgage, repayments will increase at least some $1,500 per month. Here it is correct to say that even if the RBA stop tightening now, a significant amount of residual tightening will still occur in the local economy for the next two years.

Levels of new lending in our housing economy are at GFC-like levels. In fairness, this follows an extraordinarily large increase following COVID – something we attribute to the RBA’s unconventional policies including the ultra-cheap term funding facility (TFF) that banks were able to lend with.

This slowing in credit is not conductive to risk assets. This is well illustrated in Figure 14, where we have plotted the ASX 200’s earnings per share on a quarterly basis against the RBA’s financial aggregate for business credit.

The relationship between credit growth and EPS is also true when using the RBA’s aggregate credit figures and EPS on a last twelve-month (LTM) basis. This is shown in Figure 15.

The negative that investors need to be aware of is that our credit growth is slowing – and we expect this will only speed up. This is shown in Figure 16. We have been advocating for a higher quality bias in credit and for a home bias. This is because as credit supply and economic growth slows, credit spreads; a measure of risk premium for bonds that bear the risk of default, will increase. It increases more severely in bonds that have weaker quality.

We are overweight a home bias given we have: (1) fundamental confidence in our investment grade corporate names – think Telstra, Woolworths, Wesfarmers, Coles, NBN Co, Mirvac, etc, (2) our local market is low credit beta, meaning our mark-to-market movements are not as quick on the way up nor down, and (3) local spreads are already at elevated levels to history as a function of bank TFF refinancing pushing all prices down - this dynamic is not true overseas, where spreads sit at longer term averages – hardly seeming of fair levels with such detrimental headwinds ahead.

In terms of indicators of local growth, PMI and consumer confidence surveys tell mixed stories. We have focused on leading indicators in Figure 17, such as retail trade and property services because they are both discretionary. We have also included sales clerks and new manufacturing orders surveys to paint a better picture of forward growth. The chart is noisy, but all four of these leading indicators have fallen in tandem recently – a worrying sign.

Finally on a lighter note, we close with THE BOOMER SPREAD, a measure we created that shows the degree of dispersion between consumer confidence of those that eat avocado toast at cafes and those that do not. Understandably, those aged 45+ are often burdened with mortgages, amongst other things including car repayments, private school fees and back pain. These are rate sensitive in nature, whilst on the other hand youth unemployment is at all time lows – it was 7.1% in July 2022 (it is now 7.7% according to the ABS) – versus a high of circa 20% in 1992, and ironically for this piece, that was within a year of Mr Keating become the Prime Minister 4.

Also, this record in confidence spread is perhaps a function of the naivety of youth and wisdom of elders. Those in the survey between 18-24 have never really seen the impact of sustained inflation, nor rate rises, nor the prospect of high unemployment rates and a prolonged economic downturn. Ignorance is bliss!

Takeaways – Growth:

- Quality bias – higher quality credits is the place to be in local corporates. Trim the subordinated/warehouse exposures to weak credits ASAP. Openpay is the first domino of BNPL – the sector is quickly realising the funding models do not make sense at these rates.

- The wisdom of age is speaking – markets should listen.

Footnotes:

1 Paul Keating, Parliament of Australia Hansard, Questions Without Notice, 15 September 1992

2 Paul Keating, “7:30 Report” interview, 8 May 2006

3 Paul Keating, Parliament of Australia Hansard, Suspension of Standing and Sessional Orders, 9 February 1995

4 In fairness to Mr Keating, his policies did break the back of inflation, allowing for nearly 30 years of economic growth and wealth creation.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

As Head of Investment Solutions, Charlie is a portfolio manager for BondAdviser’s SMAs, IMAs and model portfolios. He is a voting member of BondAdviser’s Investment Committee, and Credit Committee.

........

BondAdviser has acted on information provided to it and our research is subject to change based on legal offering documents. This research is for informational purposes only.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

The content of this report is not intended to provide financial product advice and must not be relied upon as such. The Content and the Reports are not and shall not be construed as financial product advice. The statements and/or recommendations on this web application, the Content and/or the Reports are our opinions only. We do not express any opinion on the future or expected value of any Security and do not explicitly or implicitly recommend or suggest an investment strategy of any kind.

The content and reports provided have been prepared based on available data to which we have access. Neither the accuracy of that data nor the methodology used to produce the report can be guaranteed or warranted. Some of the research used to create the content is based on past performance. Past performance is not an indicator of future performance. We have taken all reasonable steps to ensure that any opinion or recommendation is based on reasonable grounds. The data generated by the research is based on methodology that has limitations; and some of the information in the reports is based on information from third parties.

We do not guarantee the currency of the report. If you would like to assess the currency, you should compare the reports with more recent characteristics and performance of the assets mentioned within it. You acknowledge that investment can give rise to substantial risk and a product mentioned in the reports may not be suitable to you.

You should obtain independent advice specific to your circumstances, make your own enquiries and satisfy yourself before you make any investment decisions or use the report for any purpose. This report provides general information only. There has been no regard whatsoever to your own personal or business needs, your individual circumstances, your own financial position or investment objectives in preparing the information.

We do not accept responsibility for any loss or damage, however caused (including through negligence), which you may directly or indirectly suffer in connection with your use of this report, nor do we accept any responsibility for any such loss arising out of your use of, or reliance on, information contained on or accessed through this report.

© 2023 Bond Adviser Pty Ltd. All rights reserved.

{kind=link}

{kind=link}

5 topics

As Head of Investment Solutions, Charlie is a portfolio manager for BondAdviser’s SMAs, IMAs and model portfolios. He is a voting member of BondAdviser’s Investment Committee, and Credit Committee.

As Head of Investment Solutions, Charlie is a portfolio manager for BondAdviser’s SMAs, IMAs and model portfolios. He is a voting member of BondAdviser’s Investment Committee, and Credit Committee.

Comments

Comments

Sign In or Join Free to comment