What Benjamin Graham would say about this market

"In the short-run, the market is a voting machine - reflecting a voter-registration test that requires only money, not intelligence or emotional stability - but in the long-run, the market is a weighing machine."

The quote was attributed to Ben Graham by Warren Buffett in the 1993 Berkshire Hathaway letter to shareholders.

Ben Graham would be familiar to most Livewire readers as the father of value investing and he played a seminal role in developing the profession of equity analysis. Graham developed a framework to analyse companies, very different from the speculation and market manipulation that prevailed in stock markets the first quarter of the 20th Century, famously described by Edwin Lefevre in his 1923 book Reminiscences of a Stock Operator.

In 1923 Graham set up his own firm and soon afterwards began teaching investment classes at Columbia University in New York. The content of these classes was initially incorporated into the heavyweight Security Analysis from 1934 and then the more accessible The Intelligent Investor in 1949.

Famously in 1950, a young Warren Buffett enrolled at Columbia to study under Graham and later work for him at his investment partnership Graham-Newman. At the heart of Graham’s investment philosophy was selecting securities that were currently priced at a discount to their intrinsic value.

What Benjamin Graham would say about today's market

I see that the above lesson from Ben Graham is very useful in making sense of the market noise that investors face on a daily basis and the oscillations in market sentiment that drive share prices.

On a daily basis, no investor sets the share prices of the companies in their portfolio and good quality companies will get sold down along with shaky companies in market corrections.

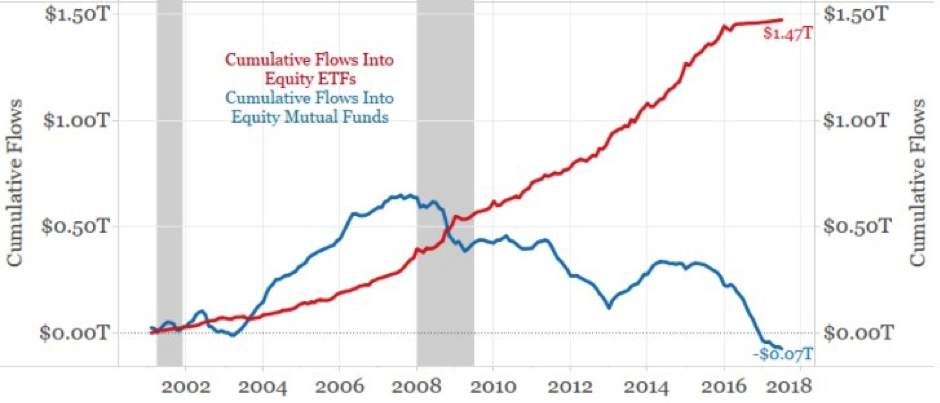

Over the last ten years, we have seen a large significant amount of money flowing into equity index funds globally, which we see has reinforced the view that the market is, even more, a voting machine in the short-term than it was in the past.

When funds flow into index funds, the managers mechanically buy equities based on their index weight, pushing well-loved stocks higher.

Conversely when index funds see large redemptions such as was the case in October 2018; all stocks in an index such as the ASX 200 are sold down in proportion regardless of an individual firm’s profit outlook.

Macquarie is a prime example

For example, one of the worst performing major stocks on the ASX in October was Macquarie Bank, whose share price fell -7% despite the bank offering a good prospect of reporting a solid profit result and higher dividends in the first week of November.

Macquarie Bank’s share has begun to recover after upgrading their earnings outlook for 2019 twice this month!

So, what investors can control is owning companies with solid fundamentals with earnings and dividends that are growing ahead of inflation.

Over time, the market will "weigh” the rising earnings and dividends which will be reflected in a rising share price.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in both Australian Equities and Listed Property and Infrastructure. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

1 topic

1 stock mentioned

Atlas is a boutique investment manager focused on income-related strategies in both Australian Equities and Listed Property and Infrastructure. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in both Australian Equities and Listed Property and Infrastructure. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available...

Expertise

Comments

Comments

Sign In or Join Free to comment