Why it pays to follow the insiders

There is an asymmetry of information in markets which is one of the key reasons buyers and sellers are willing to transact at a given price, as investors try to make perfect decisions with imperfect information. So, what if we were closer to having perfect information, surely our decision making should improve right? That’s the theory of insider trading. A practice that despite the common misconception, does exist in a governed, legal form which is what we are referring to herein.

At Chester we have material personal investments in our fund because we believe in what we do and believe aligning our interests with those of unit holders, enhances our stewardship of their capital. We seek the same when we invest in companies. I.e. we seek an alignment of interests between us and the board and management, which often comes with equity ownership. For this reason, we are encouraged when insiders take to buying stock and pause for consideration when insiders sell.

What can be gleaned from insiders' trading?

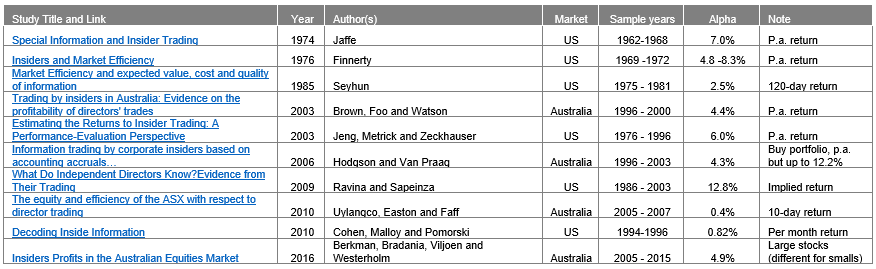

We wouldn’t want to cheapen a 50k word PHD by trying to replicate their work with a shorthand article but below we have attempted to quantify some of the historic studies to give us a point of reference on insider dealing. Despite debates around its application as a decision-making input, evidence does exist to support the notion insider dealing can lead to alpha generation.

Source: Table prepared by Chester Asset Management but refer Further reading for links to referenced study

This is by no means an exhaustive list and doesn’t include studies that argue to the contrary regarding insider dealing. However, it does provide evidence we have done at least some reading and provides a reference for anyone wanting to do further reading.

How to interpret insider trading

Following insiders' leads in buying and selling decisions is a bit like Sex Panther perfume (per the movie Anchorman), 60% of the time it works every time. This was evident in our review of historical literature and in the director trades of FY2019 and FY2020. We make the following points, some of which are somewhat obvious.

- Director buying has greater information than director selling. This famous Peter Lynch quote sums it up best "insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise."

- Without detracting from the above quote, buying is sometimes undertaken by insiders to game markets and assist capital raising efforts, a phenomenon common but not limited to small cap resource companies

- The closer to the coalface the better. As the Perich family may attest, executives buying and selling is a better signal than a non-executive director, given Management should have a better understanding of the day to day operations. Some papers have even gone as far as suggesting CFO trades are more profitable than CEO trades

- Director trading as a signal is more powerful the smaller the company

- Obvious point but the more directors transacting (and obviously the more material the stake) the better the signal. We have tried to show this as a % of market cap in the tables below

- One-off opportunistic trades (i.e. one off on-market buying) is more powerful than “routine” trades. The Cohen, Malloy and Pomorski 2010 study showed this best with 0.82% abnormal monthly return vs 0% for routine trades

- Insiders can often act well in advance of good news so the phrase “stay the course” is relevant

- Stocks with high free cash flow yields that are subject to insider buying have even stronger outperformance than low free cash flow yield purchases

- There can be many false flags. Just ask any investor who got spooked because Bevan Slattery sold 10 million NXT shares in November 2014 at AUD1.95/share, or 3.3 million MP1 shares in May 2019 at AUD5.11/share

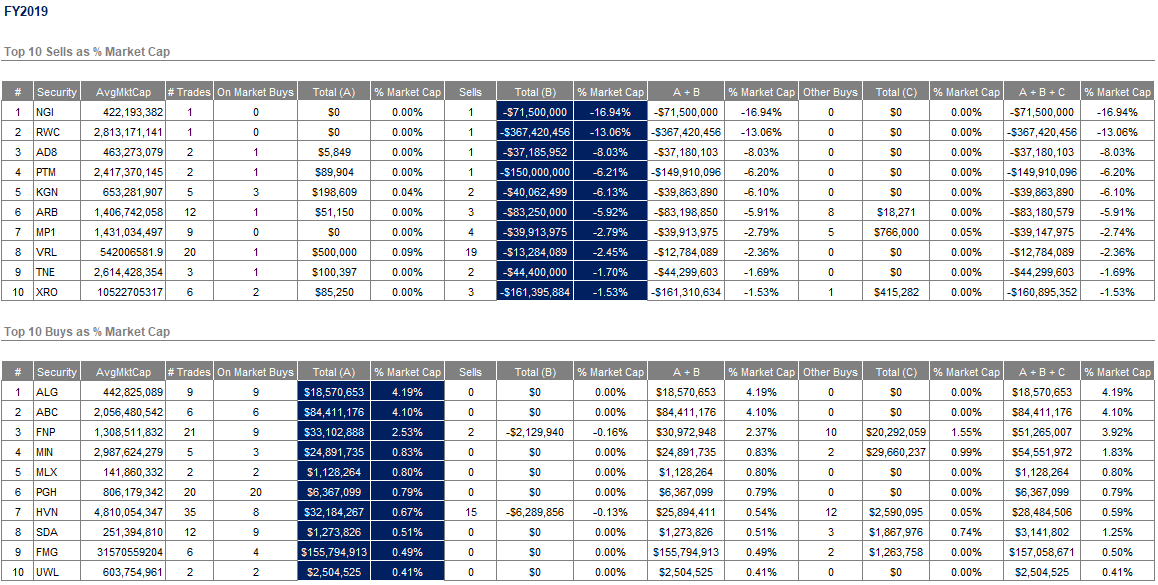

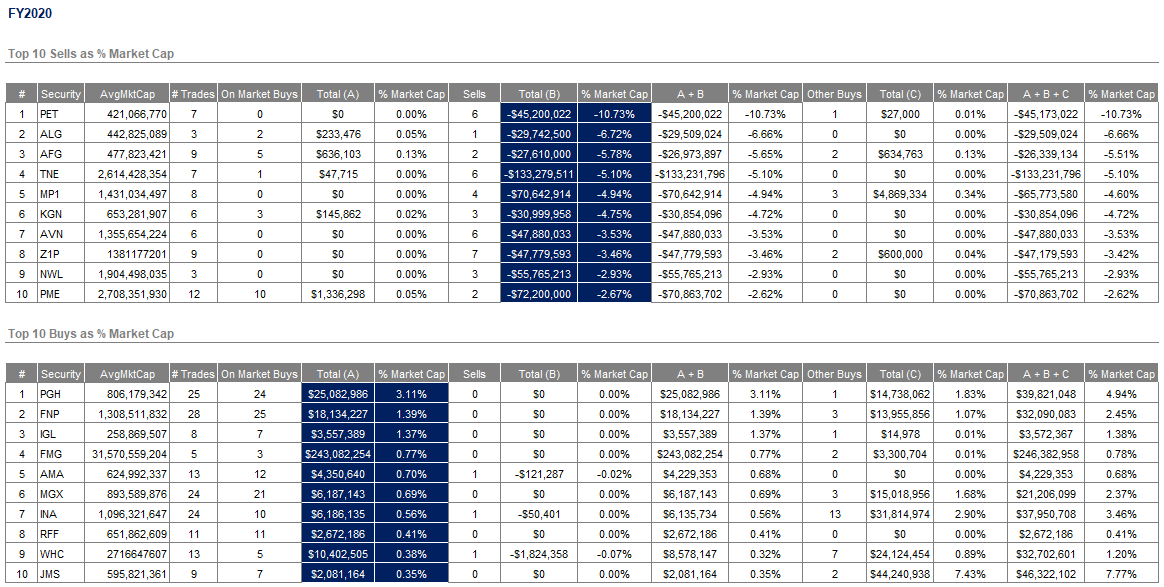

Director Transactions in FY19 and FY20

Most market participants will refer to Bloomberg for cues regarding insider trading but we have noted that the Bloomberg data doesn’t necessarily split insider dealing into on-market trades and other trades. While we can’t speak to the accuracy or completeness of the data contained in Market Index it does appear to offer greater information content than Bloomberg, albeit at the expense of extra manpower inputting data and working spreadsheets, to compile the following tables. We won’t provide a stock by stock analysis of each of these but in the subsequent paragraph we provide some examples of how Insider dealing has contributed to the Chester decision making process.

Source: Chester Asset Management with data from Market Index

Source: Chester Asset Management with data from Market Index

Decision making examples

While we don’t necessarily run screens searching for material director trades to identify stocks to buy, sell or avoid it does feature in our assessment of a company’s governance and in our decision making by testing or adding to our conviction. Below we have listed a subset of examples of the input of insider dealing within our process.

- ORA. We sold out in FY2019 given deteriorating fundamentals and management turnover. Multiple directors (MD and Chairman) selling in March 2019 contributed in our decision making to exit the position

- OGC. Multiple material director purchases in November 2019, including by the MD and Chairman added to our conviction in building a position. Refer Underappreciated and unloved Gold

- RWC. The (final) AUD367m 10% sell down and severing of ties by the original founders in February 2019, less than 12 months after the acquisition of John Guest left us very cautious and out of the name in 2019

- UMG. Multiple (14!) director purchases (including executives) on-market in the past 6 months has increased our conviction in the stock

- MIN. Material director purchase (AUD19m) in May 2019 supported our buy on the stock right before our note, A different kind of Portfolio Manager

- IMD. Director selling in December 2019 provided an opportunity to test our thesis but didn’t change our decision to hold

- A2M. Material share disposals in August 2020 by the Chairman, interim CEO, AsiaPac CEO and other Executives leaves us cautious on the outlook for the company

- Energy. Multiple energy names have seen recent insider buying which has drawn our attention

- Technology. We

have recently witnessed Directors selling in a number of technology companies above what we see as fair value for the company

Owners of capital

We will look to release a more detailed paper on executive remuneration and tenure in the coming 6 months but as noted in our opening, part of our thought process on insider dealing extends to the overall level of insider ownership.

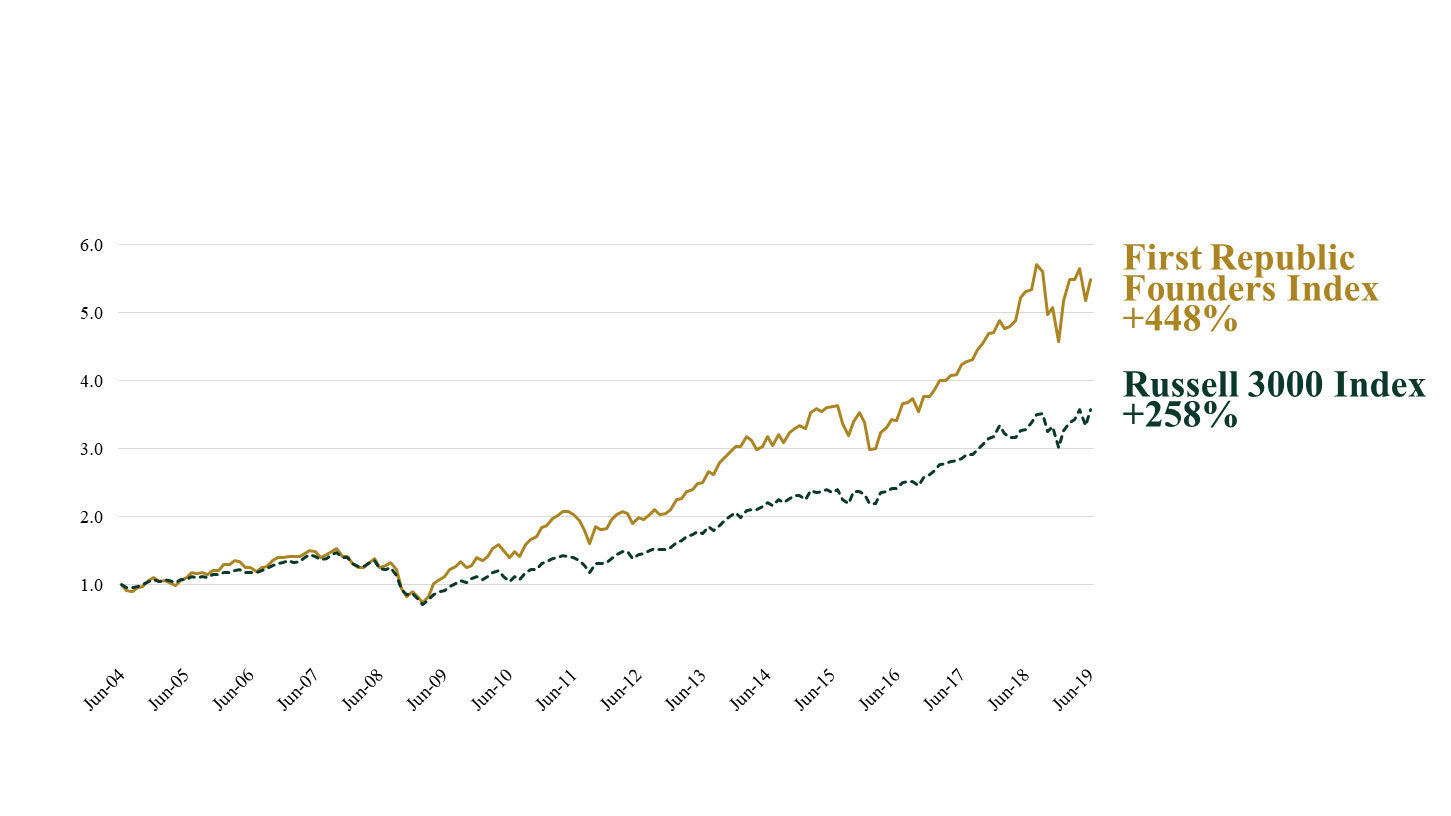

We find that owners of capital have much stronger alignment of interests with shareholders than non-owner stewards of capital (executives without significant stakes or long tenures) which as evident in the graph below has historically translated to outperformance. Another somewhat obvious point but the smaller the company the more likely it is for founders and owners of capital to exert more influece over the direction and success of the company, hence aligning ourselves to passionate and entrenched founders / CEOs is something we pay a good deal of attention to. There are plenty of reasons why owners of capital outperform including but not limited to the culture in the company driven by the mindest of its founders to challenge industry norms and persevere. Jeff Bezos, who is probably the most famous founder of our time, also has some of the most expensive failures was once quoted as saying, "If you decide that you’re going to do only the things you know are going to work, you’re going to leave a lot of opportunity on the table".

Source: First Republic Bank

Source: First Republic BankConclusion

We would all love to be able to utter the phrase “I am not uncertain” in our stock selection. With information asymmetry not just a feature but one of the key reasons markets exist maybe the best we can hope for is less uncertainty. Hence insider dealing and ownership should be incorporated as factors to consider in a portfolio decision making framework.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Further Reading

- Special Information and Insider Trading

-

Insiders and Market Efficiency

- Market Efficiency and expected value, cost and quality of information

- Trading by insiders in Australia: Evidence on the profitability of directors' trades

- Estimating the Returns to Insider Trading: A Performance-Evaluation Perspective

- Information trading by corporate insiders based on accounting accruals…

- What Do Independent Directors Know?Evidence from Their Trading

- The equity and efficiency of the ASX with respect to director trading

- Decoding Inside Information

- Insiders Profits in the Australian Equities Market

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chester Asset Management is a high conviction equities fund manager co-founded in 2017 by Rob Tucker and Anthony Kavanagh, with a 25-40 stock benchmark unaware strategy comprised of predominantly broadcap (ASX300) stocks.

........

Past performance is not a reliable indicator of future performance. Positive returns, which the Chester High Conviction Fund (the Fund) is designed to provide, are different regarding risk and investment profile to index returns. This document is for general information purposes only and does not take into account the specific investment objectives, financial situation or particular needs of any specific individual. As such, before acting on any information contained in this document, individuals should consider whether the information is suitable for their needs. This may involve seeking advice from a qualified financial adviser. Copia Investment Partners Ltd (AFSL 229316, ABN 22 092 872 056) (Copia) is the issuer of the Chester High Conviction Fund. A current PDS is available from Copia located at Level 25, 360 Collins Street, Melbourne Vic 3000, by visiting chesteram.com.au or by calling 1800 442 129 (free call). A person should consider the PDS before deciding whether to acquire or continue to hold an interest in the Fund. Any opinions or recommendations contained in this document are subject to change without notice and Copia is under no obligation to update or keep any information contained in this document current

3 topics

29 stocks mentioned

Chester Asset Management is a high conviction equities fund manager co-founded in 2017 by Rob Tucker and Anthony Kavanagh, with a 25-40 stock benchmark unaware strategy comprised of predominantly broadcap (ASX300) stocks.

Chester Asset Management is a high conviction equities fund manager co-founded in 2017 by Rob Tucker and Anthony Kavanagh, with a 25-40 stock benchmark unaware strategy comprised of predominantly broadcap (ASX300) stocks.

Comments

Comments

Sign In or Join Free to comment