TOL - 29th Nov, 2024

Watch out for "sharp but brief price drop" in lithium, Macquarie

Lithium minerals markets have been dynamic over the past few weeks, with prices staging a modest rally. We check up on the key developments.

The ASX lithium trade has been both rewarding and debilitating at times over the last 2 years. Those who have endured the last bull and bear cycle have likely experienced both sides of the emotional investing rollercoaster.

Many are playing the long game however, choosing to look through the recent valley in lithium minerals prices. It’s pretty simple, they argue. The energy transition has begun, and lithium is going to play a major role in the decarbonisation of the planet. These investors believe it’s just a matter of time until lithium demand again dwarfs its supply.

In a recent article, I noted from a technical perspective, it appeared that at least a short term bottom in lithium prices appears to be in. Since then, the S&P Platts Global spodumene 6% price has increased by over 5% to US$815/t, up nearly 14% from its October low, and benchmark January lithium carbonate futures have also rallied over 5% to RMB80,350/t, up nearly 13% from its respective low.

My “bottom is in” call is so far holding, and remains intact until new lows are printed (then the technicals revert to following the prevailing long term downtrend – it’s the dark pink zone in the chart above).

A new research report from major broker Macquarie sheds further light on the current demand-supply dynamics in the lithium market, as well as several major ASX-listed lithium stocks. Let’s review the key points from the report.

Latest lithium market demand-side factors

In the report, titled “Critical Minerals Chronicle: Lithium producers musical chairs”, Macquarie also notes that lithium’s downward price trend has “moderated” since August. The key demand-side factor contributing to the stabilisation of the downtrend has been seasonal restocking of lithium chemical inventories, particularly in October and November, ahead of the usual shutdown in processing and battery production over the Lunar New Year holiday in late-January-early-February.

The big risk, notes Macquarie, is when this restocking tapers off, lithium minerals are at risk of suffering “a sharp but brief price drop”. Timing? Macquarie warns restocking will begin to taper in December, and January could be a major risk month for lithium minerals prices.

China remains the primary driver of lithium demand due to robust growth in plug-in vehicle sales, bolstered by subsidies and new model launches. Macquarie notes that year-to-date, China's plug-in sales have grown by 40% year-over-year, with an average market penetration of 46.7%. However, this strength contrasts with weaker EV sales in the U.S. and Europe, tempering global demand growth.

Latest lithium market supply-side factors

Macquarie identifies three major factors influencing the supply side of the lithium minerals price equation now and likely in the medium term.

Factor 1: Production curtailments and supply adjustments

Negative supply-side responses have intensified during 2024 as subdued lithium prices have ramped up the pressures on high-cost producers. According to Macquarie, key developments include:

Liontown Resources (ASX: LTR): Reduced its mining rate by 7% to 2.8 mtpa at its maiden 2H FY25 production guidance release.

Mineral Resources (ASX: MIN): Suspended its Bald Hill operation (~16ktpa lithium carbonate equivalent (“LCE”)) and one train at Mt Marion (~12ktpa LCE). The company also delayed the Wodgina three-train strategy.

Pilbara Minerals (ASX: PLS): Cut production by suspending operations at the Ngungaju plant (~12ktpa LCE).

Lepidolite operations in China: CATL’s Jianxiawo mine, with a nameplate capacity of ~90ktpa LCE, has reduced production by approximately 40ktpa LCE due to high costs.

These curtailments have partially alleviated market oversupply, notes Macquarie, who now forecasts a surplus of 62kt LCE in CY24 and 120kt LCE in CY25.

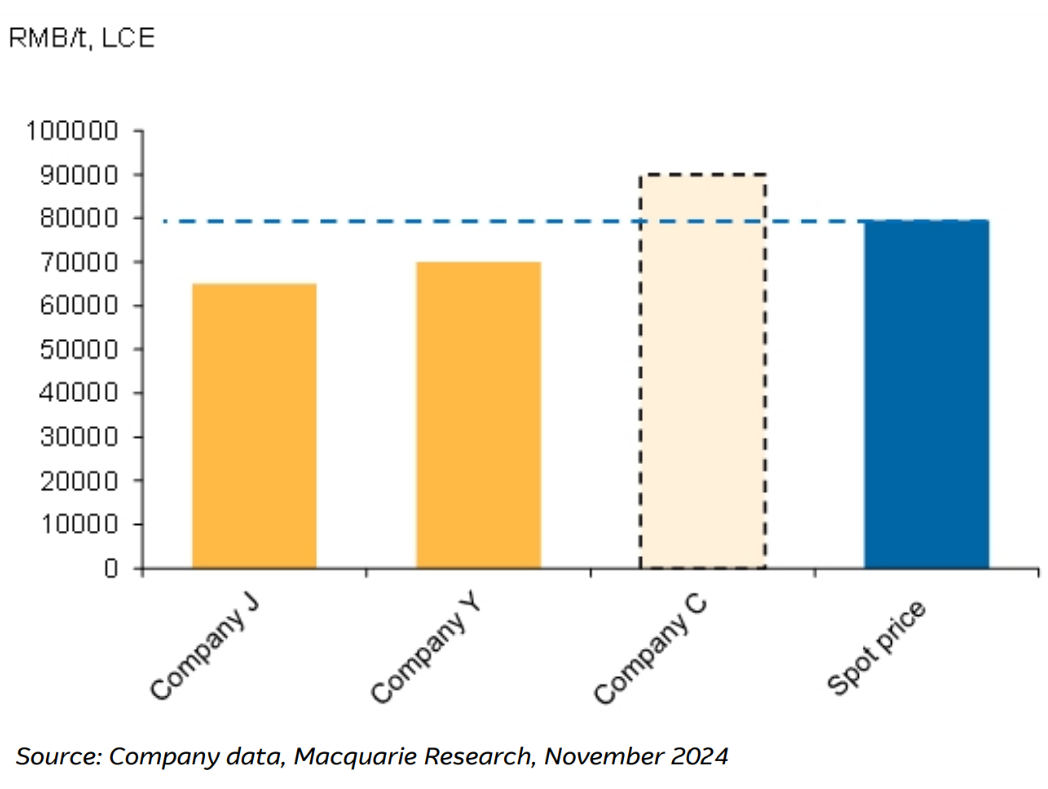

Figure 8 - AISC estimate for major Lepidolite supplies. Source: Company data, Macquarie Research, November 2024. From “Critical Minerals Chronicle: Lithium producers musical chairs”, Macquarie Research, 25 November 2024. (click here for full size image)

Factor 2: Financial pressures on smaller producers

Macquarie observes that smaller producers and developers are facing increased cash flow challenges, leading to business mergers and production halts. Notable examples include the recent merger between Sayona Mining (ASX: SYA) and Piedmont Lithium (ASX: PLL), as well as Arcadium Lithium’s (ASX: LTM) decision to suspend waste stripping at Mt Cattlin and move operations to care and maintenance by mid-CY25.

These actions reflect a broader trend of consolidation and financial strain among less competitive players.

Factor 3: African and low-grade producers face challenges

Macquarie notes that African producers have reduced petalite shipments to downstream refineries due to negative margins, while low-grade lepidolite suppliers in China have also cut uneconomic output.

Macquarie warns that whilst these adjustments have helped to stabilise lithium minerals prices more recently, they are unlikely to be sufficient to completely eliminate further downside risk.

Lithium price forecasts

Putting the above demand-side and supply-side factors together, Macquarie concludes lithium minerals prices are likely to remain range-bound in the near term, with support around RMB70,000/t and resistance at RMB90,000/t for lithium carbonate. The current price for lithium carbonate is approximately RMB80,000/t.

Above RMB90,000/t, suggests the broker, the market could again be awash with supply as suspended production capacities return. Just a reminder here also of the potential for a “sharp but brief price drop” in December and January as restocking activities ease in line with seasonal patterns.

ASX-listed lithium stocks updates

Macquarie provides updates on several lithium stocks within its coverage. Here are the main points from each update, as well as the broker’s current rating and target price for each stock:

IGO Limited (ASX: IGO)

Rating: NEUTRAL | Target Price: $5.60

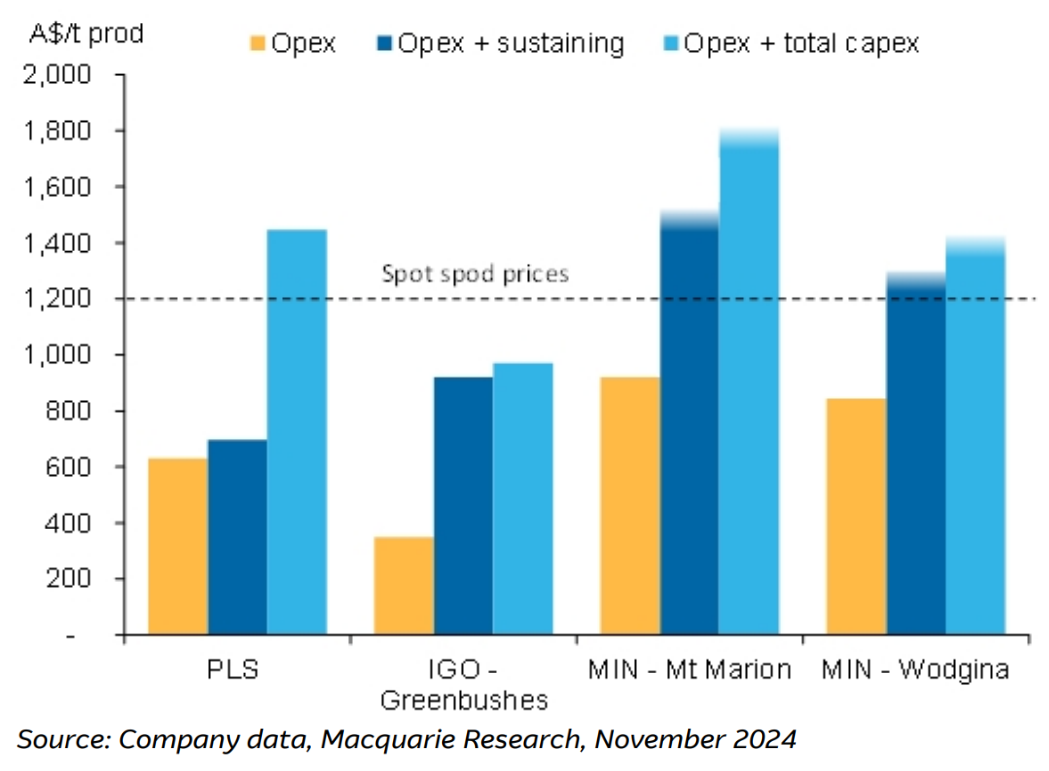

Competitive position: Greenbushes mine remains the lowest-cost lithium producer, excelling in metrics that include sustaining and total capex.

Risks: Expansion plans at Greenbushes and Kwinana Hydroxide, along with potential developments at Cosmos and Mt Goode, underpin IGO’s valuation. Variances in outcomes at these projects present the greatest risks. Volatility in spodumene and nickel prices also pose risks to earnings.

Mineral Resources (ASX: MIN)

Rating: NEUTRAL | Target Price: $35

Competitive position: Cash costs for Mt Marion and Wodgina are above current spodumene prices, though recent cost-reduction measures may improve financial performance. The delayed Wodgina three-train strategy adds uncertainty.

Risks: Variability in iron ore prices and spodumene prices also pose risks to earnings.

Pilbara Minerals (ASX: PLS)

Rating & Target Price: N/a

Competitive position: The suspension of Ngungaju (~12ktpa LCE) has impacted output. However, PLS maintains the second-lowest cash costs after Greenbushes, supported by its organic growth initiatives (P680 and P1000).

Risks: While sustaining capex remains manageable, the company faces challenges in scaling new projects.

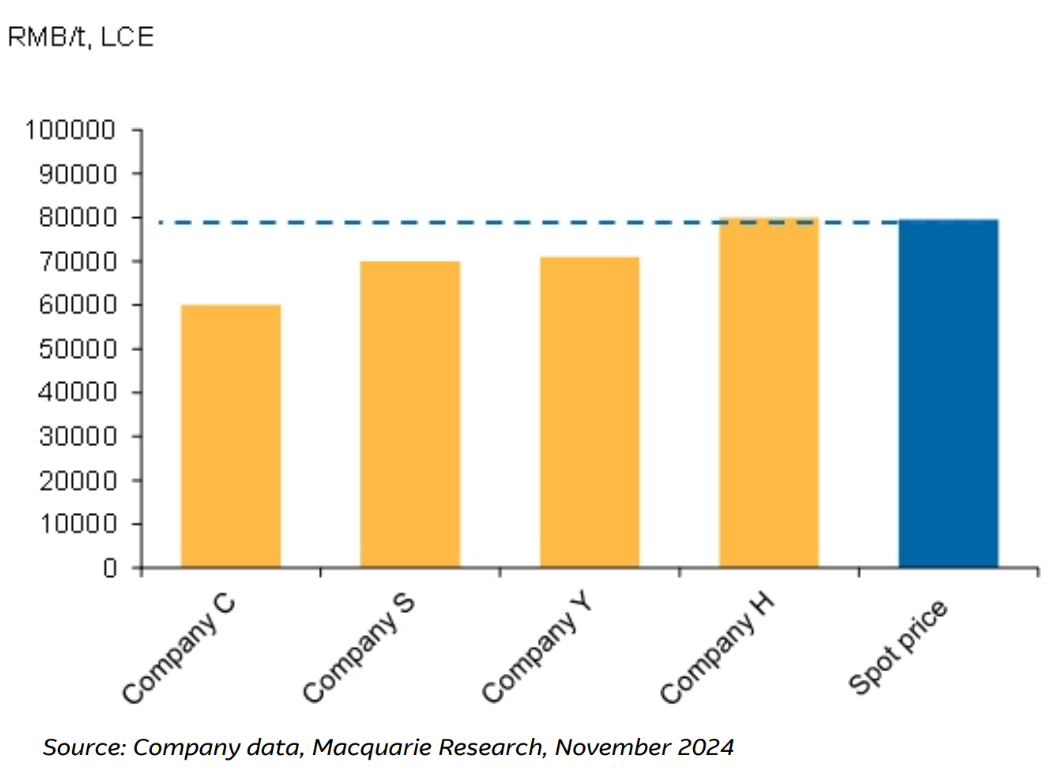

Figure 6 - Cash unit costs estimate – FY25. Source: Company data, Macquarie Research, November 2024. From “Critical Minerals Chronicle: Lithium producers musical chairs”, Macquarie Research, 25 November 2024. (click here for full size image)

Liontown Resources (ASX: LTR)

Rating: UNDERPERFORM | Target Price: $0.60

Competitive position: Underground development at Kathleen Valley contributes to higher costs, with operating costs estimated at A$1,170-1,290/t and total costs (operating expenditure plus total capital expenditure) potentially reaching A$1,430-1,550/t under certain assumptions. Growth capex of A$42-50m adds to potential financial strain.

Risks: Geotechnical challenges and ramp-up uncertainties for both open-pit and underground mining increase the risk profile.

Sayona Mining (ASX: SYA) and Piedmont Lithium (ASX: PLL)

Rating: NEUTRAL and NEUTRAL | Target Price: $0.04 and $0.21

Competitive position: The 50/50 all-stock merger removes price caps and offtake agreements, enhancing the value of the North American Lithium (NAL) project and paving the way for brownfield expansion.

Risks: Variances in the spodumene price, as well as in capital and operating costs.

Core Lithium (ASX: CXO)

Rating: UNDERPERFORM | Target Price: $0.09

Risks: Variances in the spodumene price, as well as AUD/USD volatility.

Global Lithium Resources (ASX: GL1)

Rating: UNDERPERFORM | Target Price: $0.21

Risks: Boardroom uncertainty, variances in the spodumene price, as well as AUD/USD volatility.

Patriot Battery Metals (ASX: PMT)

Rating: OUTPERFORM | Target Price: $0.70

Risks: The lack of a maiden resource for the Corvette project introduces significant risk to assumptions around scale, capital costs, and operating costs.

Galan Lithium (ASX: GLN)

Rating: NEUTRAL | Target Price: $0.14

Risks: Variances in the lithium carbonate price, as well as AUD/USD volatility.

Atlantic Lithium (ASX: A11)

Rating: NEUTRAL | Target Price: $0.30

Risks: Variances in the spodumene price, Ewoyaa development project mining inventory assumptions.

Conclusions

It appears from Macquarie’s latest research, that the lithium market is at a pivotal juncture. In the bigger picture, demand is being driven by China’s growing but dynamic (greater mix of lower-lithium intensive hybrid vehicles) EV growth, but in the short term is more beholden to seasonal variations.

On the supply side, Macquarie noted that production curtailments and financial pressures on high-cost producers have introduced volatility, while mergers and cost-control measures seek to rationalise the operations of several major global players.

On ASX-listed lithium miners, Macquarie points out a broad spectrum of cost competitiveness and strategic positioning, presenting investors with both opportunities and risks. Those risks are closely tied to pricing dynamics, project execution, and general market and industry confidence.

Translation: There is no clear path at least in the short term back to the strong lithium minerals price gains enjoyed by investors in 2021 and 2022. Opportunities will present themselves, but investors will need to be on their toes in 2025!

This article first appeared on Market Index on Tuesday 26 November 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

5 topics

11 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment