Markets: We don’t believe you RBA…We expect 3 rate cuts in the next 12 months!

The Reserve Bank chose to keep its cash rate on hold at their August meeting, but market pricing suggests they’re about to cut, and cut big…

You would know by now that the Reserve Bank of Australia (RBA) chose to keep its official cash rate on hold at yesterday's Board Meeting. In addition, RBA Governor Michelle Bullock has indicated Australians shouldn’t expect a rate cut “in the next six months”. In fact, she went to great pains to stress that the bank retains its laser-like focus on bringing Aussie inflation back to within the RBA’s 2-3% target band.

What you may not know is that market pricing in key interest rate futures pegged to the level of the RBA cash rate are tipping three 0.25% cuts to the cash rate by this time next year.

There’s two possibilities here. Either, the RBA is pulling our leg about the prospect of upcoming rate cuts – something any Aussie with a mortgage who’s struggling under the weight of the present cost of living crisis is hanging out for – or the market has it very, very wrong.

According to Governor Bullock, it’s the second option: Markets have it wrong.

“The markets are betting their money on that’s what we’ll do. I wouldn’t say they’re right or not – they’re trying to guess what we’re going to do. What I’m trying to tell the markets today, is that probably expectations for interest rate cuts are a little bit ahead of themselves,” Governor Bullock said.

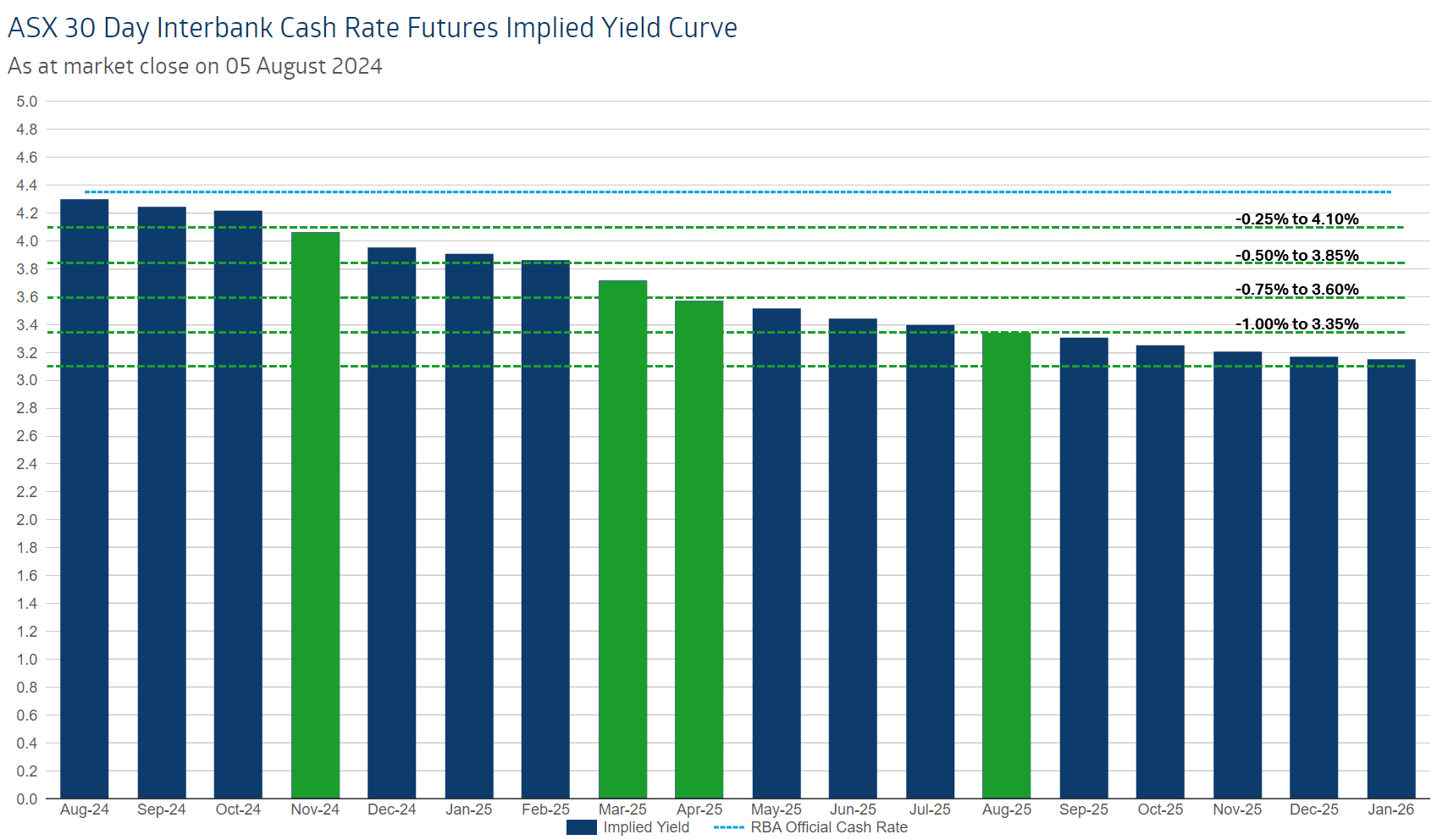

See below the market pricing of the RBA’s cash rate as proxied by the ASX 30 Day Interbank Cash Rate Futures Implied Yield Curve “implied yield curve” for the day before the RBA meeting.

When the dark blue bars fall below the level that corresponds to a 0.25% multiple under the RBA’s current 4.35% cash rate, it represents the market predicting a rate cut by that month. So, before Tuesday's meeting, the market was pricing in four 0.25% interest rate cuts over the next 12 months, with the first in November this year to be followed by cuts in March, April, and August.

Now, this version of the implied yield curve has been dramatically impacted by the major market turmoil that spiked fears of a recession in the USA, and stoked fears of financial markets contagion after the partial unwinding of the carry trade in Japan.

When markets get nervous about the prospects of either a recession in the USA or one that is more widespread, or a financial market calamity (that to be fair, could also cause a global recession), they sell risky assets like stocks and buy relatively safer government bonds.

This flow of global capital has had the effect of driving up the prices of government bonds. Because of the inverse relationship between bond prices and bond yields, those recent gains in bond prices have driven benchmark bond yields dramatically lower.

So, it appears much of the pricing in the implied yield curve in Chart 1 is influenced by circumstances beyond the RBA’s control. In some ways, the market was predicting that enough bad stuff is going to happen to the global economy, and then by extension the Australian economy – to force the RBA into three 0.25% cash rate cuts by this time next year, and nearly 4 by the end of 2025.

At Tuesday’s press conference, Governor Bullock did everything she could to change the market’s mind that rate cuts are coming soon:

There’s the not “in the next six months” comment;

There’s the statement that in this last meeting the Board only considered two options: “Hold, accepting that we may need to hold for some time, or raise”; and

There’s the point-blank calling markets out on their prevailing impending recession narrative: “Are we heading for a recession? I don’t believe so and the Board doesn’t believe so, because we still believe we are still on that narrow path”.

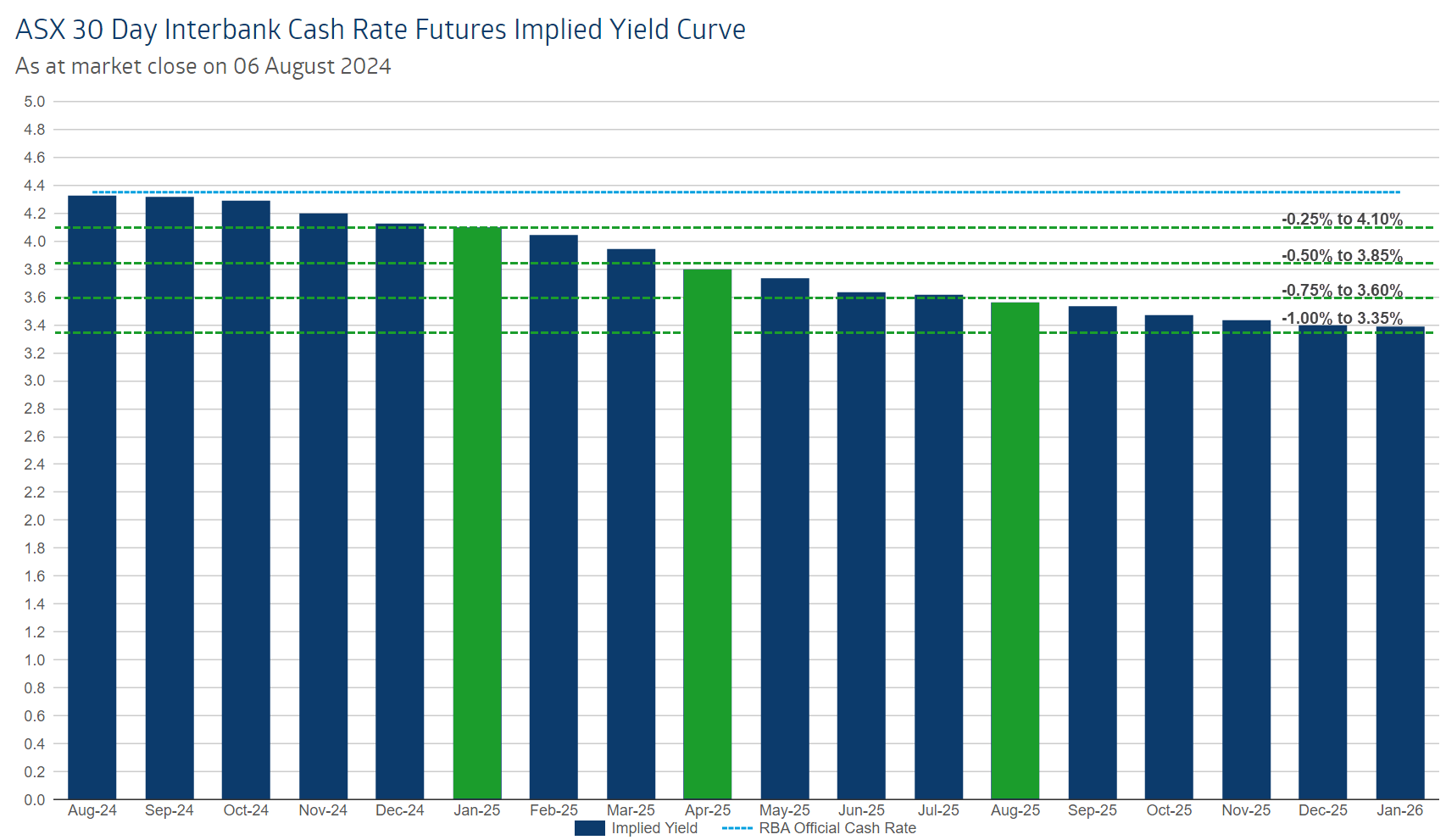

But, as much as the RBA tried to set the record straight on Tuesday, it seems markets either didn’t get the message or investors just don’t believe the Australian Central Bank. Here's the market response. See below, the implied yield curve post August meeting.

What’s an RBA governor supposed to do!? The market has only pared back their expectations from four cuts to three rate cuts in the next 12 months. At least the market has heeded the Governor’s call not to expect the first cut within six months – it’s shifted this from November to January.

Who do you believe?

As an investor, you’ll have to decide who to believe: the central bank or the market?

If the central bank is right, interest rates are likely to stay higher for longer. If this plays out, it’s probably because the Australian economy hasn’t fallen into the toilet – which is a good thing for stocks.

Yes, the stock market loves lower interest rates – it’s good for consumers and that’s good for company profits. It also lowers the cost of company debt repayments and allows for more aggressive pricing of shares on the share market due to a lower discount rate applied by investors.

But a recession in the Australian economy (possibly caused by a global recession or another global financial crisis) will be far more damaging to the Australian share market than the benefit of getting a few rate cuts.

It’s some version of this last scenario that the market is still factoring in – and the problem is history shows the market has an uncanny knack of correctly pricing risk. So, I suggest we hope the market has it wrong this time – and we don’t see rate cuts any time soon!

This article first appeared on Market Index on Wednesday 7 August 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

{kind=link}

{kind=link}

5 topics

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment