Watch out for exaggerated optimism in small caps

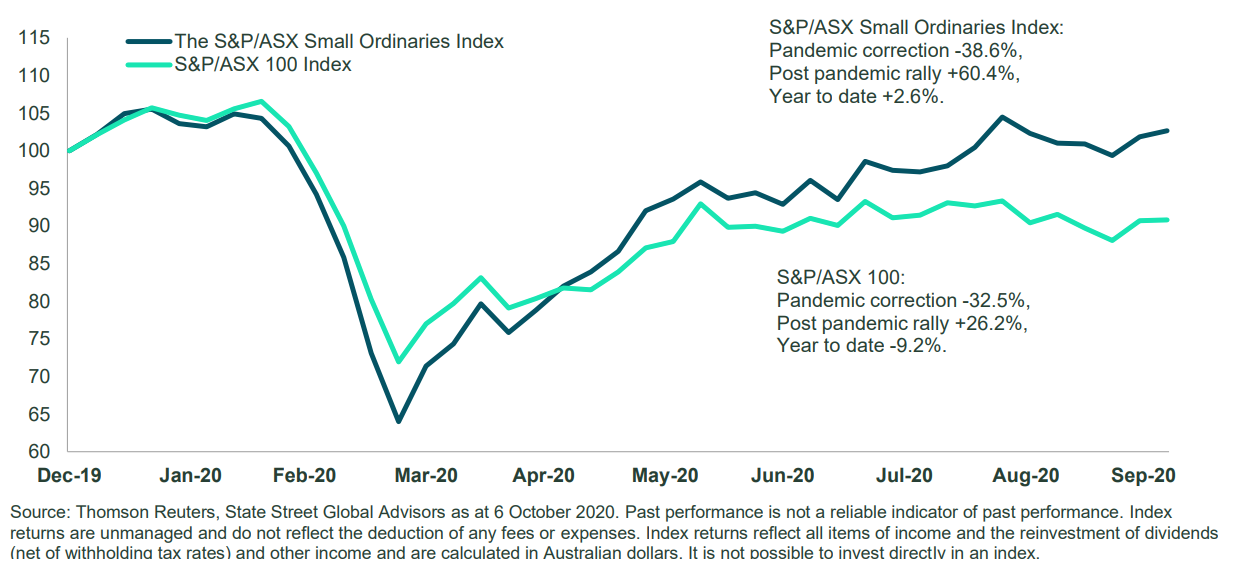

Small capitalised companies have been having a great run since the market bottomed in late March. The S&P/ASX Small Ordinaries Index is up 60% since the 24th of March 2020, but by contrast the larger capitalised companies as represented by the S&P/ASX 100 Index is only up 26.2%. The significant outperformance of the smaller companies has ignited renewed interest in this section of the market. In this monthly note we take a closer look at smaller companies.

Figure 1 - A wild ride in equities and even wilder ride in smaller companies

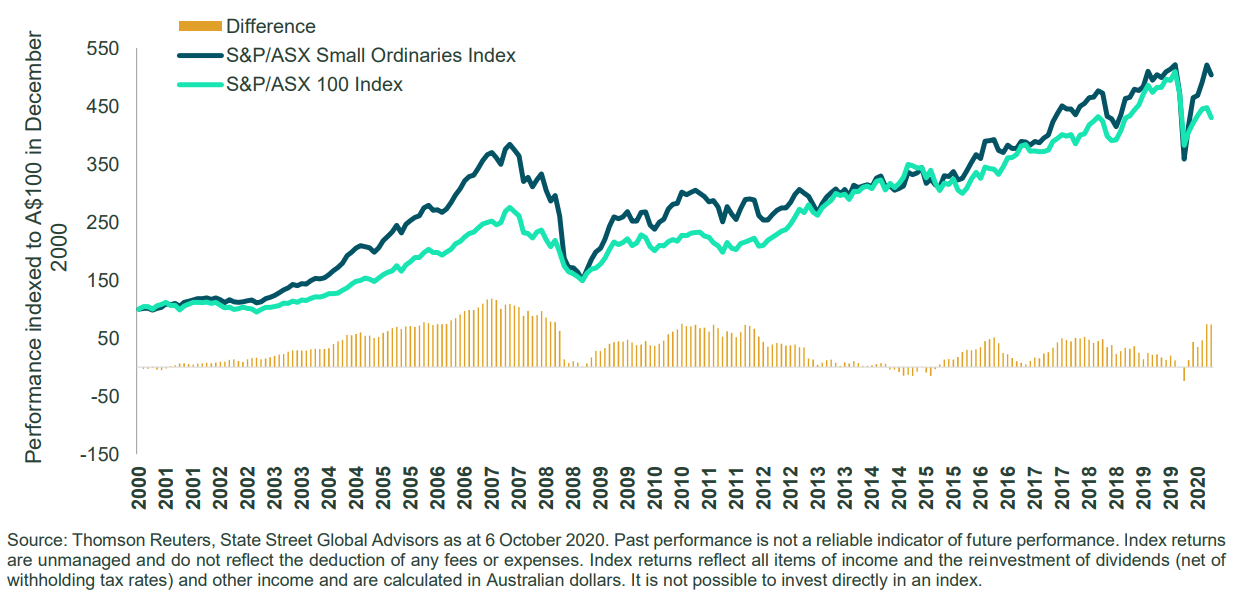

Greater returns but with more volatility

Over the last 20 years smaller companies have outperformed larger companies by almost 0.86% per annum but this outperformance has not been without risk. On average the volatility associated with small companies is 17% compared to larger companies with 13%. This is also evident in the beta of the small company index averaging 114%.

Figure 2 - Longer term return and risk characteristics from Australian Small and

Source: Thomson Reuters, State Street Global Advisors for the period 30 December 2000 to 30 September 2020. Past performance is not a reliable indicator of future performance.

Smaller companies have had a great run in the last 6 months but a quick look at the long term puts that outperformance into some context. Figure 3 illustrates the journey for the last 20 years. The smaller companies have had periods of significant outperformance which is historically followed by periods of underperformance. Depending on when you invest your experience could be quite varied.

Figure 3. Periods of outperformance have historically been followed by periods of underperformance

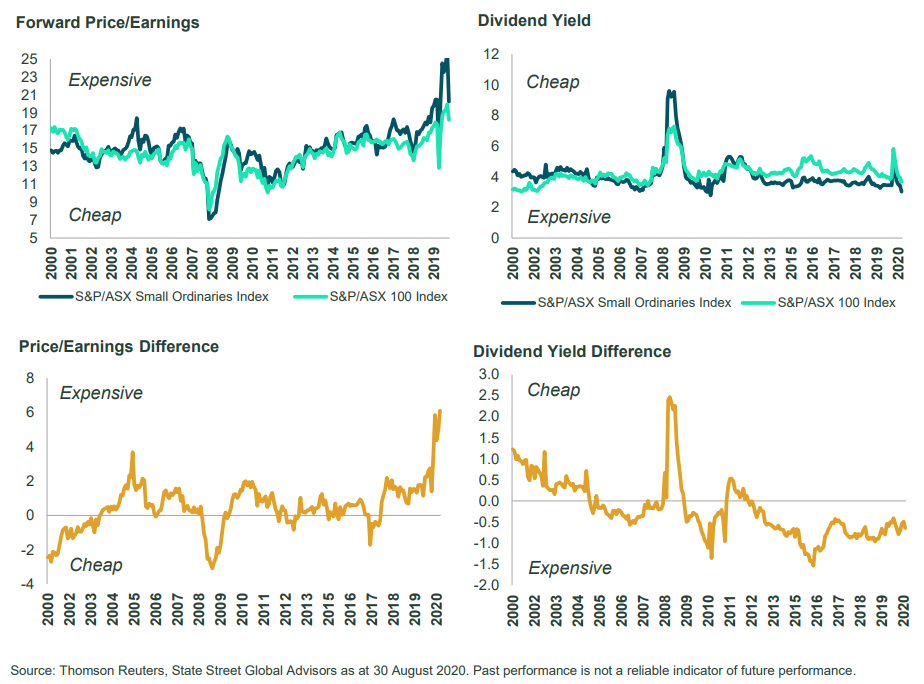

Valuations are rich in absolute and relative terms

On average over a longer period of time we find the smaller capitalised companies tend to trade at a slightly higher price to earnings multiple and generate slightly lower yields. But this tends to be quite volatile, as during risk on periods they can trade at much higher multiples whereas during risk off this can trade at below average multiples. Currently valuations are stretched for the market and are especially stretched to the smaller end of the index. Most of this has happened in the last 6 months as investors have been willing to price a strong recovery in earnings. It is entirely possible that the economy will recover and many company earnings will return to pre pandemic levels, but if they don’t then this section of the market is more at risk of disappointment. From a relative yield perspective the smaller companies are not as expensive as is implied by earnings multiples.

Figure 4: Smaller Company Valuations

Watch out for overly optimistic earnings especially from smaller companies.

One of the interesting observations about smaller companies compared to larger companies is the investment community is usually overly optimistic on earnings. In the last 20 years expected growth for the next 12 months has averaged +21.1% and yet on average this group of companies has only delivered +13.2%. By contrast the expected growth for larger companies is expected to be lower at only +9.4% and has only delivered +6.8%.2 A much smaller earnings disappointment compared to smaller companies. In both cases analysts’ expectations have been overly optimistic but in the case of smaller companies this optimism is exaggerated.

Never miss an insight

Stay up to date with our latest thoughts by clicking follow below and you'll be notified every time we post content on Livewire.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

........

Issued by State Street Global Advisors, Australia Services Limited (AFSL Number 274900, ABN 16 108 671 441) (“SSGA, ASL”). Registered office: Level 14, 420 George Street, Sydney, NSW 2000, Australia · Telephone: +612 9240-7600 · Web: www.ssga.com. State Street Global Advisors, Australia, Limited (AFSL Number 238276, ABN 42 003 914 225) (“SSGA Australia”) is the Investment Manager. Investors should read and consider the relevant Product Disclosure Statement (PDS) for a Fund carefully before making an investment decision. A copy of SSGA’s Managed Fund PDSs are available at www.ssga.com.au This general information has been prepared without taking into account your individual objectives, financial situation or needs and you should consider whether it is appropriate for you. You should seek professional advice and consider the product disclosure document, available at ssga.com, before deciding whether to acquire or continue to hold units in the Funds. The views expressed in this material are the views of the SSGA Australian Active Quantitative Equity Team through the period ended 8 April 2020 and are subject to change based on market and other conditions. The information provided does not constitute investment advice and it should not be relied on as such. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Volatility management techniques may result in periods of loss and underperformance, may limit the Fund's ability to participate in rising markets and may increase transaction costs. Actively managed funds do not seek to replicate the performance of a specified index The fund is actively managed and may underperform its benchmarks. An investment in the Fund is not appropriate for all investors and is not intended to be a complete investment program. Investing in the Fund involves risks, including the risk that investors may receive little or no return on the investment or that investors may lose part or even all of the investment. Standard & Poor’s and S&P are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”) and Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”) and have been licensed for use by S&P Dow Jones Indices LLC and sublicensed by SSGA. The S&P/ASX 300 Index is a product of S&P Dow Jones Indices LLC, and has been licensed by SSGA. SSGA’s Funds are not sponsored, endorsed, sold or promoted by S&P Dow Jones Indices LLC, Dow Jones, S&P, their respective affiliates, and none of S&P Dow Jones Indices LLC, Dow Jones, S&P, nor their respective affiliates make any representation regarding the advisability of investing in such product(s). Investing involves risk including the risk of loss of principal. Risk associated with equity investing includes stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. This material should not be considered a solicitation to apply for interests in the Funds and investors should obtain independent financial and other professional advice before making investment decisions. There is no representation or warranty as to the currency or accuracy of, nor liability for, decisions based on such information. The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA Australia’s express written consent.

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Global Advisors

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Global Advisors

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why "buy and manage" is the better way to invest in stocks

Livewire Markets