US inflation risk is building

In the next 6 – 9 months, the US inflation outcome will be the key determining factor of both Fed policy and therefore the longevity of this US economic cycle. Current consensus expectations lean firmly towards a low inflation outcome and therefore a dovish Fed with continued, albeit low, economic growth. The market is currently pricing a 29% chance of a hike by September and a 47% chance of a hike by December, which is broadly consistent with recent Fed governor language. Several factors are consistent with that consensus view. Inflation expectations, according to market & surveyed based measures, are at multi-year lows, commodity prices are flat (Y-o-Y), and producer price inflation is close to ZERO. Our inflation models carry a similar message. It’s clear that beyond the US, deflationary pressure is still a key global theme. Read the full story below to understand the risk of rising inflation.

In half of the 22 EM economies that we track, inflation rates are trending down while global wage inflation trends are generally weak.

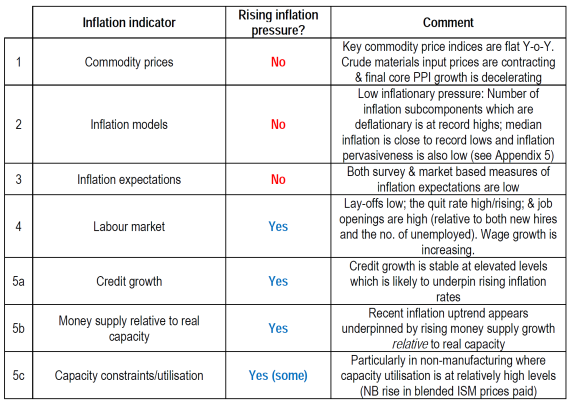

Table 1: Potential sources (and/or measures) of US inflation

With respect to that consensus view (and rows 1, 2 & 3 in Table 1 above), three key points, though, are worth noting: i) much of the weakness in US inflation relates to goods inflation (which is essentially a global inflation rate and is primarily driven by OIL and other commodity prices). Indeed the correlation between OIL (Y-o-Y) and US goods inflation is high. That type of inflation, though, is volatile, mean reverting and therefore largely overlooked by the Fed (especially if domestic inflation pressures are rising). ii) Market & survey-based inflation expectations, which are currently low, are backward looking and reflect the actual inflation outcome (rather than lead/predict future inflation rates). iii) Our inflation models, which currently indicate deflationary pressure, often mean revert quickly once they have reached extremes. Some those indicators are currently at extremes.

Other indicators, in rows 4 – 5 of Table 1, point to building inflationary pressure in the US economy (primarily due to higher services inflation – which is domestically driven). That pressure is from two key sources:

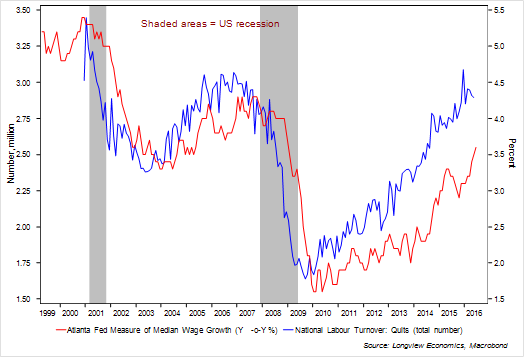

i. The tightening labour market, which should underpin rising wage growth in coming months/quarters. Multiple indicators illustrate that tightness: Job openings, for example, which essentially measures ‘demand’ for labour, have accelerated higher. With that, they have risen above the level of ‘new hires,’ suggesting that new job positions are opening more quickly than they are being filled. Historically, that has been indicative of labour market tightening and has coincided with accelerating wage growth. The ‘quit rate’ is trending higher (fig 1), as workers voluntarily leave their jobs (typically because they are confident in their ability to find a new job, and/or they see better opportunities elsewhere). It also suggests that firms are competing more actively for new hires and, as such, this data is highly correlated with wage growth. The ratio of ‘unemployed per job opening’ continues to fall and is now below the lows of the last economic cycle and at its lowest level since 2001. There are currently just 1.3 unemployed people per job opening (down from almost 7 in 2009). Small business compensation plans are at reasonably high levels and consistent with high/rising wage inflation.

Fig 1: Atlanta Fed wage growth (median, three months smoothed) vs. ‘Quits’ (number)

ii. Credit and money supply growth are high/accelerating. The credit cycle is the primary driver of US inflation. US bank credit growth accelerated higher in early 2014 and, for the past 18 months, has been stable at high levels. That has foreshadowed (and driven) the recent acceleration in US inflation rates. In prior Longview research, we examined the causal-link between credit and inflation. Consistent with stronger credit growth, money supply growth has also accelerated. Of particular note, though, money supply is rising rapidly relative to total US total capacity. As Greenspan highlighted this week: “It is the ratio of money supply divided by real GDP capacity to produce that ultimately determines the price level”. That ratio has accelerated higher in the past 18 months and is highly correlated with CPI inflation. Rapid credit growth, if it persists, should, therefore, continue to add to building domestic US inflationary pressure.

In conclusion, consensus expectations continue to favour a low inflation outcome in the US. Those expectations, both surveyed and market-based, are consistent with, and probably influenced by ‘goods inflation’ readings, which remain deflationary. Indeed, inflation readings of both ‘durable’ and ‘non-durable’ goods are negative. Critically, goods inflation is volatile, mean reverting and backward-looking. It’s also largely driven by oil & other globally traded commodity prices (and is, therefore, a global inflation rate). As such, it’s largely discounted by the Fed. Service sector inflation, which better reflects domestic inflationary pressure, is running at multi-year highs (2.85% in June) and is trending firmly higher. Two key factors point to a continued uptrend in Service sector inflation: They are i) the tightening labour market, and therefore growing wage and consumer price inflation pressures; and ii) the acceleration in credit and money supply growth, with ‘money creation’ through commercial banks as the primary driver of US inflation. The risks to the consensus view are therefore skewed to the upside, with the growing likelihood that the Fed is forced, at some stage, to begin once again talking up the prospect of rate hikes.

Article written by Harry Colvin and contributed by Longview Economics: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation advice; and Global thematic, macro and commodities research.

4 topics

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets