What we learned from Wirecard – does your ethical ETF pass the pub test?

In late June, German payments giant Wirecard filed for insolvency, owing creditors almost $5.8 billion. The company’s collapse came a week after its auditor, Ernst and Young, found a massive $3.1 billion hole in its books. EY refused to sign off on the company’s 2019 accounts, saying there were indications of an “elaborate and sophisticated fraud involving multiple parties around the world”.

Markus Braun, the firm’s CEO, resigned, and was subsequently arrested on suspicion of misrepresenting the firm’s finances.

Wirecard’s implosion is a stunning fall from grace for a company that was once seen as a champion of the European technology industry.

So how is the demise of a German fintech company relevant to Australian investors in global ethical ETFs?

While it’s likely that relatively few Australian investors will have had direct exposure to Wirecard, it’s possible that significantly more had exposure via a managed fund or ETF.

The holders of broad sharemarket funds may be relatively sanguine about an event such as this, accepting that broad sharemarket exposure inevitably involves ‘taking the bad with the good’.

However, for one rapidly-growing class of investors, investing their money in businesses whose environmental, social and governance (ESG) standards are beyond reproach is non-negotiable. For ethical investors, a true-to-label exposure is one of the most important factors to be considered in their investment choices.

What do we know about Wirecard?

Wirecard offers products and services in the areas of mobile payments, e-commerce, digitisation and finance technology. And in particular, it is one of the popular options consumers can use to gamble online. Once an account is set up with Wirecard, it can be loaded with funds from a credit or debit card, or from a bank account. Account holders can use Wirecard to move money to and from online casinos, without having to disclose their banking information.

In a report by the Financial Times[1], Wirecard acknowledged that up to 10% of its payment volumes “relate to lottery, gambling, dating, adult entertainment and associated business models”.

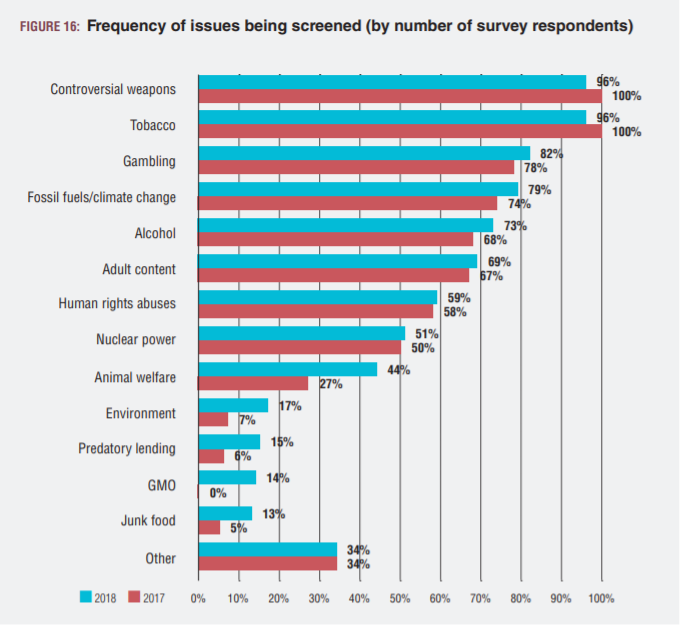

In its Responsible Investment Benchmark Report 2019, the Responsible Investment Association Australasia (RIAA) found that 82% of the responsible investment managers surveyed said they screened investments for gambling (see figure below).

Source: Responsible Investment Benchmark Report 2019, RIAA

How did ethical ETFs perform in practice?

Wirecard was excluded from a number of ASX-traded ethical ETFs, including the largest equities-focused global ethical ETF, the BetaShares Global Sustainability Leaders ETF (ASX: ETHI).

ETHI applies limits to the percentage of a company’s revenue that can be derived from activities deemed inconsistent with responsible investment considerations. These exposure limit guidelines include a limit of 0% for casinos and manufacture of gaming products, and 5% for distribution of gambling products.

Due to its involvement in gambling, Wirecard did not pass ETHI’s screening process. It was estimated that well over 5% of the company’s revenue was derived from providing payment services to online gambling, poker tournaments, and sports betting platforms.

Negative screens also resulted in Wirecard’s exclusion from most other ASX-traded ethical ETFs – but not all.

Not all ethical exposure are created equal

For investors who are concerned about the true-to-label exposure of their ethical investments, it’s essential to have confidence that an ethical fund is screening out investments that do not align with their values.

In evaluating whether an ethical ETF is true-to-label, investors need to assess the integrity and quality of the investment methodology the fund employs, in particular how stringent the fund’s screening processes are. The rigour of screening processes can vary between ethical ETFs.

Many ethical investors also believe it is important to have an element of human oversight, to provide an extra filter that decreases the chance that an investment of dubious ethical quality will ‘slip through the cracks’. Some ethical ETFs rely on off-the-shelf indices without this element of additional oversight.

This can frequently result in peculiar stock inclusions that may not pass the ethical ‘pub test’, and would be out of place for most investors seeking an ethical exposure.

For example, the French beauty giant L’Oreal is a constituent in a number of ethical ETFs trading on the ASX, but has been screened out of others, including ETHI, based upon its record on animal welfare. The company conducts animal testing for cosmetic purposes and has received a “Fail” grade from the influential Ethical Consumer Guide.

In the last two years, other stocks screened out of some ethical ETFs but included in the portfolios of others traded on the ASX have included Halliburton, Schlumberger, Barrick Gold, Valero, Kering, and others that ethical investors may not be comfortable with, for reasons including environmental degradation, fossil fuel exposure, animal cruelty, junk food, bribery, fraud, tax evasion and breaking trade sanctions.

Summary

The Wirecard episode demonstrates the importance of understanding what lies ‘under the hood’ of an ethical ETF. There are significant differences between fund methodologies, and as a consequence, in the ability of different funds to deliver on their promise of offering ethically-screened portfolios that align with the values of ethical investors.

When considering investing in an ethical ETF it’s important to read the PDS and other resources on the fund issuer’s website to understand how the fund’s screens work, and other elements of its methodology.

[1] https://www.ft.com/content/cd12395e-4fb7-11e9-b401-8d9ef1626294

Learn more

ETFs are one of the fastest growing investment vehicles in the Australian market. For a full range of products available to investors, please visit BetaShares website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Betashares is a leading Australian fund manager serving over one million investors across Australia’s broadest range of ETFs. Betashares’ range of intelligent investment solutions covers almost every asset class and investment strategy.

4 topics

Betashares is a leading Australian fund manager serving over one million investors across Australia’s broadest range of ETFs. Betashares’ range of intelligent investment solutions covers almost every asset class and investment strategy.

Betashares is a leading Australian fund manager serving over one million investors across Australia’s broadest range of ETFs. Betashares’ range of intelligent investment solutions covers almost every asset class and investment strategy.

Comments

Comments

Sign In or Join Free to comment