The Upside of Time in the Market

“Time in the market beats timing the market – almost always.” - Ken Fisher

The idea of being able to time the market is emotionally appealing. After every significant market dislocation, the popular business press will carry the story of the market wizard who got it just right. The catch is that from one correction to the next, it is rarely the same wizard. The reality is that most professional investors get it partly right and a few will get it horribly wrong. On top of that, it can be awfully hard to tell in advance who will get the timing right. It is very highly likely that the manager who gets their timing just right will have been wrong for a period before the dislocation, only to get lucky in the eleventh hour. An old market adage is “to be early and wrong are indistinguishable” – and that is a truism for good reason.

So, what should the individual investor do so as to best “time the market”? Solid portfolio returns are derived much more through time in the market rather than by timing the market. Some data and stories will help to explain why.

I am reminded of an old colleague and a story he told me years ago. During his time in university he

invested about $4k in an investment fund. He graduated, started a successful career and as life got busy

forgot about the investment. Then in 2008 whilst tidying up he found the investment statement, and it

turned out that over the past 19 years the position had increased in value to more the $60k, a return of

15x on his initial investment. At one point within the 19 years, although still up substantially on his initial

investment, the fund experienced a 50% drawdown. If he hadn’t forgotten about the initial investment

he likely would have panicked and sold in an attempt to protect the gains he still had. Although liquidating

may have felt comforting at the time, in the subsequent years he would have missed out on the gains that

accrued from that point.

Casinos all around the world provide a useful analogy. Imagine: we’re in Las Vegas on the main gaming

floor and a punter is on a winning streak at the roulette wheel. The pit boss is looking increasingly sweaty

and furious, the crowds are gathered around the hot player cheering them on and admiring how clever

they appear to be. Yet the casino plays on, because they know they have a small statistical advantage and

whilst they might lose today, over the weeks, months and years ahead the advantage of being ‘in the

market’ will compound, ensuring the casino is the ultimate winner in the long run.

The same rules apply to investing: in the very short run the probability that an investor receives a positive

return is evenly balanced. Importantly, as an investor extends their time horizon, the probability of a

successful outcome skews more and more in their favour.

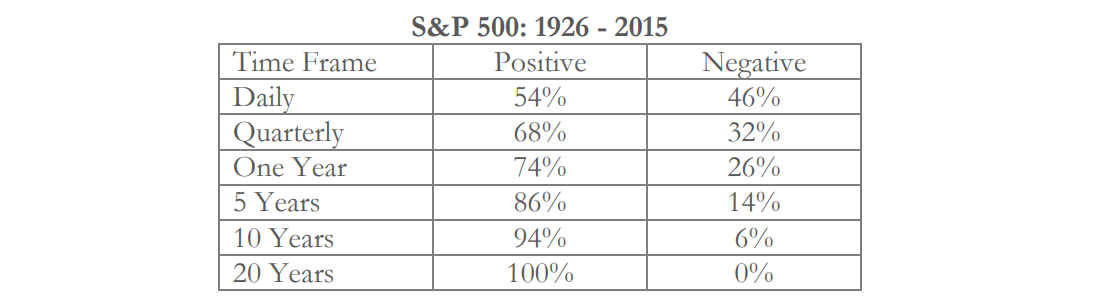

Looking at historical S&P 500 data we find that;

- On a given day it is a coin toss as to whether you receive a positive return.

- In a full year there is about a 74% chance your portfolio has a positive return.

- With a decade long horizon your chances of a good outcome are better than 94%, and

- Extend your timeframe to 20 years and you will almost certainly receive positive returns

I know what you are thinking: if you’re disciplined about your ‘timing’ strategy (and you time the market

perfectly) the benefits would be significant. Yet on the contrary, a London based fund manager by the

name of Albert Bridge Capital has produced a study on market timing showing this isn’t the case. The

study demonstrates that with a long enough time frame and consistent reinvestment the absolute worst

market timer does almost as well as the very best market timer. In their study they demonstrate that the

investor who allocated $1000 to the S&P 500 on the worst (highest point) each year from 1989 to 2018

would have a portfolio worth almost $122k. The investor who allocated $1000 on the best (lowest point)

each year would have a portfolio of $155k. The study was replicated over multiple 30-year time frames

and found similar results. Contrary to popular belief, the benefits of timing even when done with

complete precision aren’t as large as you might have guessed.

Market timers face some significant challenges, high transactional costs and often a higher tax burden –

but perhaps the most significant challenge is knowing when to reinvest. It is one thing to have the

foresight to go completely to cash; it is another thing to then have the courage to dive back in. Markets

are forward looking and they place a present value on the future; investors, on the other hand, remember

the past. After a significant correction, asset prices begin to rally well in advance of any good news being

evident. The investor sitting in cash inevitably finds it difficult to reinvest if they miss the first 10% of a

rally. Instead. they wait for a good pull back to dive in, reminding themselves regularly, “I will buy when

the market pulls back 10%.” But: what if it doesn’t? There are more than a few investors that have been

only invested in cash since 2010 waiting for a pullback. That perhaps wouldn’t be such a problem if cash

still paid a return greater than inflation; alas those days are gone for now.

So, if timing the market is too hard what is an investor left to do? Be a long-term investor. In parts 1 and

2 of “The Upside of…” (see links at the start of this paper) we covered topics including diversification

and upside vs downside capture. Together with time they form the core of Koda’s investment philosophy.

They are the strategies that will anchor an investor’s ability to ride out the ups and downs of cycles, stay

in the market and ultimately increase the probability that a portfolio achieves satisfactory returns.

It’s important to note the notion of ‘time in the market’ does not in any way endorse a passive, set and

forget portfolio. Changes are necessary from time to time; for example, sometimes holding a higher level

of cash will be prudent, while other times one asset will offer compelling risk-reward characteristics when

compared to another. There are often adjustments to be made along the way.

Most importantly investors must;

- Be diversified across different types of assets with low levels of correlation to one another • Look for value driven favourable risk-reward opportunities

- Seek out niche investments away from the crowds

- Be prepared to make changes

- Manage appropriate liquidity for any shorter-term needs, and

- Maintain the discipline of rebalancing the portfolio.

“A diversified portfolio of investments, each of which is unlikely to produce significant loss, is a good start toward

investment success.” – Howard Marks

Note: This is part three of a trilogy series outlining the principles behind Koda Capital’s investment philosophy: diversification, upside/downside capture and time in the market. Parts one ('The Upside of Diversification') and two ('The Upside of Minimising Downside').

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael Massey is a Partner at Koda Capital and advises family offices and high net worth individuals. Areas of expertise include asset allocation, alternatives, fixed interest, capital markets and risk management hedging strategies.

........

This research note has been prepared without consideration of any client's investment objectives, financial situation or needs. Before acting on any advice in this document, Koda Capital Pty Ltd recommends that you consider whether this is appropriate for your circumstances.

While this document is based on the information from sources which are considered reliable, Koda Capital Pty Ltd, its directors, employees and consultants do not represent, warrant or guarantee, expressly or impliedly, that the information contained in this document is complete or accurate. Koda does not accept any responsibility to inform you of any matter that subsequently comes to its notice, which may affect any of the information contained in this document.

© Copyright Koda Capital 2020 | AFSL: 452 581 | ABN: 65 166 491 961 | www.kodacapital.com

3 topics

Michael Massey is a Partner at Koda Capital and advises family offices and high net worth individuals. Areas of expertise include asset allocation, alternatives, fixed interest, capital markets and risk management hedging strategies.

Michael Massey is a Partner at Koda Capital and advises family offices and high net worth individuals. Areas of expertise include asset allocation, alternatives, fixed interest, capital markets and risk management hedging strategies.

Comments

Comments

Sign In or Join Free to comment