The sky is not falling, but storm clouds are brewing

The sky is not falling was the message in September 2017. Our message was that the overall market did not show excessive valuations, which generally is a precursor to stock market corrections. However, our market outlook dimmed due to recent ‘risk-on’ rally, where most of the year’s return was delivered in the last three months. While large-cap industrials generally exhibit reasonable valuations, we are beginning to observe pockets of irrationality, with prices running ahead of fundamentals. In the following commentary, we highlight two areas of the market where we believe risk is taking a back seat.

1st storm cloud: Small-cap valuations

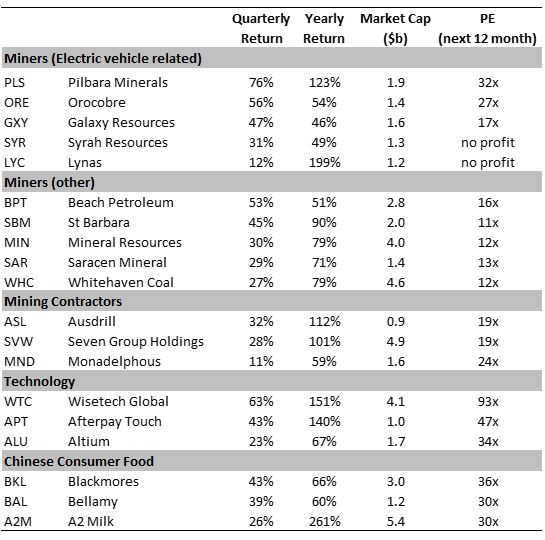

In 2017, small companies (S&P/ASX Small Ordinaries Accumulation Index) delivered a total return of 20%, trouncing their larger peers (S&P/ASX 100 Accumulation Index), which delivered 11% total return. Small-cap stocks with very high multiples and/or volatile earnings have performed very well (maybe too well) over the quarter. Specifically, in the current environment there is a lot of hype and momentum in miners (where related to electric vehicles, revived commodity prices and mining contractors), technology and Chinese consumer food themes.

Table 1. Small-cap stocks exposed to hot themes

Source: Vertium, Factset

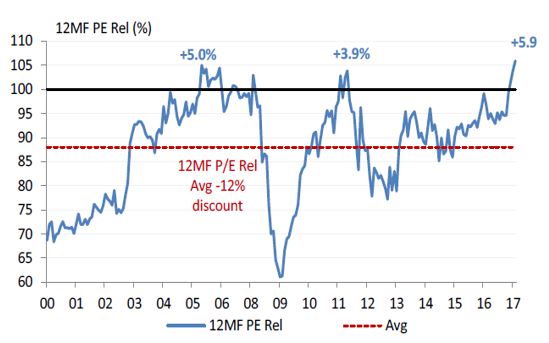

After the surge in valuations over the quarter, small caps relative to the top 100 stocks are now at extreme levels. If history is a guide, this is not sustainable.

Chart 1. Relative PE multiple of the S&P/ASX Small Ordinaries Accumulation Index versus the S&P/ASX 100 Accumulation Index

Source: Morgan Stanley

When growth is hard to come by in our challenged macro environment, investors are increasingly prepared to pay higher prices for any growth. The ‘fear of missing out’ mentality is turning many high-priced securities into lottery style tickets: very slim odds with the perception of winning large pay-offs.

No doubt, the pay-offs are large for fantastic businesses that can reinvest at high returns on capital for a very long period. However, when you attempt to pay extremely high prices for perceived growth companies, two things work against you:

- A wonderful business at a high price can be a terrible investment. For example, Walmart is a fantastic company that once was a high-flying growth company. Since its IPO in the 1970s as a small company, its share price has delivered double-digit returns for almost 30 years. But it all came to a standstill in late 1999 when it’s one-year forward price earnings (PE) multiple hit 50x. By the end of the next decade, Walmart had experienced fantastic growth with earnings per share (EPS) nearly tripling. However, its share price was more than 20% below its 1999 peak! It was a wasted decade for Walmart investors.

- Finding a wonderful business with a long runway for earnings growth is rare. There is a very good chance that most stocks in a portfolio will not exhibit long-term earnings growth like Walmart. While short-term earnings growth may look intact, over the long term the law of averages applies – very few companies can sustain high growth rates. Hence, growth perceptions can be very fickle.

When a mediocre business is bought for a very rich price, it sets the foundation for extreme volatility. It was not long ago that we observed some high-flying small-cap stocks that crashed when their stellar growth stories changed. For example, Mayne Pharma (MYX) was a recent market darling because earnings were revised up by about 80% over two years prior to its share price peak in August 2016. When the euphoria was at a crescendo the stock’s PE multiple hit 27x making it a giant among its small-cap peers with a market capitalisation of $3.2 billion. However, the fear of missing out mentality quickly dissipated when the company revised its profits lower in late 2016. Consequently, MYX’s share price collapsed and it was the worst performing small-cap stock in 2017 delivering a -48% total return.

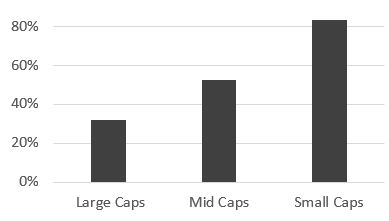

MYX is not an isolated case because small-cap stocks in general exhibit high levels of volatility (other notable mentions include TPG Telecom, which lost 60% from peak to trough, and APN Outdoor, which lost 35% in one day!). Changing perceptions, leading to excessive share price volatility, is to be expected more so from small-cap stocks compared to large-cap stocks. Over the last decade, the average price range between the 12-month high and the low for small-cap stocks is about 83%. As illustrated in chart 2, the price range of small caps is historically about three times greater than that of large-cap stocks.

Chart 2. Average price range (12-month high and low) for large, mid and small-cap stocks between 2006 and 2016

Source: Vertium, Factset

2nd storm cloud: Resource valuations

While the top 100 stocks have been left behind by the small-cap sector, the Resources sector within the S&P/ASX 100 Accumulation Index has been on fire. The S&P/ASX 100 Resources Accumulation Index has returned 24.2% in 2017. In comparison, the S&P/ASX 100 Industrials Accumulation Index delivered a modest 8.5% return.

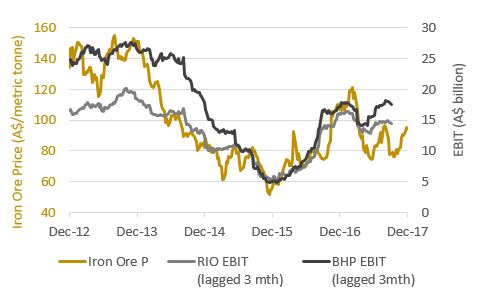

Since the commodity price scare in 2015, resource giants like BHP Billiton (BHP; 14.7% quarterly return) and Rio Tinto (RIO; 14.0% quarterly return) have taken substantial steps to lower their operating costs and deleverage their balance sheets. However, it does not change the fact their profits are significantly driven by the iron ore price: 44% of BHP’s earnings and 70% of RIO’s earnings were derived from iron ore in 2017.

Chart 3. AUD iron ore price versus BHP and RIO’s rolling EBIT (next 12 months)

Note: EBIT is lagged by three months to the iron ore price because it takes about three months for sell side analysts to revise their earnings estimates. Source: Vertium, Factset

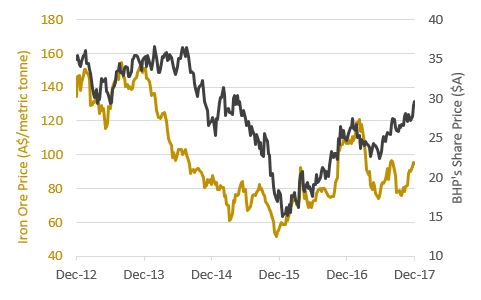

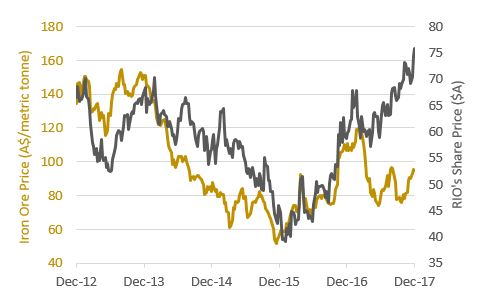

Consequently, the share prices of both BHP and RIO generally track the iron-ore price.

Chart 4. AUD iron ore price versus BHP’s share price

Source: Iress

Chart 5. AUD iron ore price versus RIO’s share price

Source: Iress

However, unlike previous years where there was a positive relationship between movements in the iron ore price and BHP and RIO’s stock prices, 2017 was an extremely odd year. The share price of BHP and RIO rose 18% and 27% respectively despite the AUD iron ore price falling 15%. Given such a large disconnect, their elevated share prices are implying a strong outlook for iron ore prices. Time will tell whether this will happen, but we believe the odds are against it.

China accounts for around two-thirds of world iron ore demand, so any changes in the country’s marginal demand has a profound impact on iron ore prices. Unfortunately for the resource bulls, we believe the conditions that led to a significant increase in iron ore prices in CY2016 are unlikely to be repeated. To stave off a recession in 2015, the Chinese Government implemented enormous stimulatory measures. Its fiscal expenditure growth rate jumped from 10% in the prior year to 18% (equivalent to a 16 trillion RMB injection) and monetary policy was aggressively eased (interest rates dropped from 6% to 4.35%). The stimulus led to the tail winds of strong infrastructure spend and property construction, which underpinned steel demand, resulting in a sharp iron ore price rebound in 2016.

Backing up the enormous fiscal stimulus of 2015, the Chinese government did not disappoint when it announced its 13th five-year plan (2016 to 2020) to spend 13.4 trillion RMB on more than 300 projects on roads, railways, waterways and airports. Their flagship mega-projects include:

- Belt and Road Initiative: the modern-day equivalent of the old Silk Road trade route to connect China to more than 65 countries across Asia, Europe, the Middle East and Africa.

- Jing-Jin-Ji development: to create a megalopolis connecting Beijing, Tianjin and Hebei with significant transport infrastructure so that 130 million people within that region can move around with ease.

- Yangtze River Economic Belt: to strengthen logistics and transport infrastructure that covers 11 provinces including Shanghai. The region accommodates almost half of China’s population and generates more than 40% of China’s GDP.

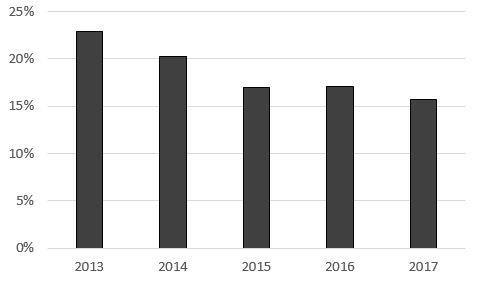

While the large infrastructure spend is impressive, it is important to note the growth rate has decelerated from the previous five-year plan and has been relatively steady in recent years. Stable growth rates in infrastructure spend mean it does not create extra marginal demand for iron ore.

Chart 6. Chinese infrastructure fixed-asset investment yearly growth rate

Source: Vertium, National Bureau of Statistics of China

The steady infrastructure spend since the start of the 13th five-year plan reflects recognition within the Chinese government that debt is growing faster than GDP at an unsustainable rate. The Bank of International Settlements estimates China has a total debt-to-GDP ratio of 256%. Over the last two years, China has attempted to control its debt binge by maintaining its budget deficit to around 3% of GDP. For 2018, authorities have recently announced they will be maintaining the same budget deficit as prior years. Hence, for the foreseeable future, infrastructure spend is expected to remain steady.

While we do not think Chinese infrastructure spend will add more to incremental iron ore demand, we have concern about recent cyclical weakness in property construction. The monetary stimulus implemented in 2015 had the unintended consequences of stoking a property bubble, which China’s richest man, Wang Jianlin, in 2016 declared was the “biggest bubble in history”. As we debate how to cool Australian house prices, in China there are now strong policies to curb property speculation. This includes the requirement that second home buyers put up at least half of the purchase price in equity and home resales are banned within two to three years of purchase.

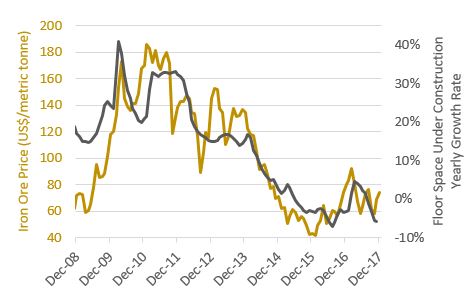

Strict macro-prudential policies and recent increases in interest rates have led to property prices cooling and a fall in property construction. While many commentators cite current strong steel margins to underpin iron price demand, it ignores the fact steel producers are selling into a weaker real estate construction market. The latest yearly growth rate of floor space under construction is now running at -6%. The cyclical nature of Chinese property construction means this large segment of the Chinese economy has a significant impact on the marginal demand for steel and indirectly iron ore. Hence, it has a strong influence on the iron ore price.

Chart 7. USD iron ore price versus Chinese floor space under construction yearly growth rate (3mma)

Source: Vertium, National Bureau of Statistics of China, Iress

China is now running hard to stand still. There is no longer a cyclical uptick in property construction. With share prices of iron-ore related companies implying higher commodity prices, there is a disconnect between the perception and reality of what is happening in China. Accordingly, we remain cautious on iron ore-related companies.

Perceptions change far more often than the fundamentals. So, when valuations are stretched, then buyer beware – volatility works both ways.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

15 topics

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Comments

Comments

Sign In or Join Free to comment