What to do about franking credits

In March this year Bill Shorten pledged that should Labor win the upcoming election they will axe cash refunds for excess imputation credits paid to individuals and in superannuation funds. This would reverse the cash refund of imputation credits introduced by John Howard two decades ago. It would also be introduced with no grandfathering or transition arrangements. Malcolm Turnbull rejected it as a “cash grab”. The removal of Malcolm Turnbull means the Liberals can renege on that position and even adopt the changes should they feel it politically expedient.

The measure was introduced by Bill Shorten to win votes from the “poor majority” by stopping the super wealthy, who were in a tax-free environment, getting tax refunds. In introducing the proposals, Bill Shorten used an example of an extreme franking credit refund of $2.5m to a single SMSF in the 2014-15 financial year. But in the end, it is the 610,000 people with less than $1.6 million in their super fund that will be hurt the most. The super wealthy (those with significantly more than $1.6 million in super assets), since the introduction of the $1.6 million transfer balance cap on super pay 15% tax on investment earnings and capital gains (if the asset was held less than 12 months or 10% if held more than 12 months) and as such will be able to utilise the benefit of franking credits to offset that tax.

In many cases, for the super wealthy, the introduction of the $1.6 million transfer balance cap and the removal of cash refunds of franking credits ends up being a nil sum game - no refund, but no tax payable, because the 30% company credits are offset by the 15% super tax. In other words, the franking credits negate tax on earnings above the $1.6 million. The wealthy still get the use of the imputation credits whereas those with less than $1.6 million in super, on the other hand, simply lose the tax refunds altogether.

The Liberal government suggested in March that 97% of people who get the franking credit refunds already (1.17m people) have a taxable income below $87,000 and more than half of them have taxable income below the tax-free threshold. Lobby groups say that it would cut $5000 worth of income from the median do-it-yourself super fund retiree earning about $50,000 a year.

But the real indignation comes from the idea that the companies have already paid tax on their dividends and that the government is simply intercepting other people’s money.

The issue has obviously come back into the spotlight because the Liberals have momentarily/permanently imploded making a Labor government at this point look more likely than it was and more likely than a Liberal government. Sportsbet (not that the betting agencies have been any good at predicting elections) have Labor paying $1.25 for an election when compared to the Coalition at $3.50.

What can you do about it

We have had some client contacts asking what they should do about the potential loss of cash refunds of imputation credits. Here are a few points on that but the first is don’t get emotional - it will not help. The emotion over this issue is unprecedented. So much as mention the removal of cash refunds in polite company and prepare yourself for an hour’s worth of indignant lecturing about how unfair it is. Someone has to lobby, someone has to make an effort, and there are a variety of ways for you to support that effort. I am more concerned in this article to address the question, assuming a government gets in that removes cash refunds of imputation credits, what does it mean and what do I do about it.

Here are a few points:

- It may never happen. Labor may not win the next election.

- Even if Labor does win the next election, they may have to water down the somewhat unforgiving stance they have taken so far. They can afford to play tough right up until they lose the votes of 660,000 SMSF superannuants. If they need them, this policy will be reviewed and may even be forgotten. Forgiving it might even win them votes they weren't going to get, such will be the relief.

- Even if Labor does win the next election and pushes ahead with an uncompromised policy on this issue, they still have to get it legislated. If there is a hung parliament, even if there isn’t, they may still struggle to achieve it.

- Even if Labor does win the next election and get the changes legislated the current intention is that it would only be introduced from June 2020 onwards. In which case you still have this tax year and the next tax year to collect franking credits and have them refunded (depending on whether Labor changes the timetable). That 22-month window of opportunity may lend even more emphasis to being in stocks with fully franked yields this year while you can still utilise the imputation credits. Companies will also have this small window of opportunity to empty any bloated franking accounts through share buybacks with a large dividend component and through special dividends with franking attached. It may just be the case that the 22 months before June 2020 end up being a super bumper year of franking giveaways by corporate Australia. So don’t jump out of the big fully franked high yield stocks yet.

- Don’t get too concerned about the “whole market” turning its back on the high yielding fully franked stocks like the banks and Telstra. The section of the population that won’t be able to utilise franking credits and may desert such stocks is the minority in a zero-tax environment with less than $1.6 million in superannuation. The international institutions that hold up to 40% of many stocks will not be affected at all. They never got the franking anyway - they won't be selling anything because of the change. It is not positive for the stocks involved, but it is not universal, and the adjustment will not be made until the legislation passes and even then, probably not until it comes into effect. In other words, the bank sector will not be dominated by this issue, there are plenty of other sentimental and fundamental issues that will overwhelm this one.

- Predictable recommendations - For those that do get caught by this change, if you get caught, then the obvious advice from my industry will be to look to replace the lost income with some other return. This will manifest itself in a few recommendations, but all of them are effectively saying the same thing, how do you get a higher return without franking. Some of the recommendations will focus on yield, buying the lowest risk stocks with the highest yields to replace the lost franking. Hence the predictable recommendations to buy hybrids or REITs or bonds (Note: hybrids still include franking and will only yield around 4.5% without it, REITs offer a range of yields many of which aren’t franked and are lower than an unfranked bank, and bonds yield next to nothing). Other recommendations will tell you that you have to take more risk for a higher return (and they are right) and in so doing the focus shifts from yield to a higher total return (capital plus income), which, oddly enough should be your constant pursuit, not a new pursuit. Those recommendations will also very likely suggest that you desert Australia and invest in global equities, at least that’s what the global equity fund marketing departments will tell you, this is their opportunity to snag your interest. Other recommendations, self-interested recommendations, will tell you that now is the time to buy ETFs, which do not rely on franking as their major benefit, they rely on boring returns with very little risk relative to stocks. In the end, there is no one answer, and you will have to choose between a low-risk yield or a higher risk investment with a focus shift from income to capital. This will involve a focus on share price growth rather than income and franking, and that will scare many retiree investors who pay little attention to share prices.

- Property – Some investors might decide to abandon equities and to look at property. They are very different investments. You don’t have to mend the toilet at BHP or worry about whether your tenant is going to burn the place down. You can sell shares on the click of a mouse; property is illiquid. Your choice. Both asset classes require skill and experience, and my guess is that an equity investor will struggle badly with the engagement and commitment needed for property investment. They are not the same.

- The franking shock might be a good thing - if this legislation snaps some investors out of their zombielike pursuit of franking credits it might be the best thing that ever happened to some investors. Buying high yielding stocks by definition means buying mature companies with limited growth opportunities who can find nothing better to do with their money than return it to shareholders. In general, these stocks are by their nature, dull under-performing stocks. As such, in pursuit of franking credits, many investors have committed themselves to a lower total return because the share prices of mature stocks don’t grow as much as stocks that are in growth industries and don’t pay high dividends but reinvest returns. This franking “shock” might just shock some investors out of this rather mediocre game of buying low growth stocks with high yields which have for years distracted them from the growth available in the stock market generally. Ask any American and they will tell you that bonds are for income and equities are for growth. This is why so many American companies continue to pay no dividends despite sitting on mountains of cash because they know their job is to achieve a high return on equity and use their profits to fund that growth. American companies know the folly of chasing income, because it is in the US investment culture, to grow earnings not to return capital to shareholders so that they can earn 2.8% in bonds. It has always rather amazed me, the Australian appetite for income stocks, and it is because of franking, and the companies have pandered to that demand. That’s why the Australian market yields 4 ½% against the US market on just over 2%. Because we have a population of investors seduced by a tax fiddle rather than the main game of trying to make money out of capital gains.

- The 45-day rule becomes redundant for some - For those of you in a tax-free environment that have had to concern themselves with the 45-day rule, if you’re not going to get the franking, you can now forget it. Buy and sell stocks and strip the dividends at will over any timeframe.

- Moving money out of super - There are some suggestions that you move money from super into your personal name to take account of your personal tax-free threshold and pensioner tax offsets. Be bloody careful before you do that. Individuals investing in their own name are also impacted by the loss of franking credits (unless you are a Centrelink pension recipient). It may create a CGT event, there are selling costs, it might affect Centrelink payments and you may not be able to put the money back into super if you wanted to.

- Watch out for predators with fancy new products - Beware predators creating products tailored to your insecurity and anger and marketed as a solution to the loss of franking credits. There is nothing for nothing in this world, but this issue has created a demand for some sort of franking credit replacement. Someone will come up with a product to fill the gap, and while they market something that may appear to meet that want or need, as always with these things, like the fads in ETF’s, there is always a price to pay tomorrow for the benefit today. This is a huge marketing opportunity for product creation. Beware someone promising a franking substitute, they have their other hand in your back pocket.

- Some margin loans will no longer fund themselves - For people using franking credits to pay the interest on a margin loan, as many margin loans have marketed themselves, margin loans will become less popular.

- If it’s gone it’s gone - don’t blow the nest egg trying to get it back - The main point to take on board is that if the franking goes, it’s gone, and if you need to replace it you will need to take more risk, which includes a focus on share prices and timing stocks, or accept the loss and keep a low-risk profile in something that has a reasonable yield. Those investments might still include the banks, Telstra, utilities, even if you can’t get the franking back. Better you accept a lower standard of living than you blow your capital trying to get back what has been taken away.

Some unfranked yields

Not that it has any relevance at this very premature moment in time, but I have been asked for a list of high yielding investments that don't include franking. Here are some higher-yielding stocks and hybrids.

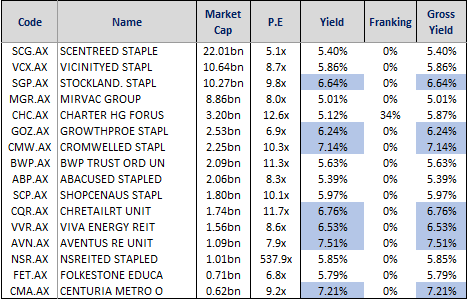

If you want low(er) risk here are the REITs - these are REITs with a market cap over $500m:

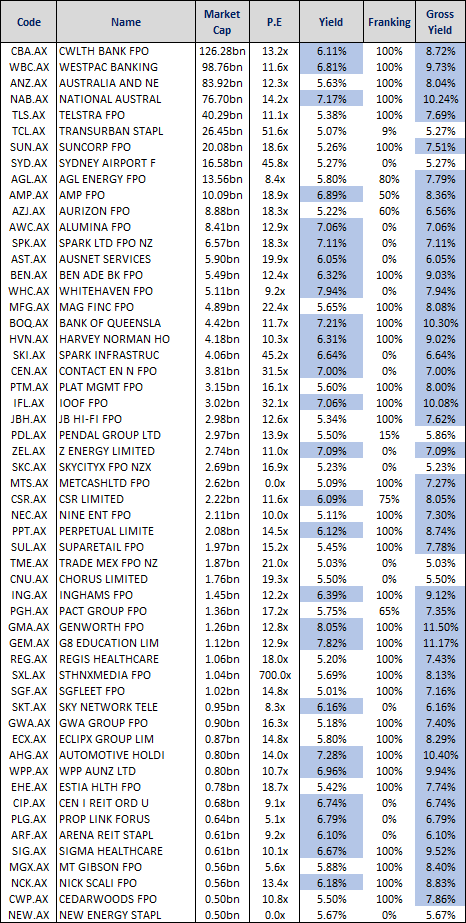

Here are stocks with yields over 5.0% before franking with a market capitalisation over $500m. I have excluded a few for quality reasons:

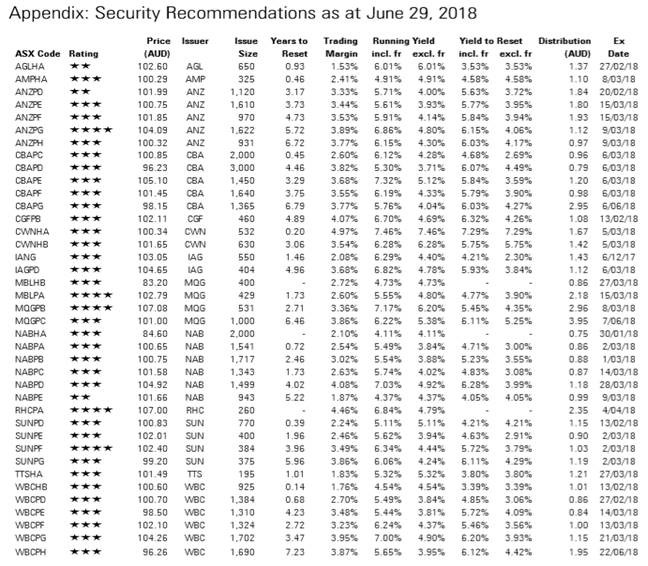

Here is a list of Hybrids showing the yields and the franking - this is from Morningstar:

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and informing private investors with insightful, honest, straight-up independent stock market research and ideas. Marcus likes to call it as it is without agenda, puts subscribers first, and this has paid off for real people with real money.

2 topics

1 stock mentioned

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Comments

Comments

Sign In or Join Free to comment