The key isssues for FY18

Alex Moffatt

Joseph Palmer & Sons

In this report from Malcolm Palmer, Managing Partner of Joseph Palmer and Sons, he reviews the financial year gone, and looks to the year ahead, including how and when the post-GFC multi-trillion dollar stimulus process ends, and what it means for markets...

Investment and economic review

Most investment markets performed admirably in the last twelve months, particularly as economic trends have generally been uninspiring. Stock and real estate prices have certainly benefitted from the unprecedented stimulus provided by central banks and governments, in the form of extraordinarily low interest rates, and even more extraordinary money printing programs.

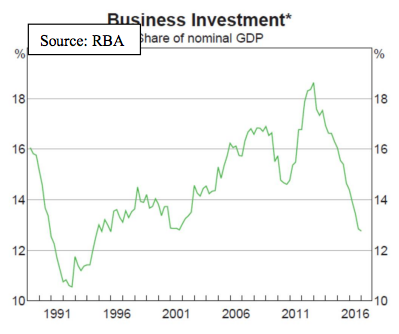

This central bank largesse had the intent (hope) of reflating economic activity and hence jobs, but in reality, has been more beneficial for investment asset prices rather than broad economic growth. There is no better illustration than this chart, which shows a collapse in business investment in Australia despite the extraordinary interest rate settings. This is not a good look.

The primary global economic conundrum ahead is how and when this post-GFC stimulus process ends. The importance of this can’t be understated as the quantum of assets acquired by the central banks is truly enormous – more than US$12 trillion, at last count, by the troika of the US Federal Reserve, European Central Bank, and the Bank of Japan.

Each of these institutions is now contemplating the process of unwinding, either by maturing or reducing bond purchases or raising interest rates. The pace and consequences of their actions will be watched very carefully in the coming year.

Two rather disparate points of view contest investment asset price deliberations:

- Firstly, the more optimistic case, argues that deflationary risks are dissipating, and global economic activity is on the mend. This view is supported by some improving data, including global PMI (manufacturing expectations) and modest gains in some labour markets, and concludes that profit growth will justify relatively high share prices, even if interest rates rise.

- The second point of view is that there is a wide disconnect between investment asset (shares and real estate) prices, and economic activity, and sooner-or-later weak GDP, retail sales and business investment will drag asset prices lower.

There is some truth in both these perspectives. It is our view that economic activity will generally remain below trend, interest rates remain very low, and asset prices find it difficult to rise very much further for a while. Stock market volatility, which has been subdued this year, will likely increase, such that there will probably be a couple of sharp sell-off periods ahead, during which assets can be acquired at more prospective prices.

There are always geopolitical events to worry the naysayer. This coming year these include the outcome of the German election in September, the momentum of the populist Five Star Movement ahead of Italy’s 2018 election, the diplomatic tensions on the Korean peninsula and South China Sea, and presumably a recognition at some stage by Americans that their commander-in-chief is entirely unsuitable for that role.

Key issues for Australia

Domestically, the primary issue ahead is the potentially calamitous consequences of too much household debt, in the face of waning employment growth and stalling house prices. At best, this issue is likely to lead to slack consumption and retail sales growth, but could turn very ugly indeed.

We remain concerned that share and real estate prices are somewhat disconnected from underlying economic activity, and for much of this year we have been expecting markets to encounter some bumps. To date, stock market setbacks have been relatively minor and real estate prices have proved resilient. Nevertheless, the outlook is beset with uncertainties, so we are retaining our cautious investment stance.

Economically, we expect the weak trend in retail sales, consumption and the labour market to continue, offset by strong tourism and servicessectors and robust construction activity. Interest rates will remain low and share prices will suffer some short-term pitfalls. This would be a generally satisfactory outlook if it were not for the frightening level of household and government debt.

We don’t have a lot of room for error...

Full report here

This is an extract of a report from Managing Partner, Malcolm Partner, for the full report, including our views on domestic equities, global equities, property, and rates please click here:

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Alex Moffatt has almost 40 years’ experience dealing in equity, debt and currency markets in Australia, the UK and USA. He has worked at several companies in the wealth management industry, including Schroders in the UK. A director of Joseph Palmer & Co, Alex is authorised to provide advice on equities, fixed income securities, managed investment products and superannuation strategy and products.

8 stocks mentioned

Alex Moffatt

Director

Joseph Palmer & Sons

Alex Moffatt has almost 40 years’ experience dealing in equity, debt and currency markets in Australia, the UK and USA. He has worked at several companies in the wealth management industry, including Schroders in the UK. A director of Joseph...

Expertise

No areas of expertise

Alex Moffatt

Director

Joseph Palmer & Sons

Alex Moffatt has almost 40 years’ experience dealing in equity, debt and currency markets in Australia, the UK and USA. He has worked at several companies in the wealth management industry, including Schroders in the UK. A director of Joseph...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Don't let all time highs stop you buying this "bull" market

Centennial Asset Management

Equities

Four founder-led companies worth watching

Blackwattle Investment Partners