TOL - 17th Sep, 2024

Why the market is wrong in expecting four RBA interest rate cuts in the next 12 months

Key interest rate futures now imply the RBA will cut rates four times in the next year, but these brokers think that’s just plain wrong.

Something rather odd has occurred within the last 24 hours. No, it’s not the miraculous rally in ASX lithium stocks! This one probably won’t get any headlines because it stems from a relatively murky and often overlooked area of the market – cash rate futures.

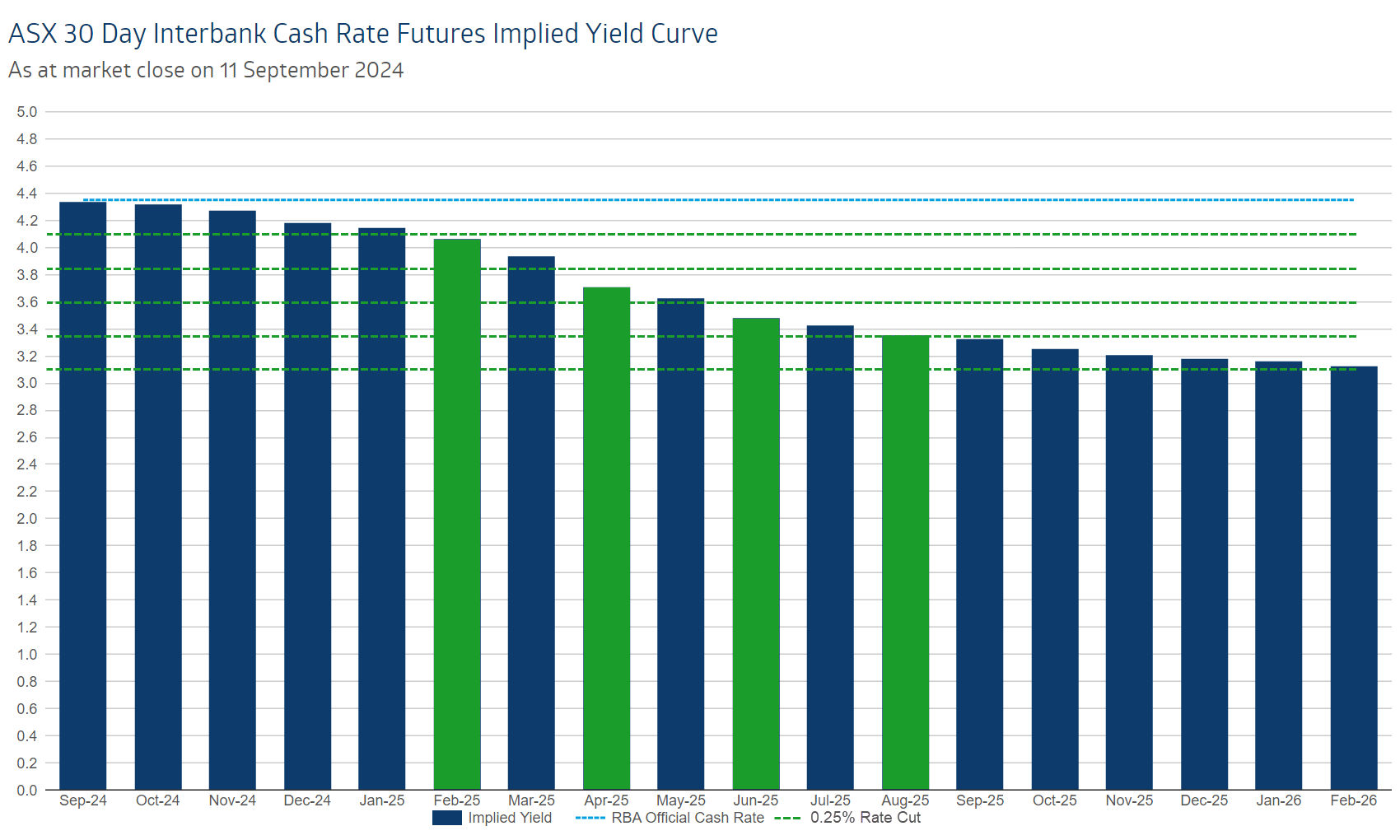

At the end of each trading day, the ASX publishes its RBA Target Rate Tracker which calculates the probability of changes in the Overnight Cash Rate based upon the implied yields of very short term (30 day) interest rate futures. The Overnight Cash Rate is a market proxy for the Reserve Bank of Australia’s (RBA) Official Cash Rate (OCR). The Tracker provides investors with a graphical representation of where the market is predicting the RBA’s OCR will be down the track.

I check the Tracker every morning, without fail. Interest rates represent the price of money, and the RBA’s OCR is the root of all interest rate pricing in Australia. The price of money affects the price of all other assets, including stocks. Generally, stocks prefer lower interest rates to higher interest rates, as lower interest rates increase consumer spending and reduce company borrowing costs – both beneficial for company profits.

The other key driver of stock prices apart from company profits, is through the discount rate. This is the rate at which stock analysts discount the future earnings of a company back to a present value – and therefore how they derive what level of a company’s share price represents good or poor value. For the same dollar of next year’s forecast profit, a lower discount rate will allow a professional investor to pay more for that dollar’s profit.

In summary: Lower interest rates help juice company profits and allow investors to bid up the value of the company’s shares.

Markets are betting on deep RBA cuts

Back to the RBA Target Rate Tracker. I’ve noticed that today, for the first time since this phase of the RBA’s rate hiking cycle began in May 2022 – markets are pricing in four interest rate cuts within the next 12 months.

How to read the RBA Target Rate Tracker:

- Each bar represents the expected RBA OCR by the end of the relevant month

- The current OCR is 4.35% (dashed blue line) and the RBA typically moves in 0.25% increments / decrements

- If the blue bars rise to 4.6% or above, the market is factoring a 0.25% rate hike

- If the blue bars fall to 4.10% or below, the market is factoring a 0.25% rate cut (and so on, so the next triggers are 3.85%, 3.60% and 3.35%

- One can also work out partial probabilities. For example, if a blue bar is at 4.475%, it is predicting a 50% chance of a 0.25% increase in the OCR by that month

The Tracker as at yesterday’s close shows that markets are predicting the RBA will first cut interest rates by 0.25% in February 2025, and then again in April, June, and August. The probability of any rate cut this year stands at 68% – better than odds on!

Why aren’t markets listening to the RBA?

I can’t remember another time that market pricing is so at odds with RBA rhetoric. RBA Governor Michelle Bullock has gone to great pains to remind us that the outlook for inflation, and therefore interest rates, “remains highly uncertain”.

As per the RBA’s most recent Statement of Monetary Policy (SMP) in August, the RBA Board also stated: “Data have reinforced the need to remain vigilant to upside risks to inflation. Returning inflation to target within a reasonable timeframe remains the Board’s highest priority.” Add to this their long-standing “the Board is not ruling anything in or out” chestnut – and it’s clear that as far as the RBA is concerned – the next move in Australian interest rates could be either up or down.

So why aren’t markets listening to the RBA? The answer lies in global interest rate movements and associated market pricing. Official rates have already started to come down in other jurisdictions, with recent cuts in Europe, the UK, Canada, and New Zealand. They’re expected to come down very soon in America, with markets pricing an 85% chance of a 0.25% cut when the Federal Reserve meets again on Wednesday next week.

Market pricing of Australian interest rates doesn’t occur in a vacuum and moves in overseas rates markets are having a major impact on local rates pricing – even if this is at odds with RBA rhetoric up to this point.

In a recent research note*, major broker Citi offered one explanation for the discrepancy, noting the “high correlation between G10 central bank policy rates means that financial markets will be hesitant to price in [RBA] policy divergence against the US Fed”. A near term cut or cuts won’t change the RBA’s mind, suggests the broker, but it will likely cause them to step up their rhetoric that they are running their own race on interest rates.

Indeed, Citi feels this step-up has already begun, potentially in anticipation of the Fed’s next move. “We believe there has been a gentle pushback by the Governor and Deputy Governor recently on the market pricing for the path of RBA cash rates”, the broker notes, labelling RBA Governor Michelle Bullock’s speech last week as “the strongest defence of previous policy decisions provided on the public record”.

In that speech, Bullock made it very clear that If inflation were to remain elevated, the RBA would act to slow the economy by even more than it has. This could mean higher unemployment and distress for mortgage holders based on her now famous “some may need to sell their homes” comment.

No cuts this year…but the next move is down – Brokers

Citi doesn’t see the RBA cutting rates this year, noting “We still don’t believe that the RBA can cut rates this year, despite what the Fed does”. The broker believes that “still strong labour market and sticky underlying inflation pressures” will leave the RBA’s hands tied well into 2025.

Morgan Stanley agrees. In a recent research note discussing the August CPI data*, the broker concluded “Market pricing retains a likelihood of a rate cut which we see as still unlikely given the data to hand. Indeed, today's CPI print is consistent with our view for a continued hold from the RBA, with cuts beginning May 2025.”

There is a general consensus among the major brokers that the next move in official Australian interest rates is down, but there is a clear divergence between the timing of their views and market pricing. If Citi and Morgan Stanley are correct, the idea of four rate cuts within the next 12 months is pure market fantasy.

The upshot is, if rates take longer to fall than the market is factoring, and given the market’s love affair with lower interest rates, it could increase volatility in share prices if the RBA is only just beginning to step up its hawkish rhetoric.

It is therefore going to be increasingly important for investors to pay close attention to RBA messaging and how this impacts market pricing of interest rates. How big will the RBA’s push back be, and how much of a tantrum will the market throw if it doesn’t get what it wants?

*1. “Australia Economics: Talk is cheap; is the RBA engaging in forward guidance & what will it do if the Fed cuts by 50bps?”, Citi Research, 3 September 2024. *2. “July CPI: Slow Progress”, Morgan Stanley Research, August 28, 2024.

This article first appeared on Market Index on Thursday 12 September 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

5 topics

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment