Who is the best investor?

You know when you ask a friend for advice and the primary theme of their advice is “keep it simple”?

It’s a very comforting phrase.

I think we (humans), as a fearing animal honed to survival, love hearing those three simple words “keep it simple”. It immediately reduces our anxiety around the path in front of us, particularly the unknown part of that path. No matter your acumen, experience, tools or knowledge, there’s not one person on the planet that isn’t convinced that as part of the unknown path they will be able to tackle the ‘keep it simple’ part.

Unfortunately, despite what ol’ Warren Buffet recommends the ‘man or woman on the street’ do regarding their investment strategy (which is basically just put it all in equities and don’t try and find someone like him to invest on your behalf), history suggests that simplicity will not get you the best investment outcome for your hard-saved dollars over the long term.

A complex combination of strategies utilised by the world’s best investors sees them get the best returns for their funds.

These ‘privileged’ investors utilise/can get access to sub-strategies including 'special situations', private equity (directly and in funds), leverage, factor tilts, and the best, most proven and exclusive investment managers on the planet.

Buffet’s Berkshire Hathaway is a good example. Warren’s recommendation to the ‘man or woman on the street’ is to invest in 90% equities (US in his example) and 10% in short term government bonds. Over the 40 years between 1973 to 2013 this would have made you a tidy sum of 9.8% per annum. If you’d instead invested in Berkshire Hathaway stock over a similar, but even longer period (1965-2017) you’d have received a 20.9% compound annual return (and if you assess your return as the CAGR of Berkshire’s book value, it’s slightly less at 19.1%). But how many average investors can bail out the wizards of Wall Street, Goldman Sachs, with a bunch of custom warrants at the height of the GFC? That’s a classic example of a ‘special situation’.

While it would take you more than a lifetime to review every investment strategy possible or on offer, much of this reviewing and distillation has been done by the global investment community over many decades; allowing us to find ‘the best’.

It’s impossible for a self-directing or advised investors to replicate the portfolios of the world’s best investors (Ray Dalio, Warren Buffet, The Ivy League Endowments, etc). However, the ‘average investor’ can allocate under a 'keep it simple' strategy and utilise the foundations of the world’s best to give themselves a good chance of generating the optimal returns. This is done by breaking down the broad asset allocations of many of the world’s best and allocating their portfolio on this basis, positioning oneself to enjoy the majority of the bests’ returns (or perhaps even more).

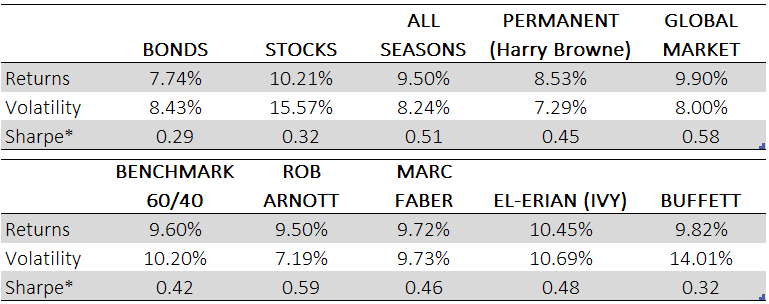

So, when we look at this deconstructing/reconstructing strategy, the strategy that comes out on top (in terms of the combination of returns, volatility and Sharpe ratios) is the strategy loosely known as the Ivy League Endowment strategy (pioneered and followed by endowment funds such as Harvard and Yale). Fortunately, or unfortunately ‘the smartest guys and gals in the room' (no reference to Enron) do better. Elitist as it may sound, the last time I looked Harvard and Yale were not open enrolment colleges; they attract the best.

Below we reproduce the ‘deconstructed’ asset allocations that the Ivy League Endowment theory suggests. Now this ‘allocation’ produces the best combination of returns, volatility and Sharp Ratios when we look at a set of other prominent investors’ ‘deconstructed’ portfolios (see Figure 4) including Ray Dalio, Warren Buffett and Rob Arnott (note we are not saying that it is the best returning allocation that could be theoretically produced with endless amounts of time and resources). While the returns from following this asset allocation were still the best of the theoretical portfolios we looked at (where no rebalancing over time is sought) (see Figure 4), on a look back basis this portfolio still underperformed the actual returns of top endowments like Harvard and Yale by about 3-4 percentage points per annum (for the reasons listed above, and a willingness and ability of these endowments to go into some very illiquid but high returning assets).

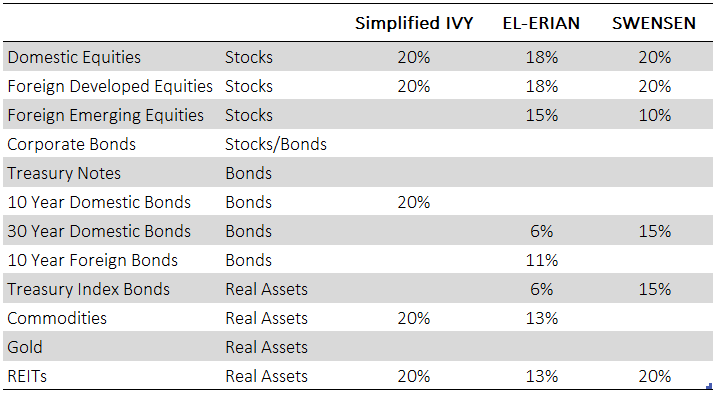

Figure 1: Ivy, Swensen, El-Erian Portfolios

Source: Global Asset Allocation, Meb Faber 2015

Source: Global Asset Allocation, Meb Faber 2015

Below we detail the returns, volatility and Sharpe ratios from the Ivy Leaguers. The column titled Ivy is a simplified version of the Ivy ‘style’. Mohamad El-Erian was the President and CEO of the Harvard Management Company (the manager of the Harvard Endowment Fund) in the middle of the first decade of this century. His allocation is adopted from his 2008 book When Markets Collide. David Swensen is the Chief Investment Officer at Yale University, and has been since 1985! Swensen invented The Yale Model with Dean Takahashi, an application of the modern portfolio theory commonly known in the investing world as the “Endowment Model”. Swensen’s allocation is adopted from his book Unconventional Success in 2005.

Figure 2: 40 Year Ivy Style Nominal Returns, annual, 1973-2013

Source: Global Asset Allocation, Meb Faber 2015

Source: Global Asset Allocation, Meb Faber 2015

I should acknowledge that in the last year some commentators have criticised the Endowment Model due to the Ivy League universities’ investment returns over the last 10 years not being as good as in decades prior (and not that stellar over the last 10 years when compared to say a simple portfolio of 60% stocks, 40% bonds). However, the last 10 years has been a pretty abnormal raging bull market fuelled by cheap money and quantitative easing. Money managers and advisers always brush off short term under-performance with “wait for a long time series and a full economic cycle to see who ‘wins’”, but in all seriousness 10 years is actually a short time when you consider the likely length of your investment journey. I bought my first shares at 19 and if I live to the average age here in Australia my investing journey will be well over 60 years. 10 years is short. I don’t know whether the Ivy portfolio will be the best over the next 10 years, but it certainly shown its colours over the long term.

And lastly when thinking about allocations, the below never ceases to scare me! Australians lead the world in myopia! No wonder history is littered with failed Australian company global expansion stories. We spend overseas, but we don’t historically invest overseas. Australians put around 75% of their stock allocation here in Australia, a market which represents about 3% of the global stock markets and even less of the global economy (around 1.6% when measured by GDP). Can you afford to risk that Australia will be as good in the future as it was in the past, particularly as our sharemarket is so concentrated these days to a few sectors like banks and mining companies and the fact we are so dependent on China (not to mention the potential franking credit change coming through)?

Figure 3: Crocodile Dundee Investing (Home Country Bias) – Actual investment by Australians in Australian Equities vs Total Market Cap of Australian Equities as a % of World Total Source: Global Asset Allocation, Meb Faber 2015

Source: Global Asset Allocation, Meb Faber 2015

Figure 4: Historical Nominal Results of All Portfolio Types Analysed 1973 – 2013

Source: Global Asset Allocation, Meb Faber 2015

Source: Global Asset Allocation, Meb Faber 2015

On a closing note, so I don’t get called a hypocrite, outside of the home that I live in approximately 50% of my investments are offshore (real estate, managed by the Fortius Global Value team).

*The Sharpe Ratio measures the excess return (or risk premium) per unit of deviation in an investment asset or a trading strategy, typically referred to as risk. The higher the ratio, the greater the investment return relative to the amount of risk taken.

Disclaimer: This article is prepared by Fortius Property Investment Management Australia Ltd ABN: 14 152 737 052 AFSL: 412083 (Fortius). It is not an investment recommendation. Prospective investors are not to construe the contents of this article as tax, legal or investment advice. Neither the information nor any opinion expressed constitutes an offer to buy or sell any financial products, nor the provision of any financial product advice or service. The content has been prepared without considering your objectives, financial situation or needs. In deciding whether to acquire or continue to hold an investment in any financial product, you should consider the relevant disclosure documents for that product which are available from the product provider. Fortius recommends you consult your professional adviser to determine whether a financial product meets your objectives, financial situation or needs before making any decision to invest.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Harvest Lane is Australia's only pure play M&A focused Fund Manager. I've been working in the investment management industry for over 25 years in Sydney, New York and London. I have a strong track record of increasing wealth for investors.

6 topics

Harvest Lane

Harvest Lane is Australia's only pure play M&A focused Fund Manager. I've been working in the investment management industry for over 25 years in Sydney, New York and London. I have a strong track record of increasing wealth for investors.

Harvest Lane

Harvest Lane is Australia's only pure play M&A focused Fund Manager. I've been working in the investment management industry for over 25 years in Sydney, New York and London. I have a strong track record of increasing wealth for investors.

Comments

Comments

Sign In or Join Free to comment