TOL - 12th Nov, 2024

Why it’s still too early to call the low in battery metals prices

Morgan Stanley outlines why the prices of key battery metals like nickel and lithium aren’t likely to rally any time soon.

No doubt those who went on the battery metals investing journey during the 2021-22 bull market (and chose to stick around) are wondering when the current and severe bear market in many battery metals prices will end.

At Market Index-Livewire, we are fortunate to have access to the latest research from the most respected broking and research houses covering financial markets. We have consistently brought you the latest information on battery metals markets from the likes of Citi, Goldman Sachs, Macquarie, Morgan Stanley and others, and whether they thought ‘the low’ was in.

To the collective credit of those we’ve reported views from over the last 12 months or so – they’ve been generally consistent – it’s unlikely the low is in just yet. Whether you like the message or not, the experts have generally got it right.

This morning, a new battery metals research report came across my desk from Morgan Stanley titled “Battery Metals: Between a Rock and a Hard Place?” It reads less than ideal for battery metals investors: While there are some signs markets may finally be finding some “cost support”, it remains too early to say the low is in.

Let’s review the main contentions of Morgan Stanley’s report.

Lithium: Near-term floor, but sustainable rebound more “challenging”

Morgan Stanley acknowledges that there are “signs of stabilisation” in both lithium carbonate and spodumene prices. The other key lithium mattery mineral, lithium hydroxide, shows no sign of reversing its steady decline and “remains under pressure”.

Benchmark lithium carbonate futures prices appear to be stabilising, volumes up (click here for full size image)

For brevity, I won’t show you all the key lithium minerals prices, but good news – I post their charts each evening on my Twitter/X feed. I happen to concur with Morgan Stanley’s assessment of “stabilisation” in lithium carbonate and spodumene – particularly in the benchmark lithium carbonate contract on the Guangzhou Futures Exchange (GFEX) (chart above) – where the price action has returned to rising peaks and rising troughs on increasing volume.

Morgan Stanley blames the stabilisation in certain lithium minerals prices on promises made in September by Beijing that it would finally tackle weak demand within the Chinese economy, as well as the current period corresponding with gearing up of seasonally strong battery production ahead of looming Lunar New Year holidays.

Morgan Stanley also points out recent supply cuts from some producers, largely forced, given that as much as 20% of global lithium producers are losing money at current prices. These producers account for around 250kt lithium carbonate equivalent (“LCE”) annually, or around 19% of global production.

“However, further cuts are needed to bring the market back to balance, and given the rise of swing capacity that can turn back on quite quickly, we see any price recovery as likely to be capped.”

– Morgan Stanley

Unfortunately for lithium bulls, Morgan Stanley believes that the “trickling in” of supply cuts so far isn’t going to be enough to balance the market. Further, they note that many of the cuts applied so far will be too easy to reverse if and when prices recover – citing Pilbara Minerals (ASX: PLS) recent FY25 guidance cut and idling of its Ngungaju plant as an example. It would only take 4 months to turn it back on, notes the broker.

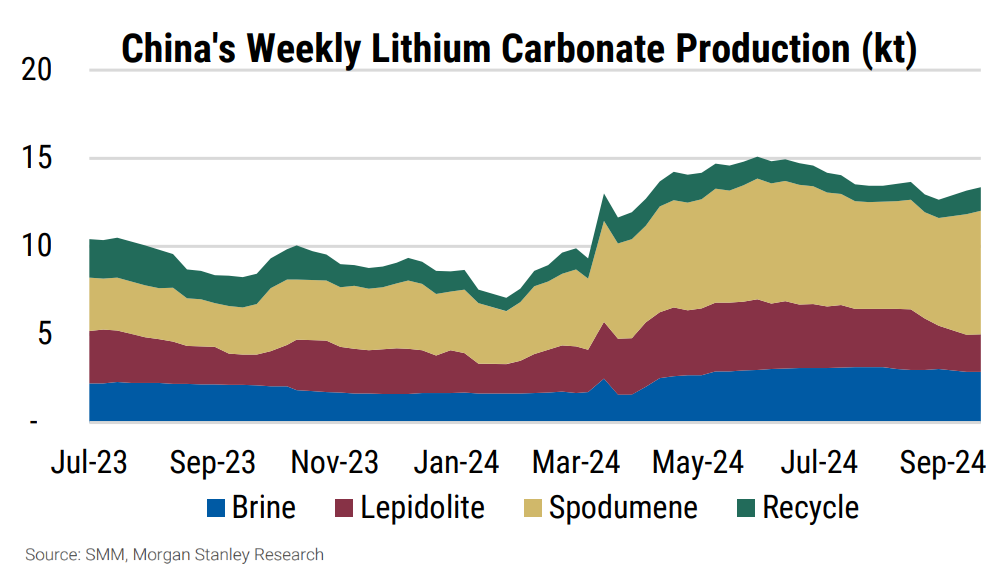

Another issue for lithium minerals prices is that China’s domestic lithium carbonate production has continued largely unabated in 2024, regardless of lower prices. Lithium carbonate is seen as the lowest common denominator in lithium minerals production and pricing – indeed many market metrics are expressed in LCE. Morgan Stanley notes lithium carbonate production has remained resilient with input materials switching from Chinese lepidolite (see this article) to Australian-sourced spodumene and South American brines.

Shifting to the issue of demand, Morgan Stanley points out that we’re in a period of peak seasonal demand for short-range, or ‘neighbourhood’ electric vehicles (“NEV”) in China. China NEV sales reached a record high of 1.3 million units in September, likely supported by government trade-in subsidies.

Morgan Stanley says that battery production is up 8% in September in response and is forecast to rise another 6% in October. “But as peak season fades in November, battery demand is expected to soften”, the broker suggests, and this will “loosen the balance” in lithium minerals markets.

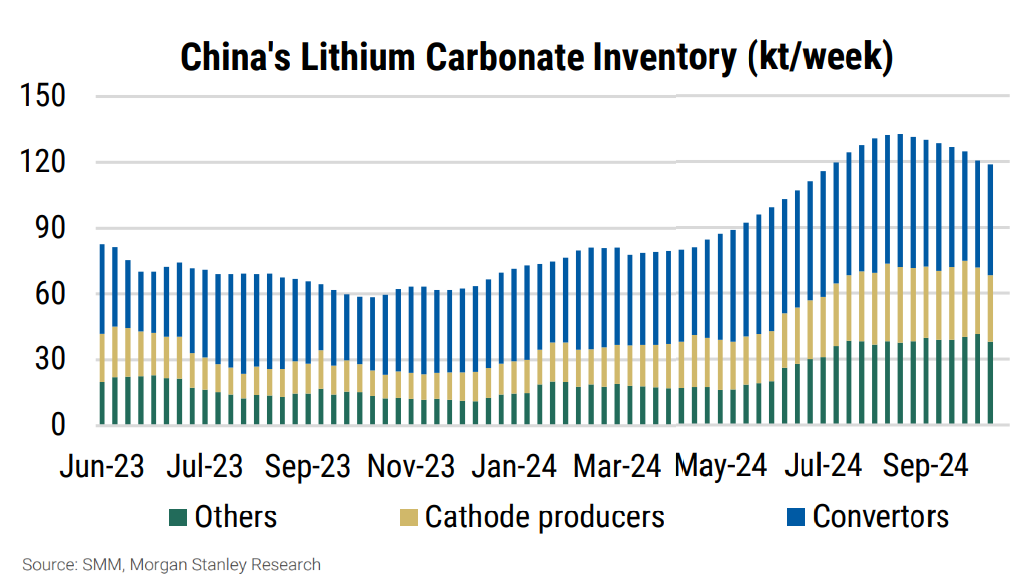

Finally, Morgan Stanley notes that inventories across the supply chain remain high, “dampening the potential price recovery”. The broker suggests inventories are 70% higher as at mid-October compared to the start of the year, and this is limiting restocking and, therefore, “restraining price upside”.

“In our view, lithium has likely found a near-term floor but a sustainable rebound may be more challenging”

– Morgan Stanley

After taking into account each of the short-term factors, as well as several longer-term concerns such as emerging battery technologies (i.e., the ongoing development of sodium-ion batteries), Morgan Stanley concludes that while the potential for “further meaningful downside in lithium is fading for now”, upside will likely be “capped”.

Nickel: Room for short-term bounce, but “tough” after that

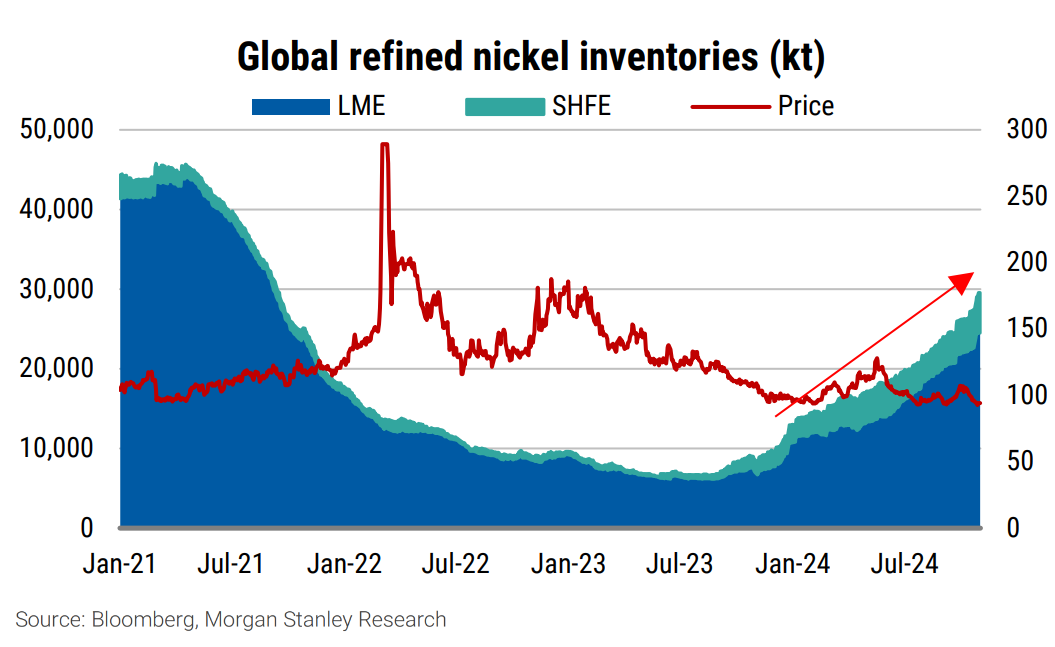

Morgan Stanley notes that nickel is bouncing off the key $16,000/t support level it touched earlier in the year. Supply cuts from projects in Australia and New Caledonia have been “significant”, but there have been few incremental cuts to improve the current market imbalance.

A rising industry cost base, restraint from major global producer Indonesia (60% of global production), and supply disruptions due to seasonal and project-specific related issues is helping firm $16,000/t as a potential near-term floor.

Another key swing factor could be a major project in New Caledonia that is presently only sustaining production due to French government support. If this project fails, it could remove as much as one-third of the market surplus currently forecast in Morgan Stanley’s models.

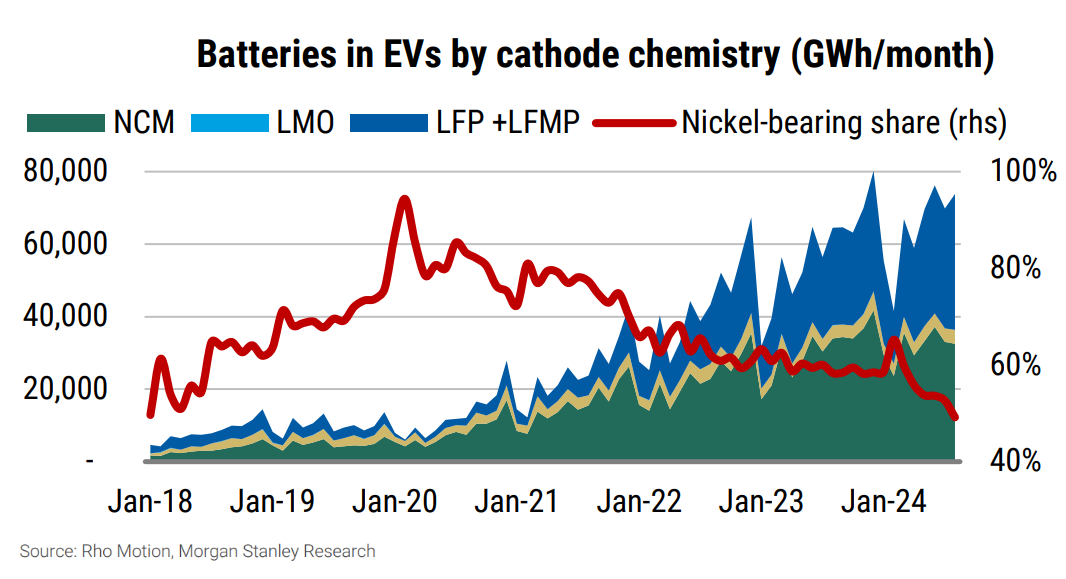

Tempering a more meaningful recovery in the nickel prices is a combination of declining market share of nickel intensive EV batteries, softening steel production in China, and risks associated with the outcome of the US presidential election – particularly those relating to tariffs on China and the removal of EV subsidies and tax breaks.

Morgan Stanley concludes there is likely “limited further downside” for the nickel price, but also that there is “limited scope” for anything more than a “tactical rebound”. The broker is forecasting the nickel price to remain range bound between $16,000/t and $18,000/t in the near term.

If nickel has one advantage over lithium, Morgan Stanley suggests, it’s that it will be far more difficult to restart shuttered nickel projects compared to similarly idled lithium ones.

This article first appeared on Market Index on Wednesday 6 November 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

5 topics

13 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment